As one of the world’s most traded commodities, soybeans are a critical feature in the global agricultural landscape. Movement in soy futures can influence the stability of different countries: shaping trade policies, impacting diplomatic relations, and determining domestic stability through the movement of key input prices. Countries like the United States, Brazil, and Argentina, which are leading soybean producers, often leverage their production capacity as a significant economic asset, affecting global supply chains and price dynamics. On the other side, major importers like China, whose massive demand for soybeans stems from its vast hog sector, view soybean imports through the geopolitical lens, ascribing the commodity critical importance for food security and agricultural policy. This geopolitical significance was evident during the US-China trade war, as soy was one of the first commodities targeted for sanctions in 2018.

Recent Trends

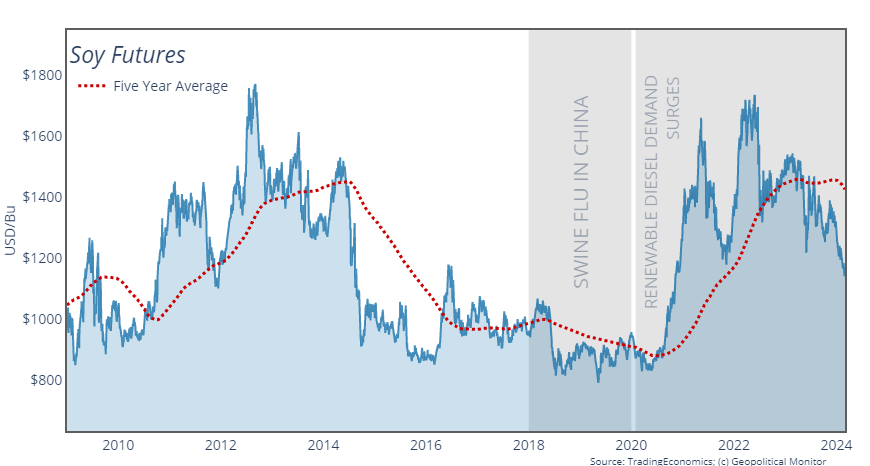

Over the past six months, several factors have significantly influenced soybean prices in what is considered overall to be a bearish market.

On the supply side, recent harvest in two major producers – Brazil and the United States – have been strong, though drought and unseasonably hot weather are beginning to impact yields in Brazil. As for the United States, according to a recent update US soybean export sales experienced a notable surge last week, marking the first time since November that sales exceeded trade expectations. Yet this uptick does not fully reflect an overall diminished interest from global buyers in US soybeans over the past few years. The US Department of Agriculture (USDA) has forecasted that for the 2023-24 season, domestic exporters are on track to ship the second-lowest volume of soybeans in a decade. And despite some optimism in the wake of recent sales numbers, the projection might still be overly optimistic.