A recent article on the ECB noted the diminishing returns of ‘unconventional’ the monetary policies which, following the Great Recession, have paradoxically become a standard component of central banker toolboxes worldwide.

Some of these diminishing returns were on open display as US Federal Reserve Chair Jerome Powell held a news conference on Thursday. Despite what was by many accounts an extremely dovish outlook from the Fed, US traders still rushed to the exits and equity markets closed the session deeply in the red. It would seem that the old maxim of C. Northcote Parkinson – “A luxury, once experienced, becomes a necessity” – increasingly applies here.

Analysis

The vision laid out by Jerome Powell should have reassured investors who were worried about a premature tapering of stimulative monetary policy.

First and foremost, and to the surprise of no one, the Federal Reserve maintained its near-zero interest rate. Rates are widely expected to maintain their current historical lows through 2023.

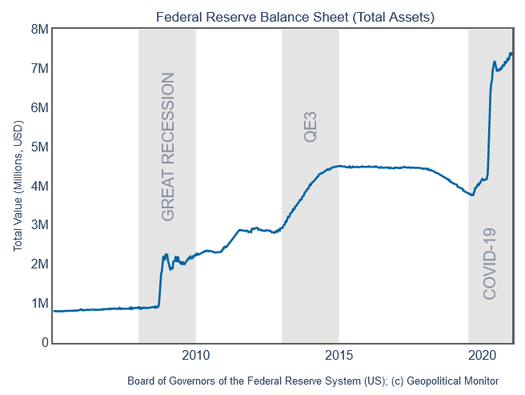

But most watchers were concerned with the fate of asset purchasing programs initiated at the onset of the COVID-19 pandemic. These include:

- Large-scale securities purchases. The Fed continues to operate a $180-billion bond-buying program, buying up $80 billion in Treasury securities and $40 billion in mortgage-backed securities every month. As of the week ending January 20, the Fed had $4.7 trillion worth of US Treasury securities on its balance sheet, and $2.1 trillion worth of mortgage-backed securities.

- Ad hoc support facilities. The Fed also runs a variety of targeted programs to support various sectors of the market, including the Municipal Lending Facility (a $500 billion program to buy up state and municipal bonds, thus depressing their borrowing costs); the Commercial Paper Funding Facility (a $250 billion program to purchase corporate debt); the Paycheck Protection Program Liquidity Facility (a program offering loans to small businesses to help pay labor costs during the pandemic); and the Money Market Mutual Fund Liquidity Facility (a program offering collateralized loans to US banks in order to shore up liquidity), among others. However, the weight of these ad hoc facilities on the Fed balance sheet is feather-light compared to security purchases.

Here Powell went through all of the usual motions to indicate that the Fed’s market interventions will persist; however, being that they’re predicated on economic benchmarks which are largely subjective, he could not commit to any firm timeline for a taper.

Hence some of the chair’s quotes: It will be “some time” before the threshold is met to alter asset programs; “[the focus] on exit is premature”; “we have not won this yet”; “[the US economy] is a long way from recovery,” etc.