The European Central Bank (ECB) strategy review – the first such overhaul since 2003 – has produced a crop of policy changes that will revamp how the Bank gauges inflation and set the stage for a more activist monetary policy on climate issues.

Analysis

A new and nimble inflation target

A new inflation target is the headline reform. Previously, the ECB’s target was “below, but close to 2%.” Now that target is 2% even, and the bank has reserved the right to temporarily exceed it whenever economic conditions demand.

The change will eliminate the vagueness of the original target. It also represents a failure by the inflation-averse Germany to have its hawkish proclivities reflected in continental monetary policy – a significant loss given the infrequency of these strategy reviews. However, COVID-related price volatility aside, the ECB inflation target has frequently been rendered a moot point by the strong deflationary forces of the past decade. Deflation, rather than inflation, is more often the overriding concern of ECB policymakers.

A new mandate on climate change

The ECB has also pledged to take climate change into account in future policy decisions. More specifically, this entails:

- Expanding analytical capacity in macroeconomic modelling, statistics, and monetary policy with regard to climate change. (Developing in-house tools with which to gauge the risks involved).

- Including climate change in monetary policy operations regarding disclosure, risk assessment, collateral framework, and corporate sector asset purchases.

- Implementing the action plan in line with progress on the EU policies and initiatives in the field of environmental sustainability disclosure and reporting.

In the short-term, the most consequential of these changes is the inclusion of climate change considerations in corporate sector asset purchases, which could effectively exile energy majors and other emitters from ECB stimulus programs like, for example, the ongoing corporate sector purchase program (CSPP), which has made some $282 billion worth of bond purchases since 2016 and currently holds the bonds of energy majors like Eni and Shell. Under the new standard, to be unveiled in detail in 2022, all companies will be required to make climate-related disclosures ahead of their potential inclusion in ECB asset-purchasing programs.

Another notable disclosure from the central bank is: “The ECB will consider relevant climate change risks when reviewing the valuation and risk control frameworks for assets mobilized as collateral by counterparties for Eurosystem credit operations.” This would come as another blow to carbon emitters, as bonds held by European banks might not be considered safe collateral from which to secure short-term liquidity from the ECB.

The natural result would be a slimmed down bond market, and thus higher borrowing costs for carbon-emitting industries. However, there will be a lot of wiggle room in how the ECB implements its new climate mandate (for example, the extent of collateral worthiness of ‘dirty’ bonds, the rigidity of carbon-reporting standards, etc.). So the devil will be in the details in just how much of an impact the ECB’s strategic review will have on carbon emitters. It is undeniable however that the new mandate outlined in this security review expands the climate toolbox available to ECB policymakers, should they choose to make use of it.

A new way to quantify inflation

The review will also tweak the Harmonized Index of Consumer Prices (HICP), the central index used by the ECB to gauge inflation. The HICP does not include owner-occupied dwelling costs at present, instead using a basket of items like rent, maintenance, and utilities to calculate housing prices overall. The ECB has pledged to incorporate house prices into the HICP, but tempers expectations by noting that “this is a difficult task that will take some years to implement.” If current trends hold, their inclusion will provide a boost to HICP readings. Housing prices were up 5.8% across the euro zone year-on-year in Q1 2021, which doubtlessly impacts household budgets across the continent yet remains obfuscated by the current HICP standard.

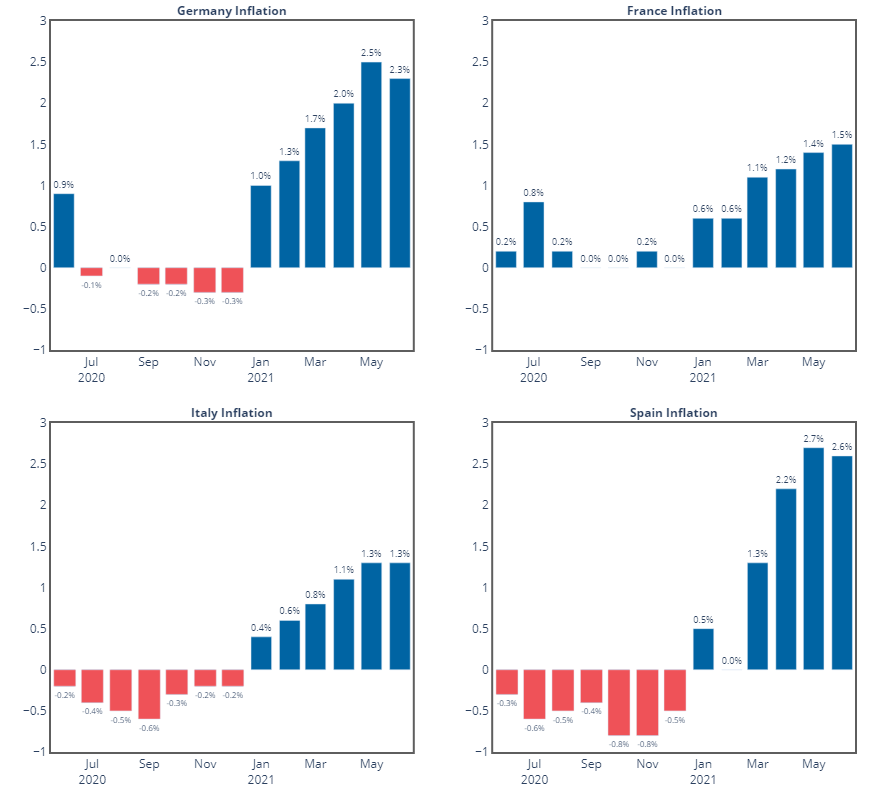

Here is the national inflation outlook for major euro zone economies:

- Sailors assigned to the submarine tender USS Frank Cable (AS 40) man the rails as they pass Mount Suribachi following a wreath-laying ceremony commemorating the 70th anniversary of the Battle of Iwo Jima. The ceremony honored those who fought in the battle and included personal testimony from Sailors who had family fight in the battle, laying of a wreath, a 21-gun salute and the playing of taps. Frank Cable, forward deployed to the island of Guam, conducts maintenance and support of submarines and surface vessels deployed in the U.S. 7th Fleet area of responsibility and is currently on a scheduled underway period. (U.S. Navy photo by Mass Communication Specialist 2nd Class Greg House)")