The year 2023 will go down in history as one of defied expectations for China’s policymaking establishment and the manifold analysts who called it wrong. Both were banking on a post-pandemic economic recovery that has yet to materialize, and this failure to launch is now shaping markedly gloomier forecasts for the year ahead.

The year 2023 will go down in history as one of defied expectations for China’s policymaking establishment and the manifold analysts who called it wrong. Both were banking on a post-pandemic economic recovery that has yet to materialize, and this failure to launch is now shaping markedly gloomier forecasts for the year ahead.

One event framed the political context of the first half of 2023 more than any other: the abrupt end of China’s zero-COVID policy. The first few months of the year saw hospitals and health services overwhelmed with the sick, and a population fearful of catching a virus that had been aggressively stigmatized by the state. COVID-related deaths rapidly mounted, though no one can be sure of the exact number given underreporting in the official data. Estimates of total deaths range from the hundreds of thousands to millions.

There was a widely held expectation that, once this transitory period of epidemiological bloodletting was over, the Chinese economy would experience a boom much like the United States did after 2021, fueled by pent-up consumer demand and savings over the course of the pandemic. But this has yet to materialize, and the listless post-COVID recovery has thrown long-term economic contradictions into sharper relief, namely weak consumer spending, declining real estate markets, mounting debt burdens, and capital imbalances. Such was the story of 2023, and absent a fundamental restructuring of the Chinese economy to address these contradictions, there’s little reason to believe that 2024 will be materially different.

Consumer Spending

The creation of a confident and wealthy middle class, one that can power GDP growth through their consumption, has long been the white whale of Beijing’s economic planning. Numerous pivots have been mapped out over the years aimed at precipitating a shift from state-led investment (largely in the form of fixed capital formation) to consumption-led growth; none have met with success, and the exit from zero-COVID was no different.

It should quickly be noted here that quantifying consumer spending or any other economic metric in China is not a straightforward exercise. This is due in large part to the very real possibility of inaccurate or incomplete reporting from official organs ever sensitive to the political implications of negative data. Taking this well-established lack of transparency as a given, economic reality is most likely revealed by examining multiple data sources and placing the official numbers in their proper context.

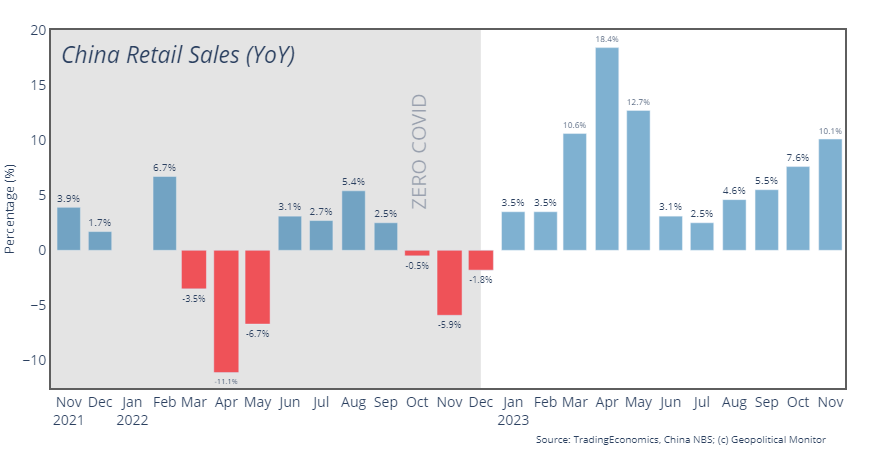

So far as the official data is concerned, consumer spending remained weak over most of 2023 before picking up in October (7.6% growth year-on-year) and November (10.1%); however, these year-on-year numbers are heavily skewed by the zero-COVID baseline of 2022. Conversely, consumer confidence surveys from the National Bureau of Statistics (NBS) reflect consistent pessimism over the final few months of the year.

Weak consumer spending is also reflected in the stock market performance of two of China’s online retail giants. The stock for JD.com (HKSE) – a Chinese e-commerce company – shed nearly 60% of its value over the course of 2023. Alibaba stock (HKSE) similarly dropped by approximately 30% over the same period. Golden Week – an extended holiday that typically represents the peak of annual travel and consumer spending – also disappointed, albeit with some positive indicators in certain sectors. In terms of travel, cross-border flights hit 1.477 million, approximately 85% of their pre-pandemic levels, but the number fell short of the 1.58 million government target. Singles Day – a one-day shopping event often likened to Black Friday – also disappointed in November, as indicated by the refusal of both Alibaba and JD.com to release their official sales numbers. This is a far cry from the pre-pandemic days when Singles Day sales data was proudly held up as proof of the implacable rise of e-commerce and the wider Chinese economy. Furthermore, third-party assessments of Singles Day have been dismal; for example, data provider Syntun estimated sales volume at 2.9% lower than in 2022, when economic activity was being throttled by zero-COVID policies.

Golden Week – an extended holiday that typically represents the peak of annual travel and consumer spending – also disappointed, albeit with some positive indicators in certain sectors. In terms of travel, cross-border flights hit 1.477 million, approximately 85% of their pre-pandemic levels, but the number fell short of the 1.58 million government target. Singles Day – a one-day shopping event often likened to Black Friday – also disappointed in November, as indicated by the refusal of both Alibaba and JD.com to release their official sales numbers. This is a far cry from the pre-pandemic days when Singles Day sales data was proudly held up as proof of the implacable rise of e-commerce and the wider Chinese economy. Furthermore, third-party assessments of Singles Day have been dismal; for example, data provider Syntun estimated sales volume at 2.9% lower than in 2022, when economic activity was being throttled by zero-COVID policies.

The failure of these high-profile retail events speaks to the tenuous position of Chinese consumers, many of whom are being pressured on multiple fronts by COVID-era disruptions to their livelihood, eroding household wealth stemming from real estate, and a weak job market, particularly for young people. But there’s another dynamic at work here: the once-dramatic discounts of Singles Day are no longer remarkable because retailers have been slashing prices year-round to entice consumer spending. The trend is also evident at the macroeconomic level as rising deflation over several months of 2023, beginning in July. Price declines then accelerated in November, which posted an annualized drop of 0.5%, more than the 0.2% drop recorded in October and suggestive of a trend heading into 2024. The mere hint of an entrenched deflationary spiral is enough to freeze the blood of policymakers as it harkens back to Japan’s post-1990s lost decade, which combined a sudden collapse in property values with long-term deflation, creating a cycle of stagnation that still reverberates to this day.

Real Estate

An overstretched consumer class is understandable in the context of China’s ongoing property crisis, which erupted during the early phases of the pandemic. The crisis originally centered on Evergrande, the second-largest property developer in China, which since 2021 has been struggling to maintain solvency after having defaulted on billions worth of loans. The ensuing vortex of collapsing confidence in real estate markets then enveloped Country Garden, mainland China’s largest private property developer, which warned in October that it is at risk of defaulting on its over $200 billion worth of debt obligations. Reuters has since reported that state authorities entered into talks in November with Ping An, a private insurance giant, urging it to take a controlling stake in Country Garden so as to alleviate some of the real estate developer’s cash flow concerns.

On a systemic level, the risk is clear: with every new default, the peril ratchets up for the remaining developers who must grapple with declining confidence. The dynamic is compounded by the nature of the Chinese real estate market, where buyers often secure their home by placing large deposits before construction has started (a system often compared to a Ponzi scheme). Such practice is the norm rather than the exception, with as much as 90% of new homes being purchased pre- or during construction. A Nomura Group report estimated some 20 million units (the equivalent of 20 times Country Garden’s output) of unconstructed and delayed pre-sold homes across the country at the 2023. The report also warns of mounting social instability in 2024 as the number of undelivered units from distressed developers ticks upward, barring more direct government intervention.

The extent of the debt levels of these distressed developers is significant. Taken together – and not including the numerous smaller developers struggling to remain solvent – Evergrande and Country Garden’s combined liability burden comes in at around $550 billion, equivalent to approximately 3% of China’s total GDP. Such sizable liabilities represent a contagion risk for China’s banking system, reflected in the recent bankruptcy of the Zhongzhi Enterprise Group, whose Zhongrong trust banking arm first signaled solvency issues in August of 2023. Both lenders were highly exposed to real estate investments, and the eventual bankruptcy came despite active efforts by the authorities to stabilize their finances.

On the ground level, Chinese households are seeing their wealth eroded by diminished sales and demand, and the effects are not evenly distributed. Real estate markets in tier 1 cities like Beijing and Shanghai, and to a lesser degree tier 2 cities like Guangdong and Jiangsu, have remained resilient relative to tier 3 and 4 cities. Similarly, new builds have historically tended to outperform existing homes due to consumer preference.

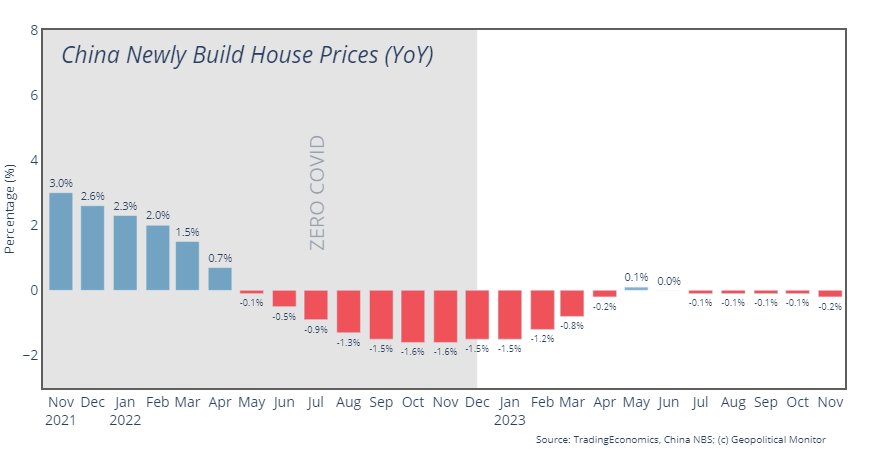

Country-wide, new house prices dropped by approximately 4.5% over the course of 2023 according to the National Bureau of Statistics (NBS) data, with price declines accelerating over the last two months of the year, posting 0.2% and 0.3% month-on-month drops respectively. Third-party assessments of the existing home market have also skewed negative. The Tianjin-based Beike Research Institute estimated a near 18% drop in prices since August 2021.

It should be noted that the NBS data likely does not reflect a complete picture of China’s real estate markets, as it is based on a survey sample using ambiguous methodology as opposed to aggregates. Moreover, the lack of public disclosure of final sales price makes any reliable third-party verification of the official numbers impossible.

The authorities have not taken this slowdown in a sector representing as much as 30% of China’s GDP lying down, and steps have been taken at all levels of government to stimulate demand and restore buyer confidence. These include a reduction in minimum down payments, waiving restrictions on multiple home purchases, and loosening financing restrictions. In large part, the story of China’s economic health in the year ahead boils down to whether or not these stimulus measures achieve their objective of stabilizing property prices and by extension the fiscal health of China’s giant developers and the banking system that sustains them. However, market watchers are remain unconvinced, with most economists polled by Reuters predicting a tepid 1% price growth rate overall in 2024. Their lingering pessimism stems from the structural nature of the problem at hand: after decades of speculative building, cities are severely over-supplied just as home demand is peaking due to economic and, even more alarming due to the long-term implications, demographic pressures. The problem is particularly acute in tier 3 cities, which together account for around 60% of China’s GDP. As recent as 2021, some 78% of total housing construction was concentrated in such cities.

Foreign Investment

‘Decoupling’ and ‘friend-shoring’ emerged as popular buzzwords in the wake of President Trump launching his trade war with China; however, the immediate impact of the policy with regard to FDI flows remained muted initially. According to research from the Rhodium Group, this temporary grace period resulted from a combination of macroeconomic factors, capital control circumvention, and overly optimistic reporting by the state authorities. In actual fact, capital inflows for long-term ‘greenfield’ projects have been declining since 2020, though the negative effects have been mitigated somewhat by strong demand among multinationals to establish China-based production targeted at the Chinese market. The end result, according to Rhodium, is an FDI outlook that is ‘lower for longer,’ thus reducing the likelihood of foreign investment rescuing GDP growth from the abovementioned contradictions in China’s domestic economy.

The more recent data is much more supportive of the idea that US-China geopolitical and trade tensions are reverberating in China’s inward FDI flows. The data point that immediately jumps out is the third quarter 2023 net deficit of $11.8 billion in FDI flows – the first such deficit since data collection began in 1998.

On one hand, it should be noted that monetary policy was a significant tailwind for multinationals looking to repatriate profits from China for safer returns in the United States. Yet it’s also true that a rare, bipartisan consensus appears to be coalescing in Washington, one that views China as a peer-level rival and antagonist despite recent attempts by the Chinese leadership to pivot back to the pre-Trump status quo. The Biden administration’s outbound investment screening program is emblematic of the new reality. The program will grant the Treasury Department authority to monitor and potentially prohibit investments involving sensitive technology in countries of concern, notably China and the Hong Kong SAR. Moreover, it’s not only the United States looking to restrict and regulate its outward investments to China. The European Union also plans to table an initiative in 2024 that will restrict investment in certain sensitive technologies on national security grounds. A successful push into investment and export controls by Brussels would mark a paradigm shift in the bloc’s security calculations, as the issue has long been a source of friction between national and EU-level governments.

While the devil will be in the details regarding how restrictive these outward screening regimes ultimately are, the new controls clearly do not bode well for investor confidence in China, especially because, like with sanctions, there is a tendency toward over-compliance where companies err on the side of caution to avoid punishment.

Government Debt

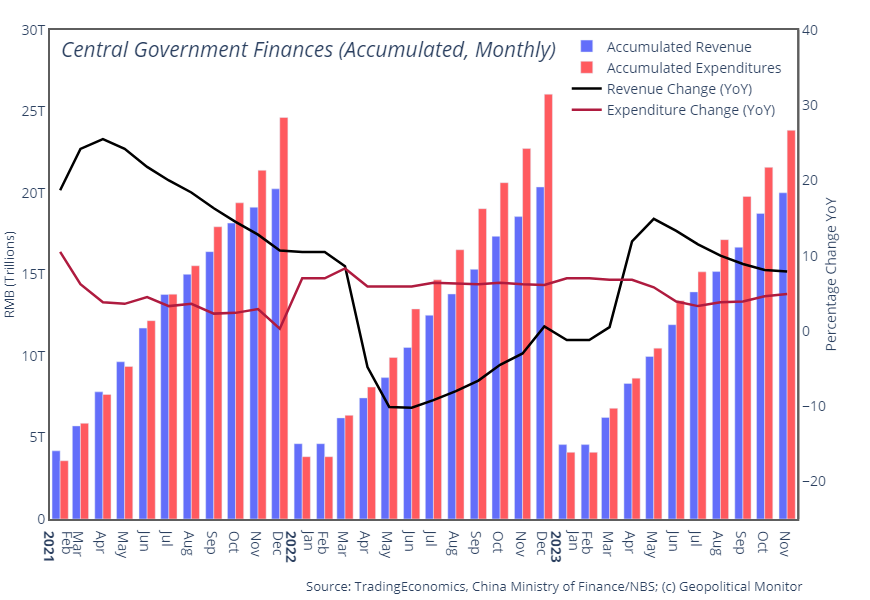

Debt remains a pressing issue for the Chinese government, though disagreements exist over severity. What’s unequivocal is that the broad long-term trend has been one of accumulation, with China’s total debt increasing four-fold, from 70% of GDP in the mid-1980s to 272% of GDP in 2022. And where the post-COVID global tendency has been deleveraging, China has moved in the opposite direction; for example, emerging markets excluding China shed 7.6% in debt-to-GDP in 2022 where China’s debt increased by 7.3%. Going back further, China accounts for over half of the entire world’s total debt-to-GDP increases since 2008.

The breakdown of China’s debt obligations is also a matter of debate owing to the opaque and often political nature of the state’s fiscal responsibilities. These can range from the straightforward local governments, which act as primary service providers despite being severely limited in their toolbox of revenue-raising instruments, to unprofitable state-owned enterprises that buttress social stability via mass employment or provision of critical services, to the countries and lending entities underpinning high-level foreign policy initiatives like Belt and Road. In nearly all cases, all roads lead back to China’s banking system, which, absent government intervention would be saddled with non-performing debts, creating systemic risk.

It was the combination of these overt and implicit responsibilities that prompted Moody’s to lower its outlook on China’s A1 debt rating from ‘stable’ to ‘negative’ in the beginning of December, a move that prompted a strong rebuke from the state media. The ratings house cited a likely bailout of local and regional governments, which themselves will be fiscally stressed by declining property values, as reasons for the downgrade.

An interesting perspective comes from Michael Pettis of Peking University, who points out that much of the focus on China’s debt burden hones in on the extent of the government’s liabilities. However, the real structural contradiction lies on the other side of the ledger – assets – where years of misallocated, state-led investment has engendered inflated valuations of what are actually non-performing capital expenditures. These valuations can be sustained only so long as the credit is available to refinance them, and the inevitable credit crunch will unleash a systemic reckoning where imaginary valuations are reconciled with reality. In light of Reuters reporting in October that the authorities are ordering state-owned banks to roll over local government debts at longer terms with lower interest rates, it would appear the reckoning is being pushed into the future. But the money to pay down these liabilities will have to come from somewhere, and until that happens the debts will continue to corrode the balance sheets of China’s major banks, hampering overall liquidity whether or not they carry the de facto ‘non-performing’ label. Incidentally, these refinancing deals are also cited by in the Moody’s downgrade as examples of the costs of local government debt being borne by the broader public sector.

Looking Ahead to 2024

Short-term success will not be measured in growth rates of 5, 6, 7% – those days are over, at least for the time being. Rather, it will come in the form of a controlled and orderly disentangling of the structural contradictions at the heart of China’s economy. Failure on the other hand could resemble the ‘lost decade’ suffered by Japan, a country that also struggled to reconcile high debt loads with low growth amid a cascading real estate collapse. But Beijing does have some advantages available to it that Japan did not in the 1990s, not least of which is the historical perspective gained from Tokyo’s long period of economic turmoil.

We can expect the recent barrage of regulatory easing and olive branches extended toward the private sector to continue in 2024, all with an overriding goal of restoring market confidence. Already the ascendance of pro-private sector and pro-growth jargon is evident in state communications, which had only recently been dominated by national security concerns. But China’s debt burden will impose hard limits to what the state authorities are able to accomplish in terms of bailing out distressed entities, whether local government, bank, or property developer. Returning to the tried-and-tested approach of mass supply-side stimulus is also presumably off the table barring a crisis, and even then it would merely be putting off the inevitable economic pain. Whatever the actual GDP growth rate was for 2023 – the Rhodium Group pegs it at around 1.5% – the year ahead will likely be modestly higher, but still well short of the official target of 5%.