With the Ukraine war stopping flows of Russian oil to Europe and attacks by the Houthis (an Iran-aligned militant group in Yemen) undermining maritime trade through the Red Sea, recent years have highlighted the vulnerability of energy markets to geopolitical developments. Despite the growing need to transition from fossil fuels to renewable energy, the world is set to continue to consume a significant amount of oil for many years. As such, oil producers and suppliers must be prepared to navigate the uncertain road ahead strategically. Although it is widely recognized that oil will become a less viable commodity, China’s economic slowdown suggests that significant changes are likely to occur much sooner than many had anticipated.

China’s transformation from an agrarian society in the 1970s to an industrialized nation is unprecedented. However, the weakening of the key catalysts that propelled China’s rapid ascent to an economic superpower has led to a slowdown in growth. Pervasive geopolitical tensions, combined with domestic challenges such as youth unemployment, the collapse of the property market, and population decline, are raising concerns about China’s growth. As the world’s second-largest economy, developments in China have far-reaching implications, driven by its deep integration into global markets. Research from the International Monetary Fund reveals that when China’s growth rate rises by 1 percentage point, global expansion is boosted by approximately 0.3 percentage points. This makes China’s economic trajectory a matter of keen interest worldwide.

Owing to the country’s substantial reserves, coal is China’s predominant energy source, with oil ranking second in terms of overall consumption. China is the second largest oil consumer in the world after the United States and possesses substantial domestic oil extraction and refining facilities. Much of the country’s domestic oil production is located in the northeastern provinces of Heilongjiang, Liaoning, and Jilin. On average, in 2023, China produced 4.2 million barrels of oil per day, but also imported 11.3 million barrels. As China consumes more oil than it produces, the country plays a major role as a key market in the global oil supply chain.

The Chinese Economy: All Good Things Come to an End

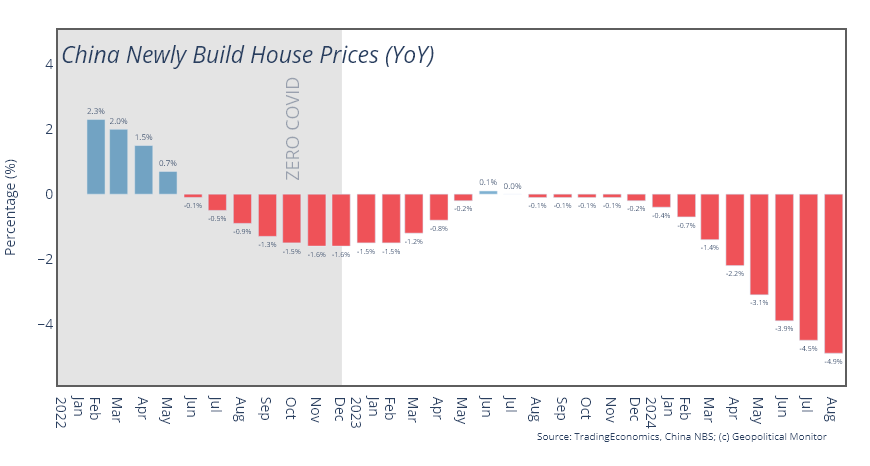

With the Chinese economy facing multiple threats simultaneously, the country has failed to bounce back following the pandemic. China’s property sector played a key role in the country’s economic growth, particularly following the deregulation of property sales in 1997, leading major private real estate firms to enter the market. Millions of domestic investors also speculated in property, with the real estate sector accounting for 70% of Chinese household wealth. Population growth and mass urbanization fueled housing demand and steady price increases, generating huge profits that prompted developers to sell properties before construction.

In 2020, Chinese Communist Party (CCP) General Secretary Xi Jinping implemented stricter regulations on the real estate market, declaring that “houses are for living in, not to be speculated on.” Given that the property sector depended heavily on such speculation, demand plummeted, leading to falling prices. As developers had to sell unbuilt houses to fund those under construction, reduced demand resulted in many unfinished housing projects. This left buyers unable to move in, impacting millions of investors and further reducing demand. With the CCP refusing to bail out property developers, the situation spiraled, resulting in the collapse of real estate giant Evergrande and the potential liquidation of Country Garden. Although officials implemented measures to stabilize the sector, such as easing mortgage rules, the fact that the average price of new homes fell at the fastest rate in almost a decade in June 2024 suggests these actions came too late.