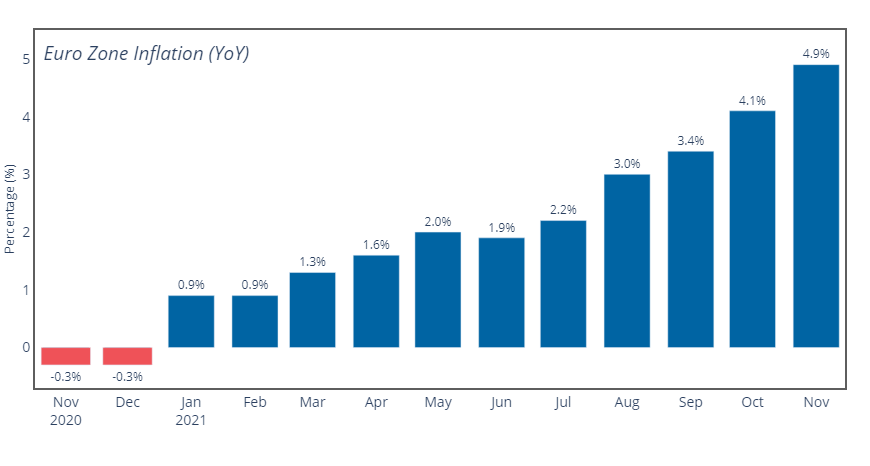

Brussels’ preliminary estimate of euro zone inflation for November came in at 4.9%, representing the highest year-on-year level since 1991. The reading is up from 4.1% in October, and comes in well above the consensus expectation of 4.5%.

Brussels’ preliminary estimate of euro zone inflation for November came in at 4.9%, representing the highest year-on-year level since 1991. The reading is up from 4.1% in October, and comes in well above the consensus expectation of 4.5%.

Rising energy costs far and away accounted for the greatest price increases, with energy costs up 27.4% compared to November of last year. Both services and food costs saw increases from the previous month, with services coming in at 2.7% (up from 2.1%) and food 2.2% (up from 1.9%).

In terms of month-on-month momentum, prices increased by 0.5% in November; prices were up across the board with the exception of services, which dipped 0.2% from October 2021 levels.

On the upper band of the inflation trend lies Lithuania (an estimated 9.8% annual inflation for November), Estonia (8.4%), Latvia (7.4%), and Belgium (7.1%). On the lower end, Italy (4%), France (3.4%), Finland (3.4%), Portugal (2.7%), and Malta (2.3%). Germany – Europe’s largest economy and ever-vigilant guardian against any and all inflationary forces – registered an estimated annual November rate of 6% (HICP), which is just shy of its all-time post-war record from 1992.

The political subtext of the November disclosure is obvious: this will increase pressure on the ECB to give some ground on its dovish policy outlook, which presently entails ongoing quantitative easing measures and a no-hike pledge through 2023. Similar forces are at work in other major central banks; for example, just today Fed head Jerome Powell admitted that “factors pushing inflation upward will linger well into next year,” representing the latest shift of an official line that had previously maintained that inflation would dissipate in early 2022.