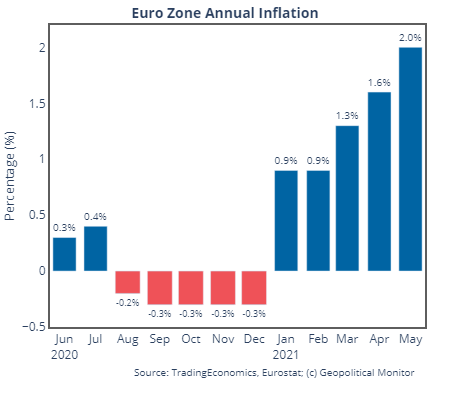

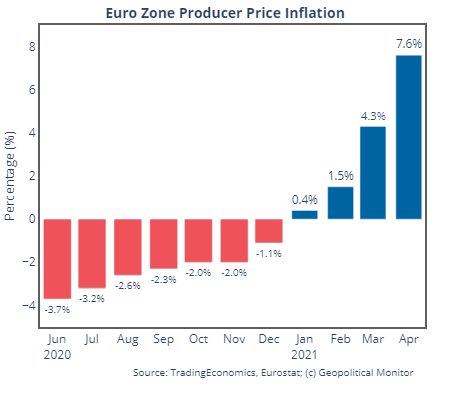

On Monday, a flash estimate from Eurostat projected euro zone annual inflation at 2% for May 2021, up from 1.6% the month before, and in excess of the ECB’s 2% inflation target for the first time since 2018. Euro zone data for producer prices then followed suit on Wednesday, posting a 7.6% year-on-year increase, well above the consensus estimate of 7.3%.

This double-whammy of inflationary surprises continues the trend of rising input prices globally, and the stage is now set for a potentially eventful meeting of European Central Bank (ECB) policymakers next week in Frankfurt.

Analysis

The euro zone consumer price index (CPI) was up 13.1% in May on a year-on-year basis (which is skewed by the sweeping disruptions brought on by COVID-19 last year). The largest monthly jumps in inflation were recorded in Malta (1.3%), Estonia (0.9%), Slovakia (0.7%), Latvia (0.6%), Spain (0.5%), France (0.4%), and Germany (0.3%).

The main culprit behind euro zone inflation of late is energy prices. In the CPI’s sector-by-sector breakdown, energy led the field in monthly gains at 0.7%, followed by unprocessed foods at 0.6%. This is not terribly surprising considering that a barrel of Brent crude cost around $35 to close out May 2020; as of today, that price has more than doubled.

A similar impact can be discerned in the euro area producer price data released today which, at 7.6% in annualized terms, was the biggest jump in producer inflation on record since September 2008. Though the month-on-month reading is not as distorted by the shocks of COVID-19, it too skews higher than many economists had expected, contributing to the wider inflationary trend of Q1 2021.

Overall, the biggest spikes in producer prices were seen in Ireland (+34.1%), Denmark (+13.3%), and Belgium (+13%).

Energy was also the primary driver of producer input inflation, with prices increasing 20.4% in annualized terms and 1% month-on-month in April. When energy is removed from consideration, the price of all other industrial inputs grew 3.5% year-on-year and 0.9% month-on-month. On the surface, this would seem to justify the ECB maintaining its dovish policy stance next week; however, it’s worth noting that the velocity of price increases over the past two months remains conspicuous whether energy is included or not. These official numbers also back up growing anecdotal accounts of supply-side crunches up and down the continent; for example, a recent HIS Markit eurozone purchasing managers’ index found that “average input costs [were rising] substantially… hitting an unprecedented level in line with widespread product shortages,” as per reporting from the Financial Times.

All eyes on ECB governing council meeting next week

The latest inflation figures are sure to be a hot topic of discussion at the ECB’s monthly policy meeting in Frankfurt next week.

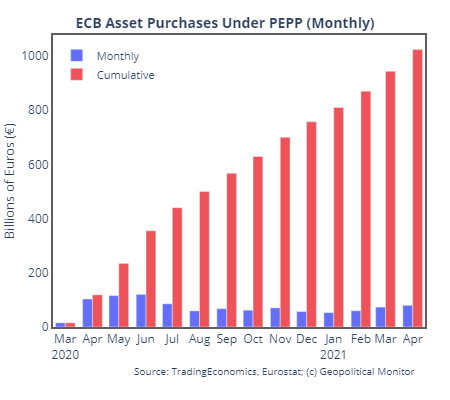

In March, the euro zone banking authority ramped up its bond-buying program amid resurgent COVID-19 infections in many EU states. Its justification at the time hinged on resurgent bond yields in euro zone countries, which had been showing signs of life after a prolonged period of dormancy in 2020. As a result of the meeting, the pandemic emergency purchase programme (PEPP) increased the pace of its bond purchases (the program originally had €1,850 billion to spend through March 2022, and the decision could have been influenced by the growing belief that the most harmful effects of the pandemic will have run their course well before that date arrives).

The ECB purchased approximately €59 billion worth of assets in February 2021, the vast majority of which were sovereign bonds of member states (primarily Germany, Spain, France, Italy, and the Netherlands). By April, after meeting’s adjustments were implemented, the ECB was purchasing around €80 billion worth of assets per month.

ECB policymakers will look to answer one critical question next week: Is the uptick in prices of the past few months a temporary phenomenon, or does it represent economic overheating that must be brought under control by a hawkish shift in monetary policy? For her part, ECB president Christine Lagarde has thus far remained unphased by rising prices, dismissing inflationary pressures as temporary in nature as recently as two weeks ago.

All told, it’s unlikely that the ECB will unveil any major policy shifts next week for two reasons: 1) there is a ready explanation for recent inflation in the form of COVID-related disruptions, and 2) inflation is actually a welcome change of pace for an economy that typically suffers persistent deflation, although only so long as the inflation remains within acceptable bounds (bounds that tend to be exceedingly conservative given Germany’s aversion to the slightest hint of runaway price growth). However, we may see some new signaling from the ECB with regard to the future drawdown of the PEPP, much like how the central banks of other developed economies have begun to look to the exits in recent months.

Inflation data from the next few months will be decisive. Additional inflationary surprises will inevitably erode faith that rising prices are a passing trend and generate added pressure for the ECB to enact monetary policy normalization. And when the ECB bond-buying program does finally wrap up, highly indebted euro zone governments like Italy (estimated to surpass 158% of GDP in public debt this year), may find themselves suddenly unable to borrow at the rock-bottom prices they’ve enjoyed throughout the pandemic; but that’s a crisis for a future article.