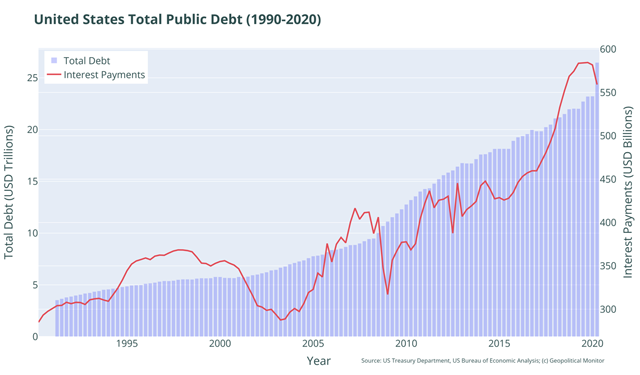

US federal debt levels are spiking, with debt-to-GDP projected to exceed 100% sometime next year. The current deficit, ballooned by federal stimulus from the COVID-19 pandemic, is expected to come in at 17.9% for FY 2020.

It’s hard to imagine this trend reversing itself anytime soon. Should an effective vaccine become widely available in the months ahead, the United States government will still have to contend with the economic headwinds of high consumer debt and unemployment, crumbling infrastructure, indebted state governments, and a dysfunctional global trade system – all of which will produce calls for more – not less – government spending.

Analysis

Comparable spikes of US debt in the past have been the result of wars, and are generally followed by stark deleveraging in a post-war growth boom. This was true of the Civil War, World War I, and World War II (which was directly preceded by the Great Depression).

Will the same be said of the COVID-19 pandemic of 2020? The following factors will tell the story:

- Domestic spending. Governments must grow out of their debt burdens in order to escape them, and the United States is no exception. One route is domestic spending, which accounts for around 70% of US economic activity. Domestic spending is a factor of jobs and discretionary income, the latter of which was being choked out by high consumer debt even before COVID-19 appeared. Student loans (which exceeded $1.5 trillion in early 2019) and auto loans are two ways through which low- and middle-income households were feeling the squeeze before COVID-19, and federal stimulus appears to be the only thing holding off a long-expected wave of delinquencies.

- Export markets. The last time the United States experienced debt levels like 2020 was in 1946, when debt-to-GDP hit a historic high of 106%. There are some significant differences between the global economy of then and now. Chief among them is the fact that in 1946, the United States stood alone as a manufacturing juggernaut, exporting to countries that were either war-torn and rebuilding or newly decolonized and in early stages of their economic development. With contemporary competitors like the European Union, China, Japan, and South Korea, the field of 2020 is much more advanced, and it’s unlikely that the rapid growth of the post-WWII period will be duplicated.

- Infrastructure. One characteristic of US federal spending in response to COVID-19 is that it heavily favors direct assistance to distressed individuals and corporations. And while this may have forestalled the wave of bankruptcies and evictions that would have otherwise occurred, these welfare payments don’t represent a good return on investment for the US government. US infrastructure on the other hand is in dire need of attention, and its advanced state of decay will impact the country’s growth prospects in the decades ahead (many ascribe the post-WWII growth miracle to the U.S.’ robust infrastructure networks at the time). How much is needed? The American Society of Civil Engineers (ASCE) put the infrastructure investment gap at $2 trillion by 2025 – that’s the amount needed just to maintain current levels of economic activity.

2012, modified, https://creativecommons.org/licenses/by-sa/2.0/")