Global geopolitical trends we’re tracking this week:

Key Dates

October 25 – Germany IFO Business Climate Index for October.

October 25 – Singapore Consumer Price Index (CPI) for September.

October 26 – Bank of Japan CPI.

October 26 – Conference Board consumer confidence index for October.

October 26 – US new home sales for September.

October 26 – API weekly crude oil stock.

October 26 – New Zealand trade balance for September.

October 26 – Australia CPI for Q3.

October 26 – China industrial profit for September.

October 26 – ASEAN three-day leaders’ summit opens (videoconference).

October 27 – US core durable goods for September.

October 27 – Bank of Canada monetary policy report, rate decision, and press conference. An expectation-beating 4.4% inflation reading in September – fueled in large part by rising oil prices – has increased pressure on Canada’s central bank to pivot toward monetary normalization. However, the consensus opinion is that the bank will hold off on hiking rates until next year, after which we’re likely to see a string of consecutive hikes.

October 27 – US crude oil inventories.

October 27 – Japan central bank monetary policy statement and interest rate decision.

October 28 – Germany unemployment for October.

October 28 – ECB interest rate decision.

October 28 – US GDP data for Q3.

October 28 – US initial jobless claims.

October 28 – Japan CPI for October.

October 28 – Japan industrial production for September.

October 28 – Australia retail sales.

October 29 – France GDP for Q3 and consumer spending for September.

October 29 – France CPI for September.

October 29 – Spain GDP for Q3.

October 29 – Germany GDP for Q3.

October 29 – Italy GDP for Q3.

October 29 – Italy CPI for October.

October 29 – Euro zone CPI for October. This is an interesting one to watch: year-on-year inflation hit 3.5% in September, and expectations are for another 3.7% increase over October. Both are well in excess of the ECB’s 2% annual inflation target, and with oil prices hovering near multi-year highs, it appears as though inflationary forces will not be receding anytime soon.

October 29 – Mexico GDP for Q3.

World

COVID-19 fast facts

- COVID-19 cases and deaths decreased 4% and 2% respectively over the course of the week, according to the World Health Organization’s latest situation report. Notably, Europe was the regional exception, as it recorded a 7% increase in new cases.

- Namibia announced that it would be suspending use of Russia’s Sputnik V vaccine after regulators in South Africa declined to approve the vaccine, citing a failure on the part of the manufacturer to provide necessary information.

- Russia’s COVID-19 outbreak is hitting record levels, with 37,678 new cases on Saturday and 1,075 deaths. Schools, stores, and restaurants are expected to close as Moscow enters a two-week lockdown.

Upcoming G20 summit split on coal, climate pledges

Climate issues will loom large at the upcoming G20 summit, scheduled for October 30 in Rome. The G20 summit will open just one day before the UN Climate Change Conference (COP26), which will run for the first two weeks in November. According to Reuters, representatives from India and China are refusing to commit to carbon neutrality or the 1.5 Celsius warming target, citing unkept promises by developed countries to provide the necessary financing for green transitions. With some highly notable no-shows expected for the meeting, including Russia’s Vladimir Putin and China’s Xi Jinping, it seems highly unlikely that the G20 summit will produce any diplomatic breakthroughs.

Asia

Myanmar junta left out of ASEAN leaders’ summit

When a three-day ASEAN leaders’ summit begins this week, it will do so without a political representative from Myanmar. The decision to not allow the junta, led by General Min Aung Hlaing, to attend is exceptional for a regional organization that prides itself on consensus-building and non-interference in internal affairs (‘the ASEAN way’). Elsewhere, the United Nation’s special rapporteur on Myanmar has warned that troops are amassing in the north of the country, evidently in preparation of a major attack on ethnic enclaves along the border. Myanmar’s National Unity Government, a shadow government formed by politicians and members of the National League for Democracy (NLD), issued an open call for armed resistance against the junta in September.

Evergrande lives to fight another day

Troubled property developer Evergrande made a $83.5 bond payment ahead of the expiration of a 30-day grace period on October 23, avoiding a default. With some $191 million in other outstanding bond payments, however, the company’s reprieve may ultimately prove to be short-lived. The next payment due is $47.5 million on October 29 (deadline for expiry of a previous 30-day grace period), followed by a series of other payments due in November and December. Elsewhere, the company is attempting to shore up investor confidence by resuming work on 10 stalled development projects in six different cities across China.

China’s delta COVID-19 outbreak expected to worsen

China reported 26 new local COVID-19 infections on Saturday, with the current outbreak now accounting for over 130 cases in 11 provinces – including the capital of Beijing. The mounting pace of spread recently prompted the National Health Commission to warn that the worst is likely still to come. Most of the cases have been linked to domestic tourist groups; however, around 20% of infections have no known origin, which suggests transmission chains that are going undetected. The outbreak comes as the Chinese economy is already contending with a power crunch and a slowdown in the critical real estate sector.

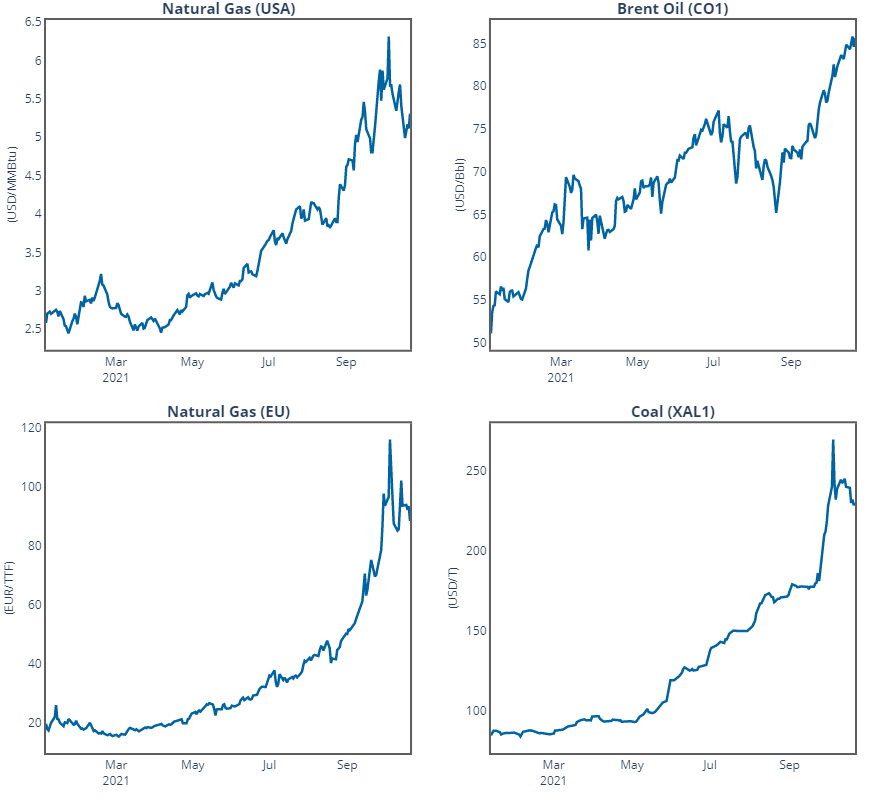

Data Snapshot

Central bankers around the world are responding to inflation and the prospect of US tapering with various levels of urgency: