Global geopolitical trends we’re tracking this week:

Key Dates

- May 16 – China industrial production data for April. Data for both industrial production and retail sales are expected to reflect a robust ongoing recovery in the Chinese economy, coming in at a projected 10% and 25% respectively.

- May 16 – China retail sales data for April.

- May 17 – Japan 1Q GDP data. Japan’s struggles with COVID-19 throughout 2021 will show in its Q1 GDP numbers, which are projected by Reuters to see a contraction of 4.6%, down considerably from the country’s Q4 2020 growth spike of 11.7%.

- May 17 – Minutes from latest Australia central bank meeting.

- May 18 – UK unemployment data for April.

- May 18 – US building permits for April.

- May 19 – UK Consumer Price Index (CPI) for April.

- May 19 – Euro zone CPI data for April.

- May 19 – Canada core CPI data for April.

- May 19 – US crude inventories.

- May 19 – Minutes from latest meeting of US Federal Open Market Committee (FOMC). These minutes will be of particular interest to investors, who will be poring over them in search of evidence of dissenting opinions regarding the Fed’s commitment to a dovish monetary policy amid mounting inflationary signs.

- May 19 – Australia unemployment data for April.

- May 20 – Germany Producer Price Index (PPI) data for April.

- May 20 – Japan CPI data for April.

- May 21 – UK retail sales for April.

- May 21 – Manufacturing and services PMI survey data for May.

- May 21 – Canada retail sales for March.

- May 21 – Existing US home sales for April.

World

COVID-19 fast facts

- New COVID-19 cases saw a marked decline globally over the past week. The 7-day average of new daily cases on May 8 was approximately 783,000. As of May 15, the number had dropped to 648,000.

- The US reported fewer than 30,000 new cases on Saturday, bringing its 7-day average to its lowest level since June.

- After effectively weathering the pandemic for over a year, an expanding outbreak has brought lockdown restrictions to Taiwan, which recorded 180 new local infections over the weekend.

- Thailand and Nepal are seeing record highs in daily infections.

- Update on vaccination coverage (percentage of population with one dose) as per Bloomberg and OWID vaccine trackers: Israel (60%), United Kingdom (54.4%), United States (47.1%), Chile (47.2%), Canada (39.4%), Germany (36.6%), Spain (22.1%), France (31%), Brazil (18.2%), China (13.6%), India (10.3%), and Russia (9.7%). Among these countries, the largest weekly jumps in population coverage were in Canada (5.3%), Germany (5%), and France (4%).

Europe

Inflation focus shifts to Europe

After a series of upside inflation surprises in the United States, the week ahead will help to fill out the picture for Europe, where we’ll see price data releases for the UK and euro zone. Both are expected to reflect significant year-on-year jumps similar to recent US data; however, there’s plenty of room to grow before running afoul of any central bank inflation targets. March CPI came in at 0.7% for the UK and 1.3% for the euro zone.

Middle East

Israel unrest spreads to West Bank

Last week saw unprecedented inter-communal violence in Israel and another outbreak of hostilities with Hamas in Gaza. Then, on Friday, major protests erupted across Israel-occupied West Bank, where at least 10 protestors were shot and killed and hundreds wounded in clashes with security forces. At least 13 Palestinians are believed to have been killed in the West Bank since Monday of last week. Developments in the West Bank could well be decisive in determining the longevity and character of this latest upheaval in the Israel-Palestine conflict, as they hold out the (admittedly faint) possibility of some degree of reconciliation between the otherwise antagonistic entities of Fatah and Hamas, along with their respective support bases. One gets the feeling that Fatah in particular is ripe for supplanting given its aging (and perhaps ailing) leadership and the absence of any credible peace process for years. Whichever group steps into the vacuum created by recent events could have an outsize influence over Israel-Palestine relations for years to come.

Asia

Anti-coup resistance taking on an armed dimension in Myanmar

An armed militia took over a town of 10,000 people in northwestern Myanmar three weeks ago, declaring its opposition to the junta government. Over the weekend, it was driven out by the Tatmadaw, with deaths reported on both sides. The militia, which was formed in the wake of the coup and calls itself the Chinland Defense Force, has since fled into the nearby mountains and is expected to continue waging a guerilla campaign against the military.

This was just one incident, but it’s emblematic of a growing trend in post-coup Myanmar – that of ethnic groups arming themselves and mobilizing against junta forces in pursuit of the more longstanding objective of achieving greater local autonomy under a more federalized constitution. The very same dynamic has fueled clashes between the Karen National Union (KNU) – a much more established and well-armed ethnic militia – and the Tatmadaw in the southeast of the country.

Fighting between the military and ethnic militias is one of several fronts where the junta government is under mounting pressure. Others include ongoing protests in Myanmar’s major cities, explosions that have been targeting government offices and military facilities, and a nationwide civil disobedience movement that has kept doctors, nurses, and civil servants from working.

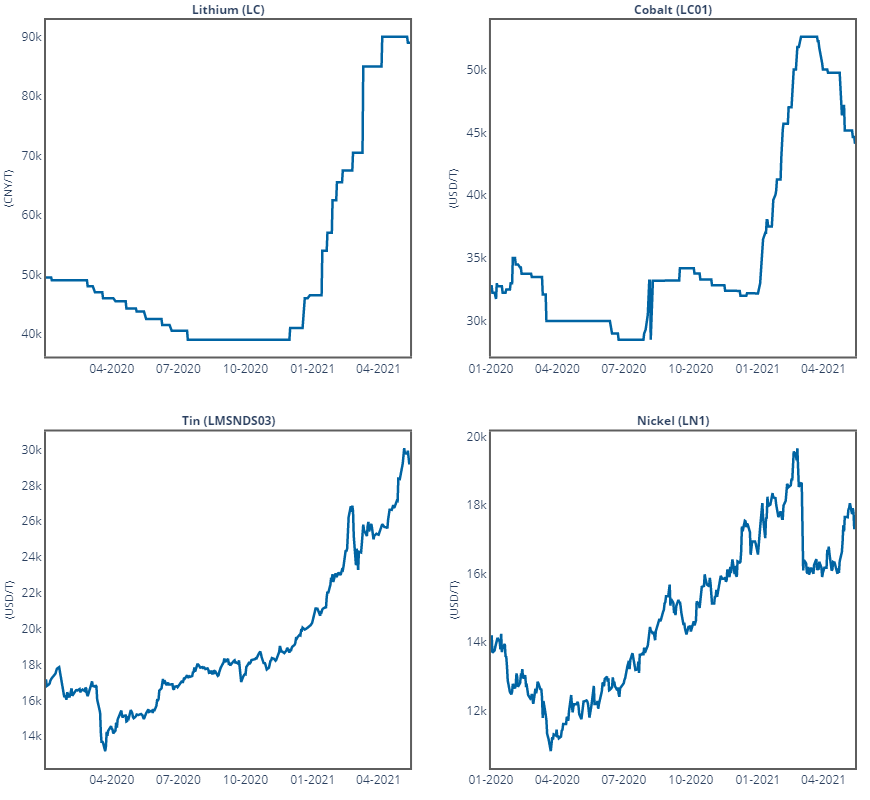

Strategic Commodity Snapshot

Albemarle’s first quarter earnings were a tale long foretold, that of rising lithium prices on the back of global supply constraints and steadily rising demand for EVs. The company has also jumped into the battery recycling industry in anticipation of the millions of EVs that will be scrapped upon reaching their end-of-life starting in the late 2020s and 2030s.