Geopolitics Weekly contextualizes emerging geopolitical trends around the world, distilling the cacophony of global events into one easy reader. It lands in the inbox of Geopolitical Monitor subscribers every week. This week’s edition has been made available to all our readers.

North America

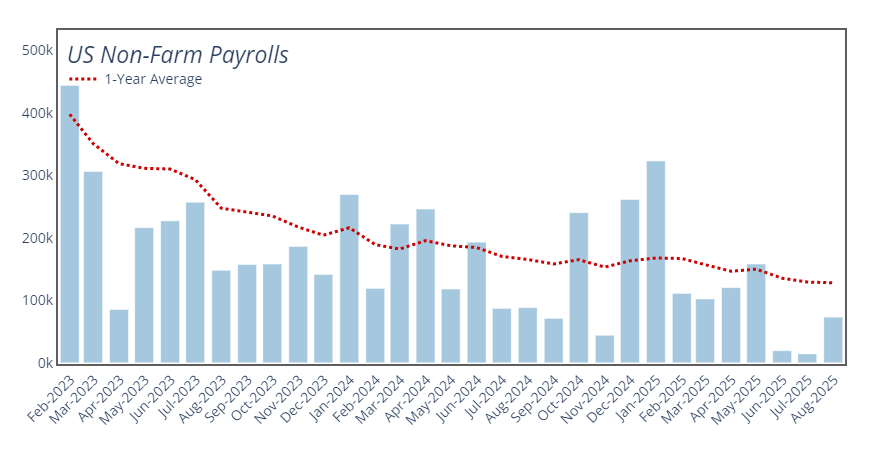

Signs of Softness Emerge in US Economy

What Happened

US nonfarm payrolls rose by 73,000 in July, coming in below the already conservative consensus estimate of 110,000. But there’s skepticism over whether even this relatively bleak figure will stand given the steep downward revisions of previous months that accompanied its announcement: May down from 144,000 to 19,000, and June down from 147,000 to 14,000. In one fell swoop, some 258,000 US jobs disappeared into the statistical ether.

Why It Matters

The numbers are starkly different – 515,000 new jobs over three months compared to 106,000 – and they provide two views of the health of the US economy. A large share of the downward revision comes from job losses in federal and local government jobs (unsurprising in the context of DOGE cuts) and administrative support and services (presumably AI and automation).

Taken in their final form, the numbers reflect a significant dip from previous months, and one that may flip the script on the US economy. President Trump has quickly moved to politicize the new data, firing the Bureau of Labor Statistics (BLS) Commissioner and calling the accuracy of the revised numbers into question. This will harm market confidence in BLS data going forward, and potentially even more so depending on who the Trump administration taps as a replacement.

If the BLS nonfarm payrolls numbers are unreliable, it follows that the CPI numbers also merit a second look. The agency is known to be grappling with a staffing shortage that is impacting its ability to collect price data, forcing it to simply estimate the prices for an average 15% of the goods it tracks. Given the current political climate, it’s no great leap to assume some degree of bureaucratic pressure to ensure these estimates come in on the downside.

If the BLS nonfarm payrolls numbers are unreliable, it follows that the CPI numbers also merit a second look. The agency is known to be grappling with a staffing shortage that is impacting its ability to collect price data, forcing it to simply estimate the prices for an average 15% of the goods it tracks. Given the current political climate, it’s no great leap to assume some degree of bureaucratic pressure to ensure these estimates come in on the downside.

The growth-inflation tug-of-war will resonate in the ongoing drama at the Federal Reserve. If there’s any silver lining in the revisions for President Trump, it’s that they increase the likelihood of a rate cut in September. A willingness to cut rates was evident in the Fed’s most recent meeting, where two members of the Board of Governors voted to cut citing softness in the labor market, the first such dissent since 1993. But given that US inflation was moving in the wrong direction in June – with a year-on-year CPI reading of 2.7%, up from 2.4% the month previous – nothing is assured.

New Wave of Trump Tariffs Roll Out

What Happened

On July 31, the Trump administration unveiled the ‘Further Modifying the Reciprocal Tariff Rates’ executive order, setting a new tariff rate for 66 trading partners. As the name implies, the order is just the latest shimmy from the moving target of US trade policy, producing confusion and alarm in capitals around the world. Notably, these tariffs will not actually go into effect until August 7, so the door is still open for last-minute negotiations and reversals.

Why It Matters

Tariffs on the schedule range from Brazil’s relatively low 10% (in addition to the 40% linked to the Bolsonaro trial) to Myanmar and Syria’s 40-41% (two countries that have no real US trade relationship to speak of). Some other notable trading partners in the order include:

Taiwan (20%). President Lai is arguing that the 20% rate is temporary, and that a deal is close There’s reason to believe that this is might be the case given the geopolitical and economic importance of Taiwan; something closer to the 15% recently secured by Japan should be doable. If the final deal is overly punitive, it will provide an opening to members of Taiwan’s pro-China legislature – newly emboldened by a failed recall movement – to push for closer cross-Strait economic relations.

Canada (35%). US-Canada trade negotiations continue to be framed in terms of national security, with President Trump hiking Canada’s base tariff rate from 25% to 35% on August 1 on the basis of combating cross-border fentanyl traffic (in reality, fentanyl seizures by the US Border Control at the Canadian border represented just 0.1% of fentanyl seized from 2022-2024). Trump seems to be singling out Canada out in particular throughout his second term, whether it be the overt threats of annexation or driving a harder negotiating position than with fellow CUSMA partner Mexico. In the Carney administration, we’re seeing a willingness to push back, with the Canadian team at one point reportedly considering walking away from the floundering talks. This hardball approach is increasingly supported by the Canadian public. Yet the stakes are not yet as high as they could be: the Trump reciprocal tariffs don’t cover CUSMA-compliant goods, which account for around 86% of Canadian exports (so long as the exporters do the necessary paperwork). These issues will come to the fore in July 2026, when CUSMA is up for its six-year review. As of Monday, Trump and Carney are expected to speak directly within the next few days.

India (25%). India’s base tariff level remains at the ‘Liberation Day’ peg of 25%, with President Trump also recently threatening an additional, “unspecified penalty” should India continue to purchase oil and weapons from Russia. Unsurprisingly, the Modi administration has pushed back on the idea, as Russia is a key supplier that now makes up approximately one third of the country’s oil imports. It remains to be seen whether President Trump follows through on the threat, but it’s clear that US-India relations have deteriorated since the Vance trip in April, when there was hope that India would be one of the first major economies to reach a trade deal.

European Union (15%). Brussels can expect a more favorable tariff rate thanks to last week’s US-EU tariff deal, but the saga doesn’t end there. One, there is still confusion surrounding the implementation of the deal, particularly surrounding which sectors are granted strategic exemptions to the 15% rate. Two, political blowback against the deal continues to mount across the bloc, with EU capitulation being the common lament. And three, the resulting text falls short of being authoritative: key aspects have yet to be codified (steel quotas, spirits, for example), and the official EU explainer makes pains to note that the agreement is not legally binding. Elsewhere, some have argued that EU Commission President Ursula von der Leyen overstepped her legal authority in pledging hundreds of billions in new investments in the US economy.

Europe

President Trump Dispatches Nuclear Subs toward Russia

What Happened

President Trump ordered two US nuclear subs to be positioned in “appropriate regions” in a direct response to inflammatory messages from Dmitry Medvedev, the former Russian president and current deputy chairman of Russia’s Security Council, a top-level advisory body on issues of national security.

Why It Matters

This might be the first time that President Trump has paid close attention to Dmitry Medvedev, but these comments are par for the course for the Russian firebrand. The tweet in question is actually tame in comparison to previous ones; for example, his typical refrain of a looming World War III. High-level US officials typically do not engage with Medvedev rhetorically let alone enact policy based on his tweets. Trump’s order itself is not tactically significant; the US Navy’s Ohio Class submarines are already at sea in service of the US nuclear triad. But the move by Trump does advance the recent theme of a hardening line on Russia, also evident in recent trade threats against India, moving up the deadline for Russia to engage in good-faith moves to end the fighting in Ukraine (which incidentally precipitated the Medvedev tweets in the fight place), and threatening new secondary sanctions and tariffs on Russia. The deadline for Russia to take these steps is currently August 7 or 9, depending on which of the ’10 or 12 days’ President Trump opts to go by.

/ modified, cc Trump White House, https://www.flickr.com/photos/whitehouse45/40884405043")

, https://flickr.com/photos/whitehouse45/35450047340/in/photolist-W1AL1L-2gnWmSz-2gmkqij-U9k7M7-U9k7Jb-2gmjWB6-2gmjX5W-2gnWmNG-UK3xEC-2gnWHBS-2gnWHsi-2gnWmrz-EgS4Ej-2gnWkXy-2gnWHEH-2gnWkYL-2gnWmuL-2gnWmzF-2gnWmf7-2gnWHt5-RXfeXy-SXNevY-2mwvfR9-2hKQjnT-2aLo7T6")