Globalization is commonly measured through aggregate indicators of openness: trade as a share of GDP, capital mobility, export intensity, or participation in international production networks. Such measures are useful for estimating the extent to which national economies are integrated into global markets, but they are less effective at identifying the structural positions countries occupy within globalization itself. Economies may exhibit similar levels of openness while deriving radically different benefits, facing different forms of dependence, or possessing sharply unequal capacities to absorb external shocks and geopolitical pressure.

This study proposes a three-dimensional framework designed to distinguish these structural positions. Rather than asking whether countries participate in globalization, the model asks how they participate, how much value they extract from participation, and how resilient their position remains under conditions of disruption.

The first axis measures structural dependence on globalization. It estimates the degree to which a country’s economic model relies on external markets, imported strategic goods, and foreign financing. The objective is not merely to identify open economies, but to distinguish economies whose internal reproduction depends heavily on continued international integration from those capable of sustaining a larger share of production and consumption domestically. Dependence, in this sense, refers to structural reliance rather than exposure alone.

The second axis measures integration gains from globalization. Participation in globalization does not distribute gains evenly across states. Some countries occupy positions associated with technological sophistication, financial centrality, control over high-value segments of global production chains, and positive international income balances, while others remain integrated primarily through low-value-added production or chronic external indebtedness. This axis does not attempt to isolate globalization from broader developmental capacity. Rather, it measures the extent to which countries convert participation in globalization into productive rents, technological upgrading, financial gains, and logistical centrality.

The third axis measures vulnerability within globalization. Vulnerability is treated as replaceability and positional fragility within global networks, conceptually distinct from dependence. A highly globalized economy may nonetheless possess substantial resilience, bargaining power, strategic centrality, or financial buffers. Conversely, economies with lower levels of integration may remain highly vulnerable because of external leverage, liquidity fragility, or weak substitutability within global production and financial systems. The vulnerability axis therefore estimates the fragility of a country’s position under conditions of sanctions, financial stress, supply-chain disruption, or geopolitical fragmentation.

This distinction has become increasingly important in the context of intensifying geopolitical competition, supply-chain securitization, industrial policy revival, and the growing politicization of economic interdependence. Under such conditions, globalization can no longer be adequately described as a uniform process of integration. Participation in globalization increasingly reflects differentiated positions within a hierarchical and asymmetric international economic system.

The model does not attempt to evaluate globalization normatively, nor does it assume that deeper integration is inherently beneficial. High scores on particular dimensions do not necessarily imply higher levels of development, but rather different structural positions within global economic networks. The objective is analytical: to classify the structural location of states within the contemporary global economy through a multidimensional framework combining dependence, integration gains, and vulnerability.

Where possible, the model avoids normalization procedures based on relative sample distributions, such as min-max scaling or z-scores. Variables are instead constructed through directly interpretable ratios and logarithmic transformations in order to preserve longitudinal comparability and reduce dependence on arbitrary benchmarks. See the methodological note for details.

Globalization Patterns

Globalization does not produce a homogeneous international economy. Instead, it generates a differentiated hierarchy of structurally distinct positions characterized by varying combinations of dependence, integration gains, and vulnerability. Several clear patterns emerge from the data. The three axes identify recognizable geopolitical-economic positions within globalization rather than merely reproducing GDP or development rankings.

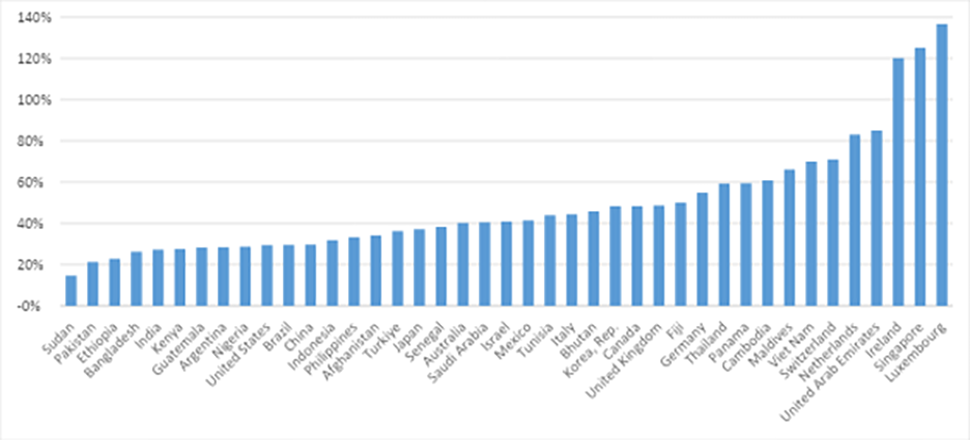

Axis A — Reliance on Globalization

Axis A does not measure a single homogeneous form of openness, but three partially independent forms of structural dependence: external demand dependence, strategic import dependence, and financial dependence. Similar aggregate scores may emerge from distinct structural configurations. The framework therefore identifies comparable levels of structural reliance without implying identical economic forms.

Three broad clusters emerge:

Figure 1 — Reliance on Globalization

The lowest dependence scores are concentrated between two very different groups: isolated domestic-market economies such as Sudan and Ethiopia, and continental-scale economies such as China, India, and the United States. This demonstrates that highly integrated economies are not necessarily structurally dependent on globalization for basic economic reproduction.

Resource exporters form a distinct intermediate category. Countries such as Saudi Arabia display only moderate dependence despite strong export intensity. Conventional globalization indices often classify commodity exporters as highly open economies, yet this model highlights their relative strategic autonomy, stemming from limited dependence on external financing and lower vulnerability to manufactured import disruptions relative to export capacity.

A clearly identifiable “European dependence belt” also emerges, composed primarily of export-oriented manufacturing economies with high structural dependence despite advanced industrial sophistication and high productivity. The model illustrates how successful integration into global markets can simultaneously generate structural exposure.

The highest dependence scores are overwhelmingly concentrated among hyper-globalized microstates, offshore financial centers, and logistical hubs. Due to the insufficiency of their domestic markets, these economies remain viable only through deep and continuous external integration.

More broadly, Axis A suggests that globalization dependence is shaped less by openness alone than by the relationship between domestic scale and external necessity. Large economies can sustain substantial autonomy despite deep integration, while smaller economies often face structural pressure toward external specialization.

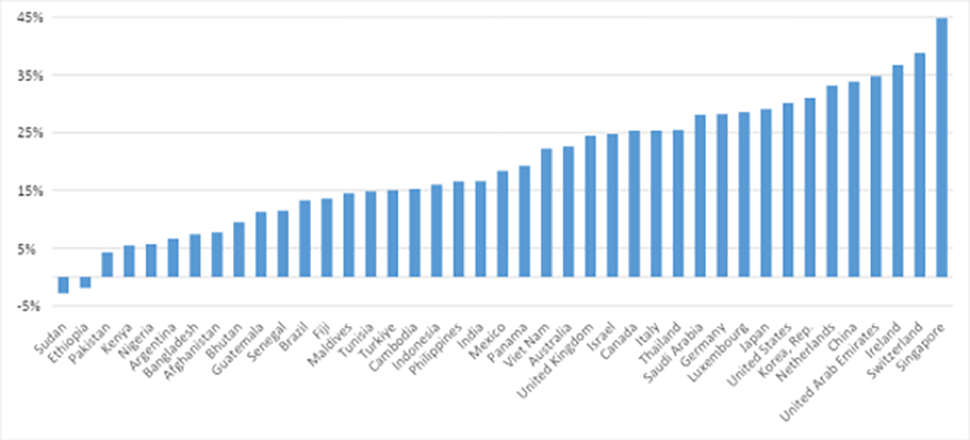

Axis B — Integration Gains

Axis B produces one of the clearest hierarchies in the model: the geography of globalization’s principal winners.

Figure 2 — Integration Gains

The highest scores cluster around three distinct structural models: financial hubs, technological-industrial powers, and resource-financial rent states. This demonstrates that globalization permits multiple successful pathways to surplus capture rather than privileging industrialization alone.

East Asian manufacturing powers, particularly South Korea, Japan, and China, dominate structurally by combining productive sophistication, manufacturing capability, and supply-chain centrality. The model strongly identifies East Asia as the contemporary productive core of globalization, consistent with much of the current political economy literature.

Europe divides into two partially distinct models: a productive-industrial Europe, represented by Germany and Italy, and a financial-platform Europe centered on Luxembourg, Switzerland, and Ireland. This distinction highlights the coexistence of multiple modes of surplus capture within the same integrated regional bloc.

Not all resource exporters capture globalization equally. Gulf monarchies and many African commodity exporters occupy sharply different structural positions. Gulf States convert resource rents into financial depth, sovereign investment capacity, and strategic positioning, while many peripheral exporters, like Nigeria, remain externally dependent suppliers of raw materials with limited upgrading capacity.

The model also reveals a clear peripheral integration trap: supply-chain centrality matters more than manufacturing share alone. China’s advantage is not merely manufacturing scale, but positional embeddedness within global production systems. Countries can survive with relatively low integration if value capture exists, but they struggle to sustain strategic autonomy under conditions of persistently weak surplus capture.

Axis B therefore functions not simply as a measure of economic performance, but as a broader sovereignty-production axis: a hidden hierarchy of extraction, retention, and coordination capacity within the world economy.

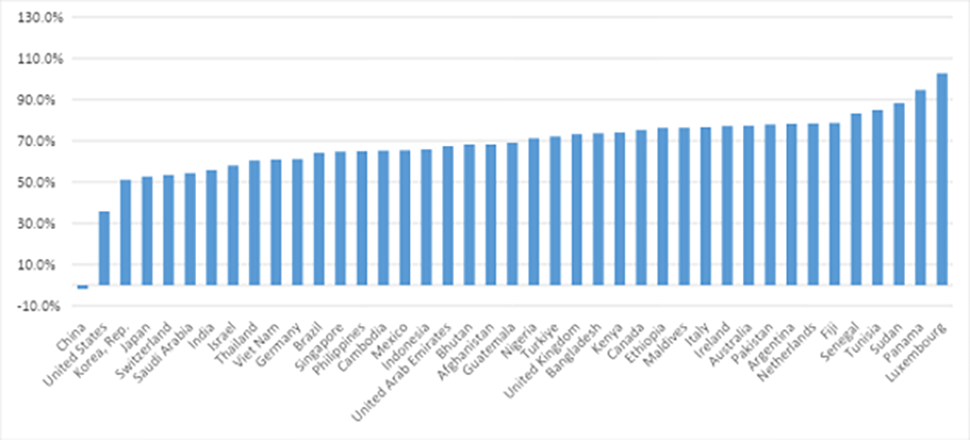

Axis C — Vulnerability

Dependence and vulnerability emerge as distinct dimensions. Germany, for example, is highly integrated but only moderately vulnerable, whereas Netherlands combines high integration with substantially higher fragility.

Figure 3 — Vulnerability

Large continental powers such as China, India, and the United States display the highest levels of resilience due to strategic depth, domestic scale, reserve capacity, and low replaceability within global networks.

Logistical hubs are not structurally uniform. Singapore represents a high-value platform model that combines logistics, finance, and corporate coordination functions, while Panama more closely resembles a transit model centered on geographic intermediation. Both derive advantages from network centrality, but differ substantially in their capacity to capture value and convert strategic position into resilience. Financial hubs exhibit high vulnerability due to the highly mobile and deterritorialized nature of financial transactions.

Peripheral debt-dependent economies cluster among the most vulnerable states, particularly aid-dependent countries characterized by narrow export structures, weak reserves, and chronic external financing constraints.

Microstates also emerge as structurally fragile. Despite occasionally moderate income levels, many exhibit narrow specialization, extreme external dependence, weak bargaining power, and very low strategic redundancy within global networks.

Conventional narratives often assume that countries benefiting most from globalization become more secure, or conversely that deeper exposure automatically produces greater fragility. The model suggests instead that gains and risks are only partially correlated. Economic success within globalization does not eliminate structural exposure; in many cases, it reorganizes it.

Globalization increases not only interdependence, but also specialization. The same mechanisms that generate efficiency, scale advantages, and surplus capture can simultaneously reduce redundancy and increase sensitivity to external disruption. Economies occupying highly optimized positions within global production or financial systems may therefore become structurally exposed precisely because of their success.

This finding aligns closely with supply chain theory, network theory, and complex systems literature. Vulnerability appears positional as much as material: it reflects a country’s replaceability, concentration of functions, and systemic role within international networks rather than wealth or openness alone.

The findings therefore challenge simplistic binaries opposing globalization and resilience. In practice, resilience appears to depend less on the degree of integration itself than on the nature of the position occupied within global systems. Some states derive resilience from centrality, indispensability, and domestic scale, while others remain exposed despite lower levels of integration.

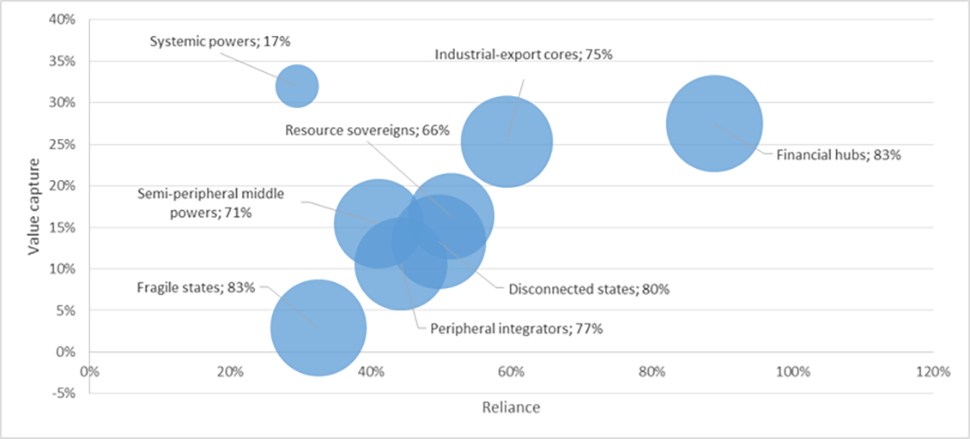

Cross-Axis Structure

When the three dimensions are examined simultaneously, several recurring geopolitical-economic archetypes emerge. These clusters illustrate that globalization does not produce a single hierarchy of “more” or “less” integrated states, but rather a differentiated landscape of structurally distinct positions combining different forms of dependence, surplus capture, and vulnerability.

The first cluster consists of systemic globalization powers, represented most clearly by China and the United States. These are not merely larger states; their economies instead combine high integration gains with comparatively low vulnerability and only moderate structural dependence. Their position reflects systemic embeddedness: they possess diversified production structures, large domestic markets, financial depth, technological ecosystems, and strategic leverage across multiple layers of globalization. They benefit enormously from globalization, while remaining comparatively capable of absorbing fragmentation within it. Their position approximates a form of structural sovereignty within the international economy. India occupies a transitional position between semi-peripheral middle powers and systemic globalization powers. Its continental scale provides strategic depth comparable to the latter, but uneven development and incomplete integration into high-value segments of the global economy continue to anchor many of its characteristics closer to the former.

A second group can be described as industrial exporters, dependent winners such as Germany and South Korea. These states achieve very high levels of surplus capture through advanced manufacturing, technological specialization, and export competitiveness, yet remain deeply reliant on continued international integration. Their economic success is inseparable from stable trade flows, external demand, imported inputs, and open logistical systems. Their position illustrates one of globalization’s central tensions: integration increases efficiency and prosperity, without necessarily maximizing resilience.

When considered in its entirety, however, the European single market occupies a position closer to systemic powers. Many of its member states appear highly dependent when assessed individually, yet the integrated European market internalizes much of this dependence, converting external dependence at the national level into internal interdependence at the continental level.

A third cluster consists of semi-peripheral middle powers such as Turkey, Indonesia, Mexico, or Vietnam. These economies occupy intermediate positions within globalization: partially industrialized, increasingly integrated into production networks, yet still limited in their ability to capture high-value segments of global supply chains. Their integration remains strategically incomplete. In many cases, they possess growing manufacturing capacity without equivalent technological centrality, financial depth, or geopolitical leverage. This hidden “middle trap” separates them from advanced export powers and appears less quantitative than positional: participation without systemic coordination capacity.

Another group can be labelled peripheral integrators. These states rely heavily on globalization while capturing relatively limited surplus and remaining highly exposed to external shocks, liquidity pressures, or geopolitical coercion. Their participation is often concentrated in low-value manufacturing, commodity extraction, or externally financed consumption structures. In many respects, this resembles the classical periphery described in dependency theory: economies integrated into global markets from structurally subordinate positions.

Resource-sovereign economies form another distinct category. These countries often display relatively low structural dependence because of domestic resource abundance or export rents that reduce reliance on external production systems. Yet lower dependence does not necessarily translate into gains that are proportionally comparable with those of technologically and industrially sophisticated countries. Some resource exporters successfully convert rents into financial depth, sovereign investment capacity, and geopolitical leverage, while others remain weakly diversified and technologically peripheral. Resource autonomy therefore appears capable of generating strategic flexibility without necessarily producing productive upgrading.

Disconnected states, concentrated particularly among small island and archipelagic states, occupy another recurring structural position. Limited domestic scale makes them heavily dependent on trade, imports, imports, tourism, remittances, or external financing despite relatively weakly integrated into higher-value segments of globalization. Their position combines high dependence and elevated vulnerability with limited capacity for surplus capture, distinguishing them both from industrial export economies and from globally central financial or logistical hubs.

Finally, the model identifies two distinct groups of hyper-globalized hubs: offshore financial centers and major logistical hubs such as Singapore or Luxembourg. These economies act as deterritorialized platform intermediaries, deriving extraordinary gains from globalization through intermediation, coordination, logistics, finance, or regulatory specialization. Their wealth depends less on domestic productive scale than on occupying indispensable positions within international flows. Yet this same dependence also generates structural exposure. Their prosperity remains inseparable from the continued functioning of highly integrated global systems.

A small subset of Caribbean offshore jurisdictions, notably Bermuda, Barbados, and Turks and Caicos, diverge from the broader financial-hub profile by combining moderate value capture with substantially lower structural dependence. Unlike major platform economies such as Singapore or Luxembourg, these jurisdictions derive a larger share of their income from specialized financial, legal, insurance, and tourism services rather than from intensive participation in global trade and logistics networks.

The central finding is that the three axes do not collapse into a single continuum. High integration does not automatically imply either high vulnerability or high surplus capture, and low dependence does not necessarily imply autonomy or resilience. Instead, globalization generates recurring structural forms that reappear across different regions, political systems, and developmental trajectories.

Countries as geographically and culturally distinct as Norway and Saudi Arabia, Germany and South Korea, or Argentina and Turkey nonetheless occupy comparable structural positions within the global economy. This suggests that globalization operates less as a culturally specific process than as a system generating recurrent geopolitical-economic archetypes shaped by scale, specialization, network position, and strategic function.

Globalization therefore appears not simply as a process of market integration, but as a hierarchical architecture of asymmetrical interdependence structured around unequal capacities for coordination, value capture, and systemic resilience.

Figure 4 — Different Modes of Globalization

Conclusions

Contrary to many dependency theory-based interpretations, which often frame globalization primarily as a mechanism of extraction and peripheralization, this model suggests that participation in globalization is generally associated with at least some capacity for surplus extraction, productivity, logistical, or financial gains. However, the distribution of these gains remains highly unequal. Only a limited number of states function as true globalization “super-capturers,” concentrating the ability to capture high-value rents, technological upgrading, financial influence, or strategic leverage while others remain trapped in low-value forms of integration.

The framework also supports an emerging “network sovereignty” interpretation of geopolitical power. Under conditions of deep interdependence, strategic influence appears to derive less from autarky or simple industrial scale than from occupying indispensable positions within global systems. The most structurally advantaged states are not necessarily the least globalized, but those capable of combining selective openness, domestic scale, technological depth, logistical centrality, and asymmetric leverage over external actors.

This helps explain why countries as structurally different as the United States, China, Singapore, the Netherlands, South Korea, or the United Arab Emirates can all emerge as major beneficiaries of globalization despite relying on very different economic models. Their common characteristic is not ideological similarity or sectoral specialization alone, but the ability to occupy positions within global networks that are difficult to bypass, substitute, or replicate.

At the same time, the findings suggest that globalization remains unevenly distributed across the international system. Much of the world economy appears substantially less structurally integrated than is often assumed in public discourse. Two broader interpretations follow from this observation.

First, significant integration potential still exists. Many economies, particularly across South Asia, parts of Africa, and segments of Latin America, remain only partially embedded within global production systems. This suggests continued scope for industrial upgrading, trade expansion, logistical integration, and technological incorporation.

Second, limited integration should not always be interpreted as developmental failure or incomplete modernization. In some cases, lower integration reflects structural characteristics such as domestic market scale, geographic insulation, resource autonomy, or deliberate political strategy. Not all economies face identical incentives to maximize external integration, and not all forms of integration generate equivalent strategic outcomes.

The broader implication is that globalization should not be conceptualized as a single continuum ranging from “more globalized” to “less globalized.” Instead, it is better understood as a differentiated geopolitical landscape composed of asymmetrical forms of dependence, unequal capacities for value capture, and uneven exposure to systemic risk.

The international economy therefore resembles less a uniform global market than a layered network structure in which states occupy distinct positional roles. Power within globalization depends not simply on participation itself, but on the specific structural position from which participation occurs.

For more details on the data used in this research, please refer to the Methodological Note & Data Matrix.