All eyes will be on the US Federal Reserve this Wednesday. On that day, the Federal Open Market Committee is expected to wrap up one of its eight annual meetings to determine US monetary policy. The meeting is expected to wrap up with a press conference, and full minutes from the internal discussions will be released three weeks later.

Investors will be monitoring whether previous forward guidance holds the line amid changing economic conditions in the United States. Yet whatever the dot plot ultimately tells them might not prove so credible in retrospect.

Analysis

US monetary policy is highly consequential at the best of times. Billions of dollars in borrowing decisions are made on the basis of anticipating what the Fed will do, and its decisions impact markets all over the world, whether by unleashing hot money in search of higher yields in developing countries or impacting their borrowing costs via exchange rate fluctuations.

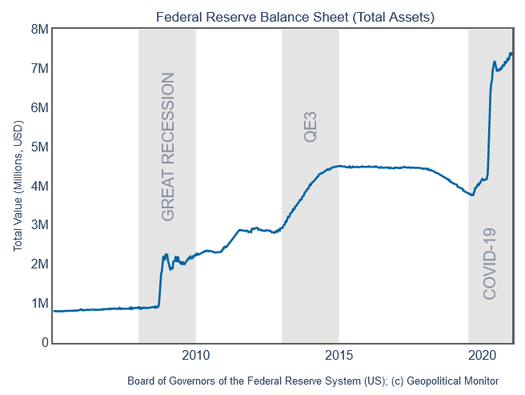

The Fed’s impact is even more pronounced at present owing to its asset purchases. It is buying up around $120 billion’s worth per month: $80 billion in 10-year Treasuries and $40 billion in mortgage-backed securities. With far more buying than tapering since the quantitative easing era kicked off in 2008, the Fed’s balance sheet currently stands at around $7.6 trillion. Roughly $4.9 trillion of this is US Treasury debt, and $2.1 trillion is mortgage debt.

We already have a good idea of the tone that will be set by this week’s meeting. Fed chief Jerome Powell will likely point to lingering uncertainties in the economy and stress the need to continue the asset purchasing program and maintain the Fed’s uber dovish forward guidance (the ‘dot plot’), which for the most part envisions no new interest rate hikes through 2023.