When is a taper not a taper at all?

When is a taper not a taper at all?

When it’s the European Central Bank doing the bond-buying. In a feat of quantum semiotics, the ECB inhabited two states simultaneously in its September 9th policy meeting statement: scaling back bond purchases to a “moderately lower pace” while also insisting, in the words of ECB president Christine Legarde, that “the lady isn’t tapering.”

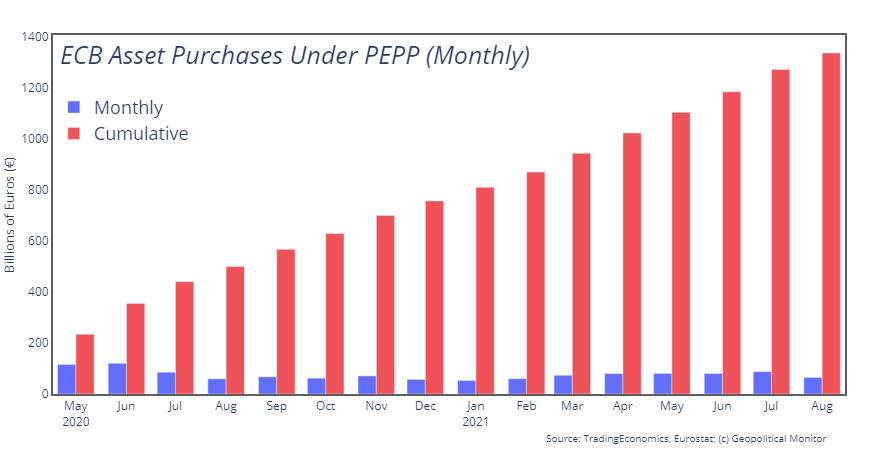

This non-taper taper tweaks bond-buying under the pandemic emergency purchase program (PEPP) from its current pace of around €80bn per month to the €60- €70bn range, according to estimates from Dutch Bank ING. PEPP was established in March 2020 with an overall budget of €1.85tn, with a target wrap-up date of March 2022. That end date remains locked in place, and PEPP has about €500bn left to disburse (enough for a pace of around €83bn per month).

The ECB’s decision comes against a backdrop of improving economic conditions across Europe and, as elsewhere, resurgent inflation as well. August inflation numbers have been surprising across the board: France posted a 2.4% rate, up from 1.5% in July; Spain posted a 3.3% rate, up from 2.9% in July; and Germany posted a 13-year high of 3.4%, up from 3.1% in July.

For its part, the ECB maintains that inflation is a temporary phenomenon. Though the central bank recently upgraded its medium-term inflation forecast, it still anticipates inflation below its target rate of 2% in 2022 and 2023.

Herein lies the logic underpinning the non-taper taper. Whenever a headline contains the words “Germany,” “inflation,” and “13-year high,” it’s safe to assume that monetary policy has become a political issue in Berlin. Herein lies the ‘taper’ part of the equation; or, a limited withdrawal of monetary stimulus in order to forestall the risks of runaway inflation, keeping the monetary hawks happy in Frankfurt.

The move places the ECB somewhat ahead of the curve in terms of developed central banks peers looking to pivot away from stimulus, many of which have indicated a willingness but stopped short of actually paring purchases (for example, the United States and Australia).

Then there’s the ‘non-taper’ part. Keep in mind that the ECB stands out among developed peers in that it was engaged in monetary stimulus before the COVID-19 pandemic, and is likely to continue stimulus measures long after the pandemic has eased, albeit not necessarily under the banner of PEPP. The ECB’s regular asset purchasing program, which hoovers up some €20 billion in bonds every month, remains operational and is expected to be ramped up as PEPP is wound down.

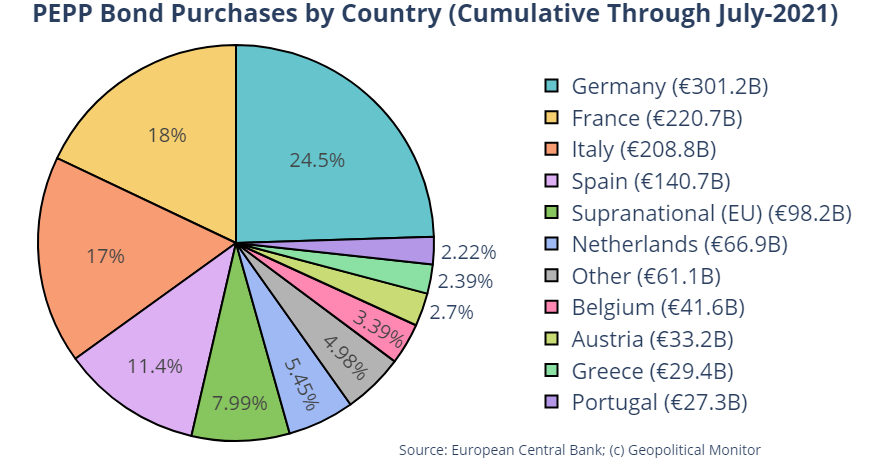

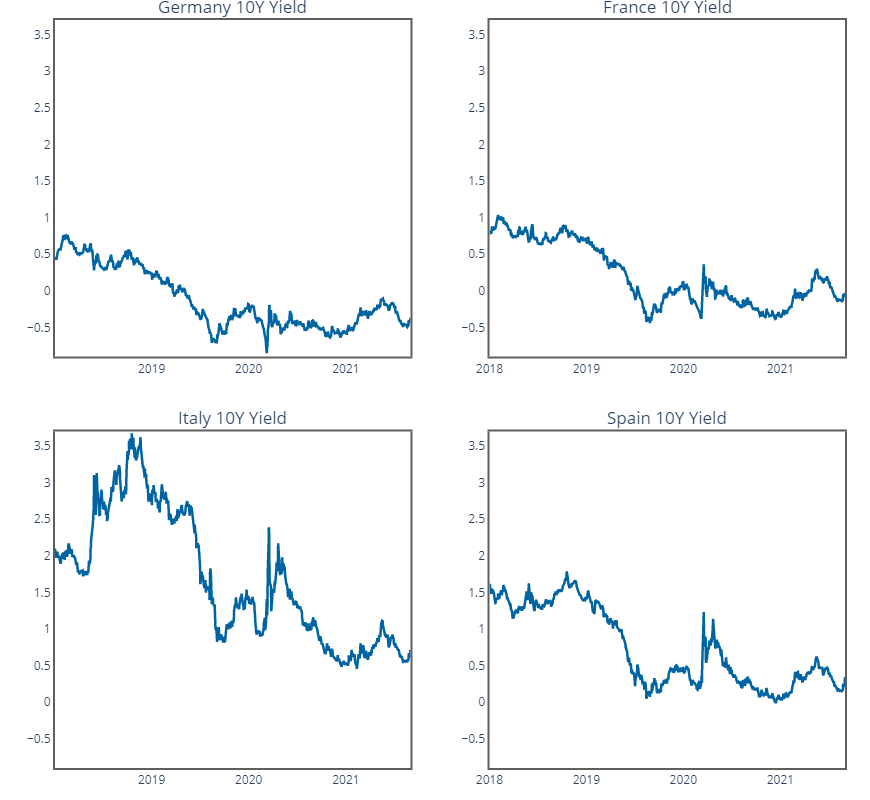

ECB bond-buying programs have carved out fiscal breathing room for Europe’s most indebted economies, depressing yields and facilitating easy financing. These fiscal pressures were conspicuous pre-COVID, notably in Italy, Spain, and Greece in the years following the EU sovereign debt crisis. Bond-buying and the “whatever it takes” era of ECB policy have made for a much more placid EU bond market; however, the situation could change in the blink of an eye if investors are given reason to question the ECB’s commitment to propping up distressed euro zone members (a dynamic that has effectively become a permanent stopgap solution for lack of any fiscal union among member states). Thus, deflationary risks aside, the ECB will always have an incentive to maintain market confidence and avoid the worst-case scenario of an out-and-out bailout ala Greece. Consequently, ECB bond-buying can be expected to outlast its developed peers, and ECB signaling will skew dovish at all times.

Thus, the lady isn’t tapering, even when she is.

, cc Benh LIEU SONG, Flickr, modified, https://creativecommons.org/licenses/by-sa/2.0/")