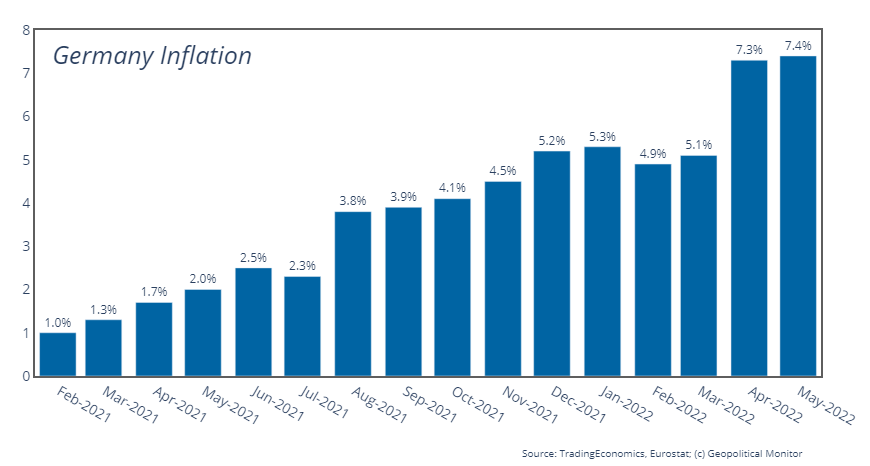

Consumer prices in Germany saw increases of 7.9% year-on-year in May and 0.9% month-on-month. Unsurprisingly, food and energy were the main culprits fueling inflation, with energy up a jaw-dropping 38.3% year-on-year and food up 11.1%. The May numbers represent a new post-unification high, fresh on the heels of a record-breaking April.

Consumer prices in Germany saw increases of 7.9% year-on-year in May and 0.9% month-on-month. Unsurprisingly, food and energy were the main culprits fueling inflation, with energy up a jaw-dropping 38.3% year-on-year and food up 11.1%. The May numbers represent a new post-unification high, fresh on the heels of a record-breaking April.

They’re paralleled by other negative inflation data out of Spain, which saw a surprise upswing in May, dashing hopes of a peak earlier in the year. Spain’s inflation rate of 8.5% in May came after a dip from 9.8% in March to 8.3% in April. Similar to Germany, inflation is being fueled by strong upward pressure in energy and food prices.

Analysis

Taken together, the Germany and Spain data complicates the immediate task-at-hand for the European Central Bank (ECB), which is widely expected to lock in a tightening cycle at its upcoming meeting by signaling rate hikes starting in July and a conclusion of large-scale asset purchases. However, recent inflation numbers in major EU economies contradict the official narrative of an orderly and linear come-down from recent highs, raising the specter of a more prolonged period of high inflation.

On the surface, the numbers would also seem to merit some kind of policy adjustment from the ECB. Recall that the Bank’s inflation target is a mere 2% over the medium term, well below the current economic reality (even when one removes energy and food costs from the index, inflation in a country like Spain is still running at over double the ECB target). The ECB’s projections underscore the disconnect between what’s imagined and what’s real: the Bank apparently foresees the HICP returning to 2.1% in 2023 after posting an average 5.1% rate in 2022. It envisions a 1.8% rate in 2023 excluding food and energy costs, which reveals the true extent to which these costs have been overlooked in the projections, apparently only accounting for .3% on average over the course of the year.