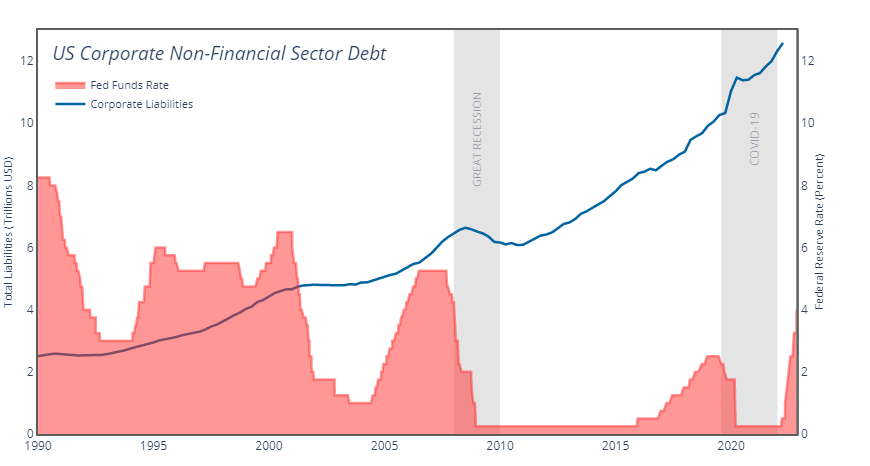

The COVID-19 era proved a mixed bag for the US corporate world: for those companies like Zoom or Peloton whose products were conducive to the new social reality, it was a boon, but for others it represented an existential challenge that could only be endured in the hope of better days ahead. In both cases, however, financing was freely available thanks to the Federal Reserve’s expansive monetary stimulus, whether deployed for debt consolidation, expansion, or simply survival.

Hence the surge in corporate borrowing through the early pandemic period, when firms took advantage of favorable rates and amassed significant new liabilities. In 2020 alone, nonfinancial companies issued $1.7 trillion in new bonds – nearly $600 million more than the previous high. One year later corporate debt accumulation exceeded its long-term trend line by over 10%.

Consequentially, US firms were saddled with historic debt loans when they entered the (tentative) post-COVID economic recovery, a period that represents a starkly different operating environment from the one which preceded it.

For one, the easy money once ensured by the Federal Reserve is gone, as we are now in the midst of a sharp tightening cycle that hopes to bring runaway inflation under control. The effect on borrowing costs has been predictable: investment-rated yields have more than doubled since 2020 and junk yields are hovering near 13-year highs. As a result, companies are increasingly having a hard time securing affordable financing, particularly small- and mid-sized operations.

It should be noted here that our picture of the US corporate debt outlook remains partial due to the nature of the COVID-era debt binge, when various major corporations secured long-term, low-rate financing that effectively insulated them from having to return to debt markets for the immediate future. New York Times cites Carvana as one such example: the yield on the used-car retailer’s long-term debt would be over 20% higher if it had to tap debt markets in the current climate. In other words, an untold number of corporations are simply hoping that the current headwinds blow over before their COVID-era (debt-fueled) war chest runs out.