Global geopolitical trends we’re tracking this week:

Key Dates

December 13 – Japan industrial production for October.

December 14 – India WPI inflation for November.

December 14 – Virtual summit between NATO leaders and Russia.

December 14 – UK employment for October.

December 14 – EU industrial production for October.

December 14 – US Core Producer Price Index (PPI) for November.

December 14 – China industrial production for November.

December 15 – UK Consumer Price Index (CPI) for November.

December 15 – France, Spain, and Italy CPI for November.

December 15 – US core retail sales for November.

December 15 – Canada housing starts for November.

December 15 – Canada core CPI for November.

December 15 – US central bank interest rate decision, dot plot, and policy statement.

December 15 – New Zealand Q3 GDP.

December 15 – Australia employment data for November.

December 16 – Germany manufacturing PMI for December.

December 16 – Trade balance for October.

December 16 – ECB interest rate decision.

December 16 – US building permits for November.

December 16 – Industrial production for November.

December 17 – Germany PPI for November.

December 17 – EU construction output for October.

December 17 – EU CPI for November.

World

COVID-19 fast facts

- The latest WHO situation report notes a plateauing of new COVID-19 cases worldwide along with a 10% increase in deaths over the past week. However, regionally, Africa the Americas saw significant case jumps of 79% and 21% in their respective caseloads.

- Equity markets were buoyed last week on news of preliminary studies from Pfizer suggesting a three-dose vaccine regiment could neutralize the omicron variant.

- Anecdotal and early clinical data continues to suggest that omicron may be milder than previous iterations of COVID-19. The variant continues to spread around the world and has now been identified in 25 US states. Tendencies in this (extremely limited) sample size of 43 US cases include mild symptoms (only one patient was hospitalized), a different symptom set than conventional COVID, and a propensity to infect younger and vaccinated patients (34 of the 43 omicron patients were fully vaccinated, with 14 having received a booster shot).

Americas

Federal Reserve meets after another estimate-beating inflation report

Gone are the predictable Fed meetings of the pandemic era, where terms like ‘transitory inflation’ and ‘for the foreseeable future’ were the order of the day. We already know that change is likely coming to the pace of tapering, as chair Jerome Powell indicated an openness last week to speeding the process up. The decision is reflective of a broad shift in market expectations amid roaring inflation and a recovering job market, with the majority of respondents now of the belief that quantitative easing will wrap up completely by March 2022, with interest hikes to follow soon after. Through its revised dot plot, this week’s meeting will provide further information as to when the first interest rate hike might occur.

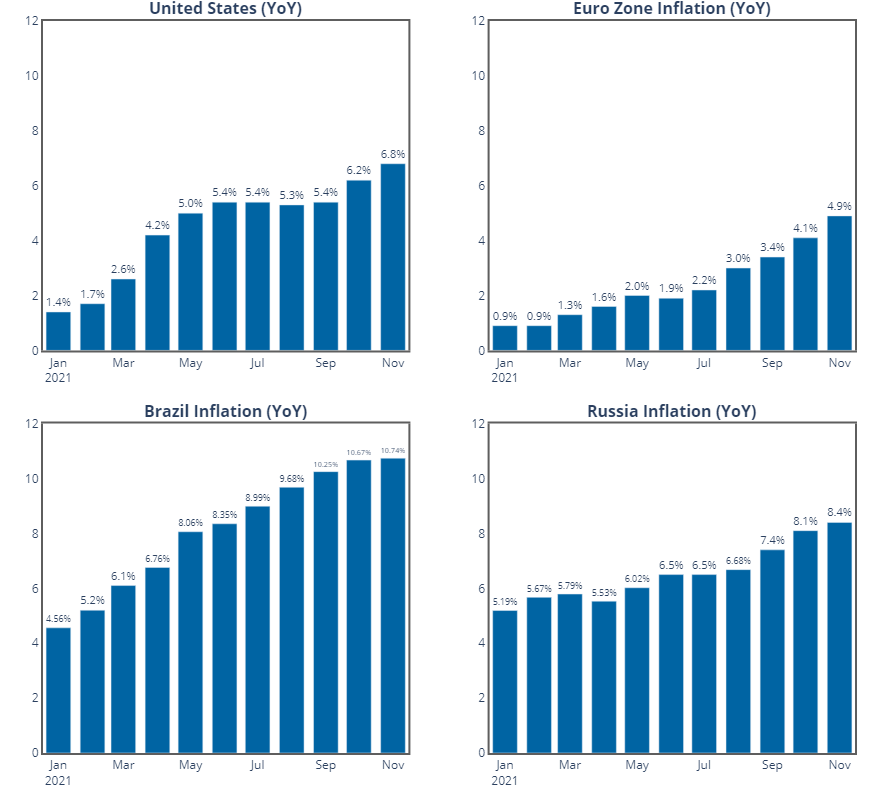

This week’s Fed meeting comes after another expectation-beating inflation report. US consumer prices increased 6.8% year-on-year in November, their quickest pace since 1982, led by gasoline, housing, food, and vehicle costs.

Europe

NATO and Russia to hold talks over Ukraine tensions

NATO and Russian leaders will meet virtually on Tuesday in an attempt to de-escalate tensions along Ukraine’s eastern border, site of an ongoing Russian military build-up. The latest crisis appears to be a diplomatic gambit on the part of Moscow to force NATO to abandon any future plan to admit Ukraine or Georgia into the alliance; the Kremlin indicated as much with the publication of its ‘red lines’ last week. For his part, President Biden has been sending mixed signals, on one hand pushing back against the idea that Russia can dictate NATO expansion policy, and on the other holding out the prospect of next week’s talks.

There will be a geopolitical incentive for the Biden administration to de-escalate tensions in eastern Europe in order to focus squarely on the Indo-Pacific – and this is precisely what is likely underscoring the Kremlin’s present calculations. Standing in the way will be the governments of NATO’s eastern flank, which will collectively be pushing to ensure that Europe remains central in NATO’s strategic planning. Furthermore, the question of just how far Russia is willing to go – whether the current build-up is a bit of military theatre or a legitimate prelude to invasion – remains to be seen.

Africa

Drones turning the tide in Ethiopia’s civil war

The towns of Dessie and Kombolcha have been re-taken by the Ethiopia armed forces, eliminating the immediate threat posed to the capital by the advance of Tigray rebel forces and their allies – at least for now. The operation marks a reversal in fortunes for the government, which had only months ago been reeling ahead of a seemingly unstoppable offensive by the Tigrayans.

Armed drones seem to have been decisive in dislodging Tigrayan forces from the two towns. (The utility of such weapons was discussed in a previous situation report from October). There are only 22 drones currently available to Addas Ababa, primarily of Chinese and Iranian make according to previous investigations by Bellingcat. However, they have proven game-changers on the battlefield, and add to the body of evidence suggesting that the offensive capacity represented by armed drones can ‘unfreeze’ frozen conflicts, particularly when the defending side lacks a modern capacity to contend the air space.

Data Snapshot

Inflation continues to surge throughout the developing world, eliciting policy responses of varying urgency from central bankers.

[/RegUserOnly]