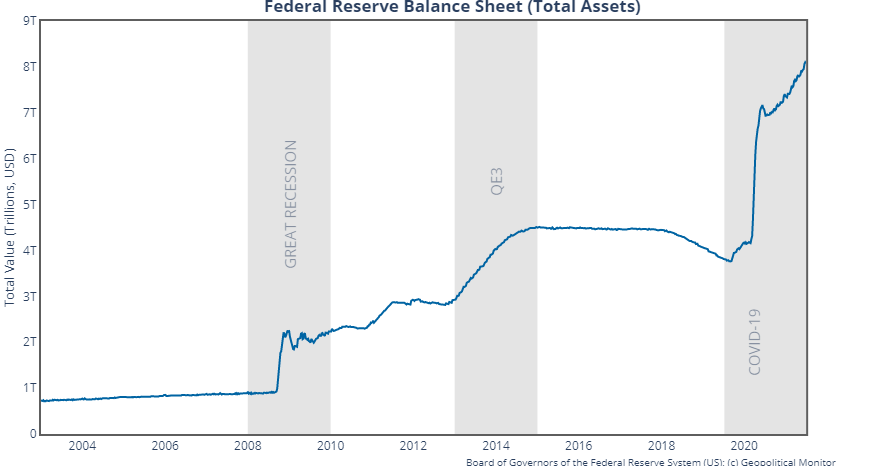

The Federal Reserve balance sheet was worth approximately $8.1 trillion in the final week of June, roughly the size of the economies of Japan and Germany combined. As of July 1, around $5.1 of these holdings took the form of US Treasuries, and another $2.3 trillion were mortgage-backed securities. Both totals continue to increase on monthly purchases by the Fed of $80 billion in Treasuries and $40 billion in mortgage-backed securities.

Other central bank assets include corporate credit facilities (worth $14 billion and now in the process of being wound down), and the Fed’s Main Street Lending Program (worth $16 billion), neither of which gained significant traction among borrowers during the economic shocks of 2020.

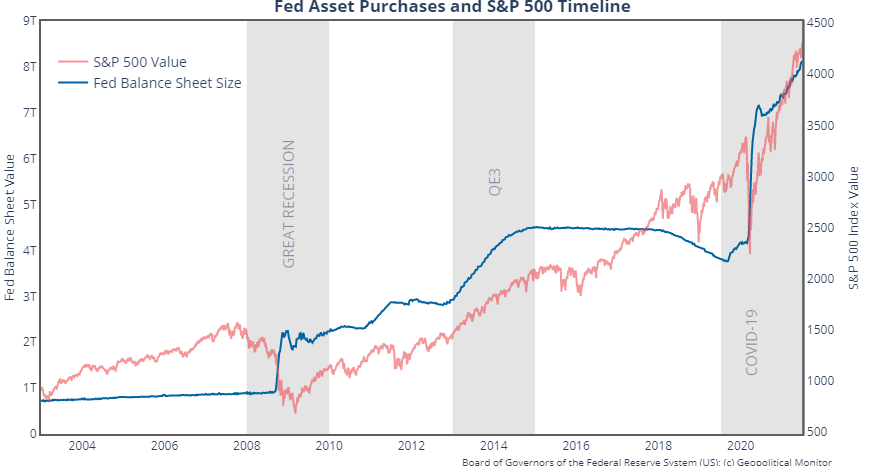

Divining the precise timing of the Fed’s decision to taper its monthly purchases, along with its preferred pace of monthly reductions, is a point of obsession among market watchers. Going by conventional logic, the taper will deflate bubbles in riskier assets such as equities and pave the way toward a wider normalization of interest rates (though some may disagree). Yet a fully consummated taper process will only curb the growth of the Fed’s balance sheet. Far less attention is paid to the question of what to do about the $8.1 trillion worth of assets that the Fed already ‘owns.’ These assets will either need to be sold off, risking severe market disruptions, or be allowed to gradually mature without the proceeds being reinvested (some $2.1 trillion of the Fed’s Treasuries will mature over five years in the future).

A winding down of the Fed’s overall balance sheet is easier said than done, as testified by the fact that, for the most part, said balance sheet has only known expansion since quantitative easing was first attempted in 2008. Former Fed chair Ben Bernanke has argued that a larger balance sheet should become the new normal, as it affords the central bank more tools in managing the money supply (two important qualifications being that this argument was made in 2016, when the balance sheet was half of its current size, and that the hypothetical balance sheet envisioned by Bernanke would be composed of Treasuries with short-term maturations, which is not the case currently). Others disagree, pointing out that the present balance sheet – which effectively represents an expansion of the money supply – is creating more money than banks can put to effective use; moreover, they’re choosing to plow excess funds back into US Treasuries rather than loan them out into the real economy. According to Bloomberg, bank surplus liquidity has increased from $300 billion in 2009, to $3.21 trillion at the dawn of 2020 (pre-COVID), and now to $6.74 trillion.

Looking ahead, we can count the Fed’s balance sheet as another unknown entity in the evolving landscape of global finance, one that by its gargantuan size alone will lend itself to unforeseen shocks along the winding road to normalization.

")