Average yields on US junk-rated debt dipped below 4% for the first time ever this week, ushering in a new wave of issuance as corporations move to secure financing under such favorable market conditions.

Some $32 billion in new corporate borrowing has already been recorded in 2021, a 35% higher rate than the same period last year (not particularly surprising given the contrasting financing climate). The issuance thus far suggests a continuation of the fervent pace of 2020, when over $547 billion worth of financing was raised by junk-rated companies – over 30% higher than the previous year, and at much more favorable yields.

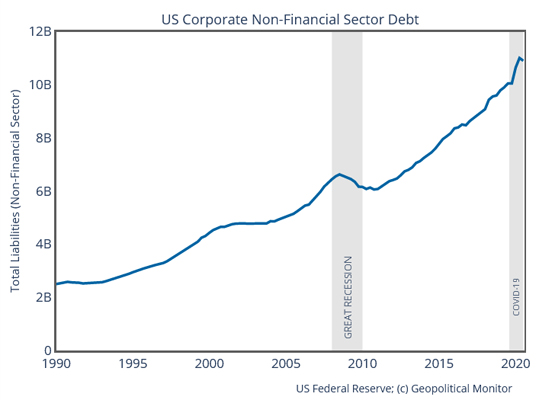

Overall, S&P Global projects the corporate debt market to drop to around $8 trillion this year, down 3% from 2020.

Two factors are fueling rapid debt accumulation among corporations in the U.S. and elsewhere. First is the highly favorable financing conditions maintained by central banks; interest rates continue to hover at near-zero or sub-zero levels and price floors are being imposed via mass asset purchases throughout the developed world. Second is the lack of alternative options for investors searching for yield. With stocks venturing into overpriced territory and sovereign yields returning a pittance, investors are turning to ever riskier assets like junk-rated debt and crypto.

The result has been a run on junk-rated debt, which has in turn depressed yields to historic lows. According to analysis from JPMorgan Chase & Co, over 58% of the market is now trading at a yield of under 4%. The 2.25% that T-Mobile secured in its $1 billion issuance in January was lower than what 10-year US Treasuries were paying at the onset of 2019. Even average yields in the CCC tier are hovering around the 7% mark – the lowest they’ve been in the past 20 years.

Pessimists will argue that the current rate of debt accumulation is unsustainable and represents a case of market euphoria overshadowing economic reality. These companies are after all junk-rated for a reason, whether due to pre-existing debt piles or dismal growth prospects, and the investors who decide to front them money are not receiving much in the way of a premium on the risk they’re taking on. Moreover, there’s several assumptions being made – that central bank support and low interest rates will persist, that vaccines will effectively remove COVID restrictions sometime this year, that the spread of COVID-19 variants won’t upend public health planning, and that many of those who lost their jobs during the pandemic will be rehired in the recovery. Should any combination of these assumptions ultimately not hold true, then investors could stand to lose out, and depending on the extent of the reckoning it could seriously impact the ability of heavily indebted and underperforming corporations to secure financing lifelines in the future.