Global geopolitical trends we’re tracking this week:

Key Dates

June 7 – China year-on-year import and export data for May.

June 7 – China trade balance for May.

June 7 – Japan Q1 GDP data.

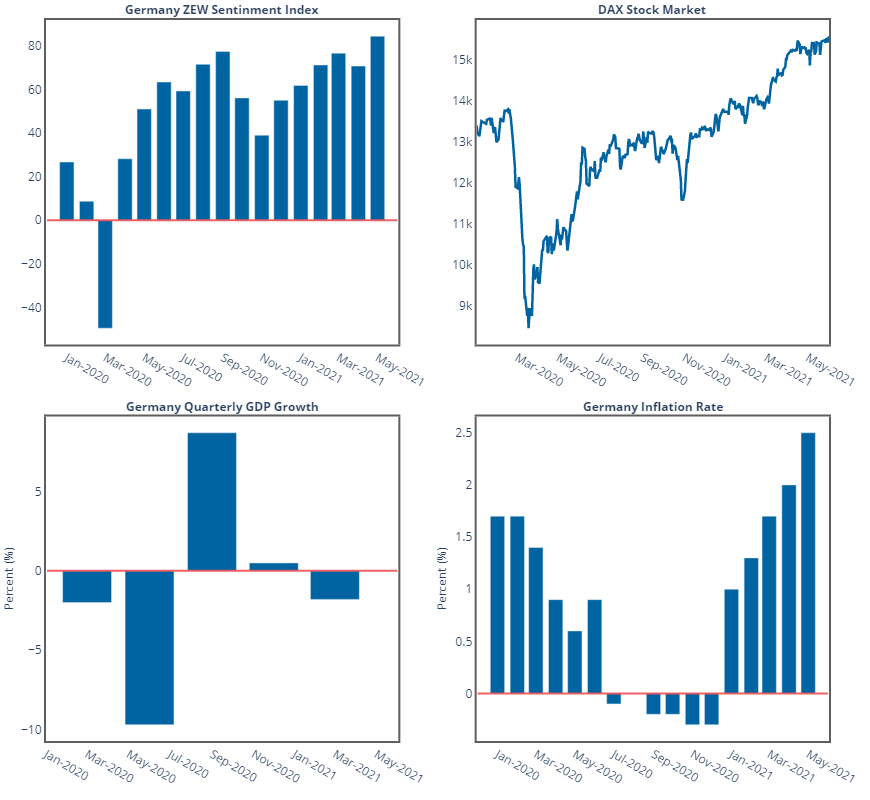

June 8 – Germany ZEW economic sentiment gauge. Investors will be looking for the six-month confidence gauge for the velocity of Germany’s economic recovery. A positive result denotes optimism, and the May reading approached a record high with 84.4.

June 8 – US Bureau of Labor Statistics JOLTs job survey.

June 8 – China consumer price index (CPI) and producer price index (PPI) for May. The question here will be whether prices in China reflect an ongoing inflationary trend in major economies. The PPI merits closest attention, as it was already surging in April (6.8% year-on-year) compared to a relatively modest 0.9% YoY increase in April CPI.

June 9 – Mongolia presidential election.

June 9 – Brazil ICPA inflation data for May.

June 9 – Bank of Canada interest rate decision and press conference. With inflation ticking upward and an economy buoyed by surging commodity prices, Canada is well-placed to lead its developed peers out of the QE wilderness of the COVID-19 pandemic. Dovish notes abound in signaling from the Bank’s previous meeting in April, where it began to taper its bond-purchasing program, and the economic data has only become more supportive of a hawkish turn since then. The consensus expectation is for more tapering, and we could see hints of an interest rate hike ahead of the previous schedule of second half 2022.

June 9 – US crude oil inventories.

June 10 – ECB interest rate decision and press conference.

June 10 – US CPI for May. With food and energy prices on the rise, public health restrictions in the rearview mirror, and employment roaring back to pre-pandemic levels, CPI data for May will help to determine whether the recent inflation surge is a lingering affair or not, particularly the month-on-month numbers.

June 10 – US Initial jobless claims.

June 11 – UK manufacturing and industrial production for April.

June 11 – US Baker Hughes oil rig count.

June 11-13 – G7 Leaders Summit in United Kingdom.

June 12 – Algeria parliamentary election.

World

COVID-19 fast facts

- After a series of missteps in its initial rollout, the EU has now administered at least one dose of vaccine to 40% of its population; in the United States and the UK, over 40% of the population is fully vaccinated. However, coverage rates are underwhelming in the developing world: Brazil has administered one dose to 22.8% of its population, and is progressing at a rate of approximately 550,000 per week; India 13.3% (2,700,000 per week); Turkey 20.8% (212,659 per week); Mexico 18.2% (628,000 per week); Pakistan 1.8% (269,500 per week); and the Philippines 3.7% (156,000 per week), as per the Bloomberg vaccine tracker. This all points to an increasing likelihood of a starkly bifurcated global economic recovery in Q2 2021.

- Worsening outbreaks among emerging economies include: Malaysia (two-week average of 7,658 daily cases), Thailand (3,563), Chile (7,138), Colombia (25,068), Mongolia (1,051), and Tunisia (1,479).

Europe

Brussels takes aim at multinational tax avoidance

The EU has hammered out a deal that will force multinational companies to disclose their tax reporting practices, exposing the common practice of profit-shifting to low-tax jurisdictions to greater public scrutiny. According to the new rules, any corporation with global revenues of over €750 for two consecutive years must disclose how much tax they pay in each EU state as well as the 19 tax jurisdictions on the EU’s list of “non-cooperative” tax authorities. The deal, which is the result of over eight years of negotiations, is regarded as a positive step toward achieving international tax transparency; however, it has also been criticized for narrowing its focus to EU and EU-listed authorities, which excludes some 80% of world governments.

Africa

Bloody border raid points to deteriorating security outlook in the Sahel

At least 100 civilians were killed in a village in northern Burkina Faso over the weekend, near the border with Niger. Though there has been no claim made for the attack, suspicion has fallen on Islamic terrorist groups such as al-Qaeda and Islamic State in West Africa (ISWA). This latest violence, which comes on the heels of another brutal attack that killed 137 Malian villagers in March, reflects a security outlook in the Sahel that is broadly deteriorating. The situation is further complicated by the recent coup in Mali, which risks provoking new sectarian conflict, and has now resulted in both the African Union and the Economic Community of West African States (ECOWAS) suspending Mali, and France cancelling its joint military operations with the Malian armed forces. A more permanent pullout of French forces operating in the Sahel now appears to be a distinct possibility, as alluded to last week by President Macron.

Middle East

Israel gets a new government, but for how long?

The Israeli opposition has cobbled together an ideology-spanning coalition that’s intended to replace long-serving premier Benjamin Netanyahu. The government will be headed by Naftali Bennet of the ultra-nationalist Yamina party, it will be composed mostly of Lapid and the remnants of Israel’s secular left, and its razor-thin majority will be sealed by the inclusion of Mansour Abbas’ Islamist list, which split from the Joint List of Arab parties earlier this year.

Obviously, this is a government that is not long of this world; however, it might not even last long enough to achieve its central goal of ushering Netanyahu from the premiership to his corruption trial. The former premier and his right-wing allies are employing a full-court press against Bennet and his Yamina party, branding them as traitors and even encouraging supporters to picket outside their homes. The pressure has already yielded one defection from Yamina MK Amichai Chikli. One additional defection is all that’s required to deprive the new government of the votes needed to be sworn in.

A naval showdown in the making in the Americas?

Two Iranian warships appear to be heading across the Atlantic, suggesting that Tehran is intent on following through on a longstanding threat to send warships into the Western Hemisphere. The goal of the voyage is unclear. It could be a symbolic demonstration of the blue water capabilities of Iran’s navy, or there could be some more tangible strategic objective involved. One possibility is that the ships are making a weapons delivery to Venezuela. In late 2020, US military officials cited a “growing Iranian influence” in Venezuela, including weapons sales. Whatever the ultimate motivations, should the vessels make their way to Venezuela, a naval stand-off or even clash with the US navy would be the most likely result. Pentagon spokesperson John Kirby suggested just such a possibility when asked about the ships, stressing that the United States reserves the right “to take appropriate measures… to deter the delivery or transit of such weapons.”

Data Snapshot

Economic sentiment remains buoyant in Germany, where widening vaccination coverage and re-openings are setting the stage for a growth comeback over the second half of 2021: