- After years of horizontal trading, China stock markets are booming on bets of a future fiscal stimulus package that might not materialize.

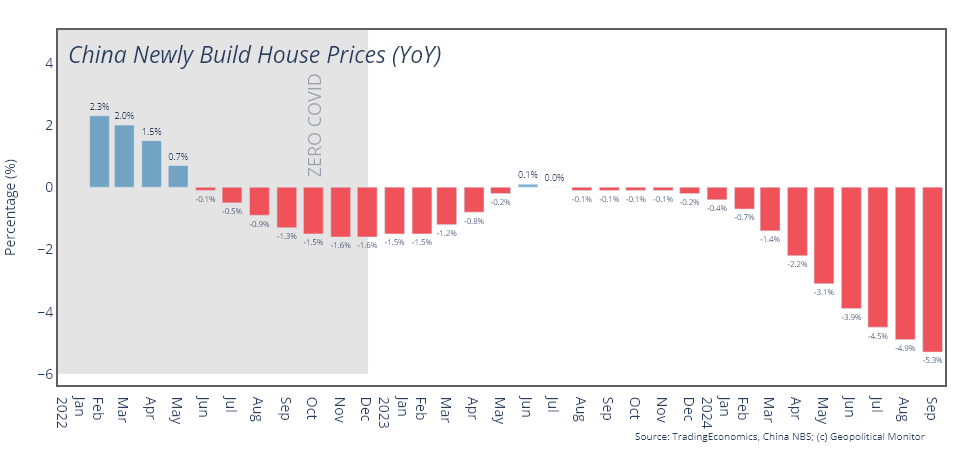

- Recent data in China’s real estate market and consumer spending do not suggest a turnaround in economic fortunes.

The rabid Fed watching of US equity markets appears to be contagious, as China stock markets have experienced wild swings as traders place bets on future stimulus announcements from Beijing.

The latest round of volatility kicked off on September 24, when the People’s Bank of China (PBOC) announced a raft of monetary policies to rouse the Chinese economy from its deflationary doldrums. The package included rate cuts aimed at broader economic activity: a seven-day repo rate cut of 20 basis points, medium-term lending facility cut of 30 basis points, and loan prime rate cut of 20-25 basis points. Yet the PBOC saved its best firepower for the stagnant real estate industry, which saw relief in the form of a 50 basis point cut to mortgage rats and a cut in minimum downpayment requirements, potentially helping to loosen the purse strings of a middle class that has lost its will to spend over the past two years. Finally, if these efforts weren’t enough to revive investor confidence, the September package also revealed direct interventions to revive Chinese equities, notably new equity purchases by state-owned funds and new liquidity facilities to help commercial banks to brokerages buy stock.

It didn’t take long for the package achieved its desired effect, as Chinese equity markets roared back to life after years of trading horizontally. The crush into equities harkened back to the glory days of 2015, when fortunes were made in the course of a six-month boom.

Yet two variables weigh down on the present market euphoria. The first is simply the fresh memory of how it all ended last time. By the time the 2015 crash had played out, stocks cratered by over 30 percent, despite the best efforts of China’s policymakers to stem the bleed, and countless personal fortunes were wiped out in the aftermath.

The second and more important reason for caution is the fact that China’s economic fundamentals do not support the euphoric mood of stock traders. This is widely acknowledged by analysts and China watchers. It’s also likely widely known among the investors now piling into the stock market, who are making bets on future fiscal stimulus on the basis of vague language from the public records of government meetings (the Chinese equivalent of divining the Fed minutes). Yet this new fiscal stimulus is anything from assured, and with each new sign that it’s not coming, equities risk correcting. This is exactly what played out on October 9, when a National Development and Reform Commission press conference failed to reveal the expected fiscal stimulus policies, triggering one of the worst one-day selloffs since 1997: the Shenzhen index dropped 8.2%, Shanghai by 6.6%, and the Hong Kong Hang Seng by 1.4%.

Absent a reversal in China’s economic fundamentals, it appears unlikely that the present rally will be long-lived. Despite some recent positive indications in top-tier cities like Shanghai and Shenzhen, China’s real estate market remains mired in a long-term decline, and one that will only be reversed when the outlook of tier-three and tier-four cities improves. Moreover, there are structural supply-demand dynamics in the sector that defy any easy or quick policy solution. Decades of over-building has produced an abundance of housing inventory, particularly in less-desirable cities, and population decline is now pulling these valuations down, likely never to recover.

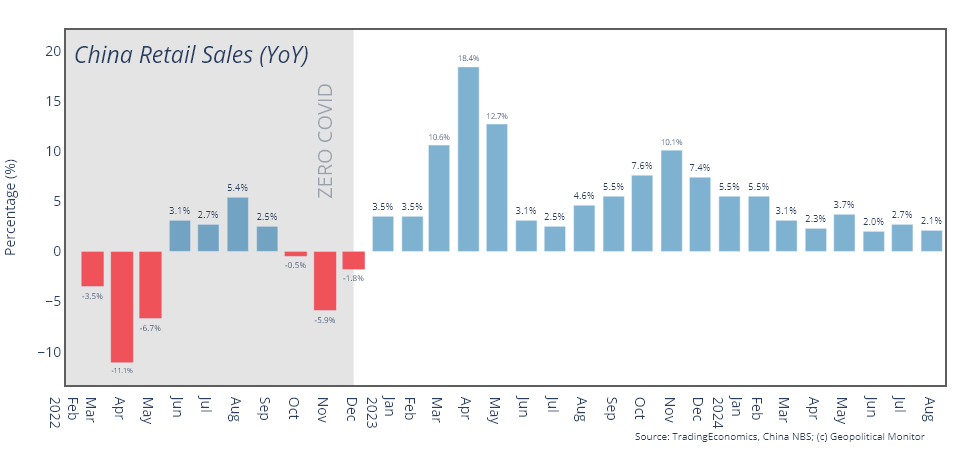

Retail sales remain weak as household wealth is squeezed by declining real estate valuations. The above chart reflects just how disappointing consumer spending has been in China since the zero-COVID restrictions were lifted. Low spending is contributing to a deflationary trend that shows no signs of slowing down. China’s Producer Price Index has been contracting since October 2022, and any optimism from the recent uptick in consumer prices in August (0.6% year-on-year) must be tempered by the fact that upward price pressure is coming from transitory weather shocks on food production; non-food inflation remains at just 0.2%, showing that the economy is not out of the deflationary woods yet.

In sum, the stock market boom appears transitory in that it is not reflective of any material change in China’s economic fundamentals. Fiscal stimulus could of course alter the country’s economic outlook, depending on the size and particulars of the package. Yet even market bets on this game-changing package, ever on the horizon, should be tempered by certain inconvenient political and economic realities. For one, the Beijing authorities have been hesitant to throw money at their economic problems for several years now, despite mounting economic challenges. Their hesitance stems from a fear of creating economic inefficiencies in the form of new non-performing assets. Absent the past playbook of generating economic activity from massive infrastructure and construction projections, the stimulus question becomes a lot more complex. How does one bail out the property market? Do local governments buy up excess stock (as is currently speculated)? If so, can this housing stock be put to any productive end or is it just an absorption of real estate losses? Bear in mind that land sales used to produce a significant portion of local government revenues, and these revenues have yet to be replaced. And two, whatever the hypothetical stimulus is, it needs to be financed by a government encumbered with a growing debt profile. China’s total debt-to-GDP hit 307.7% in June 24, up from 299.9% at the end of 2023. It’s expected to grow by a total of 12% over the calendar year, and that’s without any additional stimulus. When combined with the present trajectory of the Chinese economy, such a debt load does not lend itself to impressive fiscal firepower when designing a stimulus package.