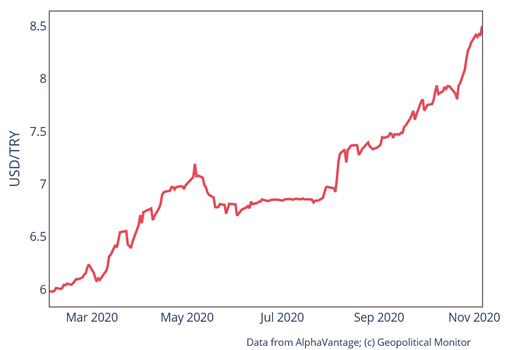

Amidst a post-election surge in emerging market currencies around the world there remains one conspicuous outlier: Turkey’s lira.

Unlike peers in Brazil, Russia, and Mexico, the lira was testing new lows of 8.5445 against the US dollar last week on news of a possible Biden victory and divided congress.

The currency is now down around 30% this year.

A new currency crisis in the making?

The threat of a currency crisis in Turkey is nothing new; in fact, since the lira’s meltdown in 2018, currency volatility has emerged as a consistent feature of the Turkish economy.

What’s behind this consistent pressure on the lira? Some of the causes are structural and stretch back several years.

One is the country’s longstanding current account deficit, which reflects a prolonged sapping of domestic capital stock. As a percentage of GDP, Turkey ran major current account deficits from 2011 onward. Last year marked a rare anomaly of a current account that was above water – 1.17% of GDP – thanks to a barrage of government policies to combat capital flight. This year however saw a resumption of the previous trend of deficits, and the country has now recorded a 12-month rolling total of $23.3 billion deficit (which captures the dip in the final months of 2019).

The inevitable result has been a decline in the foreign exchange reserves of the Central Bank of the Republic of Turkey (CBRT). Reserves have now reached a 20-year low of around $44.9 billion (as of early September). These levels have prompted warnings from Moody’s, first in 2019 and then again in 2020, when the ratings agency warned that Turkey had “depleted the buffers that would allow it to stave off a potential balance-of-payments crisis.”

Disconcerting though they already are, these foreign reserve numbers don’t tell the complete story. For the past year the central bank has been drawing an increasing proportion of its funding from the domestic banking system rather than the more conventional global sovereign debt market, fortifying its balance sheet with currency swaps and capital reserve requirements from domestic banks. Consequently, not only is the true extent of CBRT’s available liquidity obscured, but the Turkish banking system is also exposed to systemic risk through its financing of CBRT support actions and other government spending priorities (via the fact that these banks hold some $30 billion worth of Turkish Eurobonds).