The year 2023 will go down in history as one of defied expectations for China’s policymaking establishment and the manifold analysts who called it wrong. Both were banking on a post-pandemic economic recovery that never materialized, and this failure to launch is now shaping markedly gloomier forecasts for 2024.

One event framed the political context of the first half of 2023 more than any other: the abrupt end of China’s zero-COVID policy. The first few months of the year saw hospitals and health services overwhelmed with the sick, and a population fearful of catching a virus that had been aggressively stigmatized by the state. COVID-related deaths rapidly mounted, though no one can be sure of the exact number given underreporting in the official data. Estimates of total deaths range from the hundreds of thousands to millions.

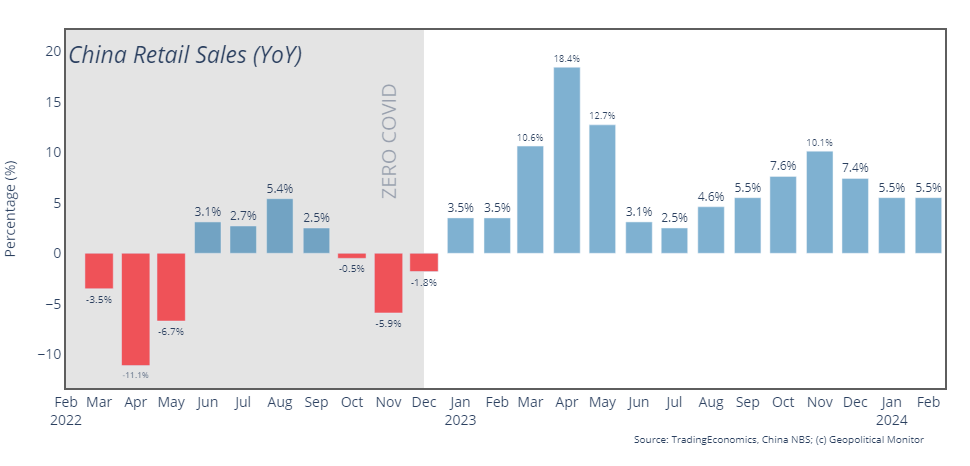

There was a widely held expectation that, once this transitory period was over, the Chinese economy would experience a boom much like the United States did after 2021, fueled by pent-up consumer demand and savings over the course of the pandemic. But the boom has yet to materialize; on the contrary, the listless post-COVID recovery has thrown long-term economic contradictions into even sharper relief, namely weak consumer spending, declining real estate markets, mounting debt burdens, and capital imbalances.

Now one quarter into the new year, China watchers are scanning for any sign of an economic inflection point, one where the doldrums of 2023 can be put squarely in the rearview mirror. Fortunately, the latest data is providing some much-needed fuel for the optimists.

Strong retail sales and industrial production to start the year

China’s economic performance in the early months of the year surpassed expectations, with retail sales increasing by 5.5%, outpacing the 5.2% growth predicted by analysts. This growth was accompanied by a significant 7% rise in industrial production, exceeding the forecasted 5% increase, and a 4.2% uptick in fixed asset investment, which also surpassed analyst expectations of 3.2%. Notably, online retail sales of physical goods saw a robust 14.4% increase from the previous year, signaling a strong consumer shift towards digital platforms.

The Chinese government seems to recognize the need for additional policy measures to achieve its ambitious growth target of around 5% for the year, particularly through demand-side interventions such as fiscal policy adjustments and efforts to boost housing and consumption. National Bureau of Statistics Spokesperson Liu Aihua highlighted ongoing domestic demand challenges, describing the economy as being in a critical period of recovery. Despite the festive boost from the Lunar New Year, which typically elevates economic figures for January and February, concerns remain regarding the sustainability of the (tentative) recovery we’re seeing in retail sales and overall consumer confidence. All told, neither has rebounded as strongly as anticipated post-pandemic, as described above.