Niobium stands apart from the critical minerals dominating current headlines. Its supply vulnerability stems not from Chinese export controls but from geographic concentration and monopoly power held by Brazil, which produced 93 percent of the world’s niobium in 2024, with one privately held company, CBMM, controlling approximately 77 percent of global market share.

The United States has not produced niobium domestically since 1959 and imports 100 percent of its consumption, valued at approximately $525 million in 2025.

Nobium Background

Niobium is a soft, ductile transition metal whose defining property is its capacity to strengthen steel at remarkably low concentrations. Added at just 0.02 to 0.10 percent by weight, niobium raises yield strength while simultaneously improving toughness and weldability.

It achieves this through grain refinement, the only strengthening mechanism in metallurgy that improves strength and toughness concurrently rather than trading one for the other. The result is high-strength low-alloy (HSLA) steel that is 20 to 30 percent lighter than equivalent carbon steel structures, with applications spanning oil and gas pipelines, automotive bodies, bridges, high-rise construction, and shipbuilding.

Approximately 77 percent of US niobium consumption flows into steelmaking, primarily as ferroniobium. Superalloys account for most of the remaining 23 percent, serving as an input to jet engine turbine components, with smaller volumes supporting niche applications in superconducting magnets, electronics, and optics.

Figure 1. U.S. niobium end-use breakdown, 2024. Source: USGS Mineral Commodity Summaries 2026.

An emerging application with potentially transformative demand implications is niobium-titanium oxide (NTO) anodes for fast-charging lithium-ion batteries. CBMM has pursued this through partnerships with Toshiba and Cambridge-based Echion Technologies.

In June 2024, CBMM and Toshiba unveiled the world’s first prototype electric bus powered by NTO batteries, which enable 80 percent charge in 10 minutes with an estimated 15,000-cycle life. CBMM also invested $80 million in a 3,000 tonne-per-year battery-grade niobium oxide facility commissioned in 2024, with plans to scale to 20,000 tonnes by 2030.

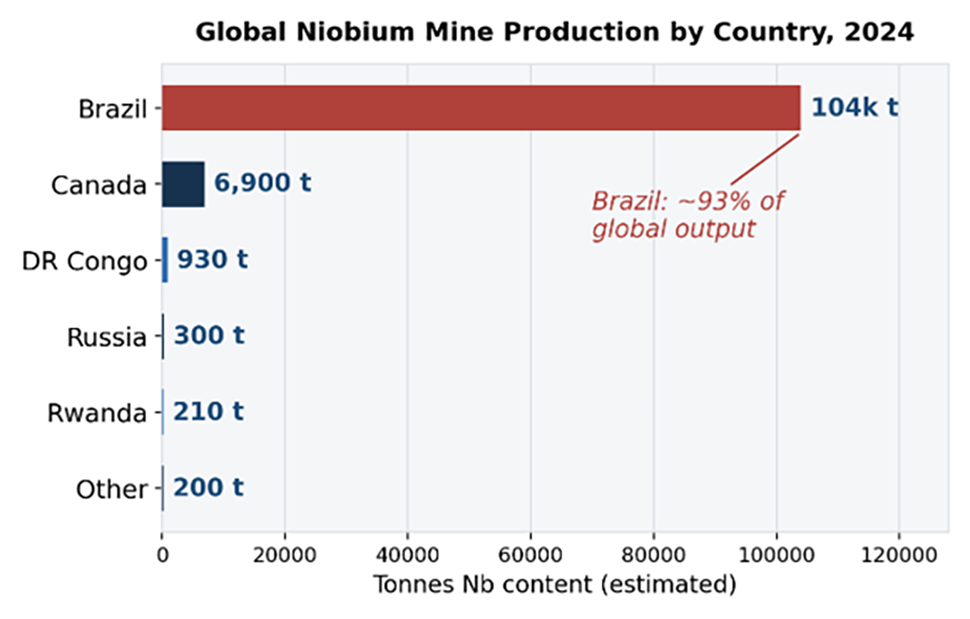

Figure 2. Global niobium mine production by country, 2024 (estimated). Source: USGS Mineral Commodity Summaries 2026.

Global Niobium Supply Chain Dynamics

Global niobium mine production reached an estimated 112,000 tonnes in 2024. Brazil produced 104,000 tonnes, or approximately 93 percent of the world total.

Canada contributed 6,900 tonnes from the Niobec underground mine in Quebec, operated by Magris Resources. The Democratic Republic of Congo produced 930 tonnes, Russia 300 tonnes, and Rwanda 210 tonnes.

US apparent consumption reached an estimated 9,340 tonnes in 2024, with net import reliance at 100 percent. Import sources over the 2021 to 2024 period were Brazil (67 percent), Canada (28 percent), and other countries (5 percent).

Table 1. Major Global Niobium Producers

| Company |

Location |

Output (2024) |

Ownership |

| CBMM |

Araxa, Minas Gerais |

~85,000 t (~77%) |

Moreira Salles 70%, China 15%, Japan/Korea 15% |

| CMOC Brasil |

Catalao, Goias |

10,024 t (~9%) |

China Molybdenum (CMOC) |

| Niobec |

Saint-Honore, Quebec |

~6,900 t (~6%) |

Magris (CEF/Temasek) |

Sources: USGS, SFA Oxford, company disclosures.

The USGS weighted average unit value for ferroniobium was $26 per kilogram (gross weight) in 2024. Prices have remained remarkably stable owing to the oligopolistic market structure, with 85 to 90 percent of sales occurring under medium- and long-term contracts. Compounding CBMM’s bullish sentiment for niobium is the fact that its applications in national security insulate it from cyclical risks in other sectors of the economy. Barring an innovation that provides a substitute or the discovery and exploration of new sources to mine from, Brazil and CBMM are well-positioned to control the market, granting Brazil a bargaining chip to use with the United States and other powers.

Figure 3. Ferroniobium price, 2020–2026. Sources: USGS, PricePedia.

Geopolitical Context of the Niobium Trade

Niobium’s geopolitical profile diverges fundamentally from the other critical minerals in this series. China is the world’s largest niobium importer, consuming approximately 36 percent of global ferroniobium supply and importing roughly 95 percent of its niobium needs, predominantly from Brazil. As a comparative benchmark, Brazil’s concentration of niobium even exceeds China’s dominance in rare earth processing, despite receiving far less attention.

President Lula has signaled a more assertive posture on strategic minerals without explicitly targeting niobium. In August 2025, Lula announced plans for a national policy treating strategic minerals as a matter of national sovereignty. The decision feeds into a trend among resource-rich countries seeking more export value by indigenizing the processing and refinery stages of the critical mineral supply chain.

Finance Minister Fernando Haddad stated that critical minerals may be brought into tariff negotiations with the United States. Niobium represents a geostrategic pillar of the 21st century but Brazil has been hesitant to wield export controls of the mineral given the demand among its key allies. The tariff picture underscores niobium’s recognized strategic importance. When the Trump administration imposed a 50 percent tariff on Brazilian imports in July 2025, it explicitly exempted niobium.

The broader Section 232 investigation on processed critical minerals, initiated in April 2025, includes niobium among 50 covered minerals. The January 2026 Presidential Proclamation directed 180-day trade negotiations rather than immediate tariffs, with a reporting deadline of approximately July 2026.

Washington’s Response and the Domestic Supply Chain Buildup

NioCorp Developments’ Elk Creek project in Johnson County, Nebraska represents the only pathway to domestic niobium production. The feasibility study projects 7,450 tonnes per year of ferroniobium over a 38-year mine life. Total project capital cost is approximately $1.1 billion.

As part of America’s return and embrace of industrial policy, federal support has accelerated. In August 2025, the Department of Defense awarded NioCorp subsidiary Elk Creek Resources $10 million under Defense Production Act Title III. Pentagon-funded exploratory drilling totaling 7,336 meters was completed through August 2025.

In October 2025, NioCorp announced a collaboration with Lockheed Martin Skunk Works on aluminum-scandium alloy prototypes for fighter aircraft. The company is pursuing an EXIM Bank loan of up to $800 million and held $307 million in cash as of December 2025. Full production remains unlikely before 2029.

Separately, the DoD awarded $26.4 million in September 2024 to Pennsylvania-based Global Advanced Metals to re-establish domestic niobium oxide production. The DLA awarded GAM a $50 million sole-source contract for niobium ingots over five years.

The USGS records potential government stockpile acquisitions of 136 tonnes of ferroniobium in FY2025.

Looking Ahead

Niobium occupies a paradoxical position in the critical minerals space. Until recently, the Brazilian monopoly and private control of CBMM had allayed concerns of supply disruptions for niobium. However, three developments could disrupt this delicate equilibrium.

First, battery applications could fundamentally reshape demand: if CBMM achieves its 2030 target of 20,000 tonnes of battery-grade niobium oxide, that volume equals roughly 14,000 tonnes of niobium content, or about 12 percent of current global production.

Second, the US Section 232 investigation could introduce tariffs or minimum import prices that restructure trade flows and further instigate trade spats between Washington and Brasilia.

Third, NioCorp’s Elk Creek project, if financed and constructed on schedule, would establish the first US domestic niobium supply since 1959, producing approximately 7,450 tonnes per year and reducing import reliance from 100 percent to roughly 50 percent. Such prospects are what enabled the deluge of federal funding and support to private sector entities in the niobium industry.

Washington has responded with the first funded path to domestic production since 1959, supplemented by stockpile acquisitions and processing contracts that lower near-term exposure. However, none of these measures will produce meaningful resilience before the end of the decade, and until they do, the United States will continue to source a material with no cost-effective substitute in steelmaking from one company in one country.