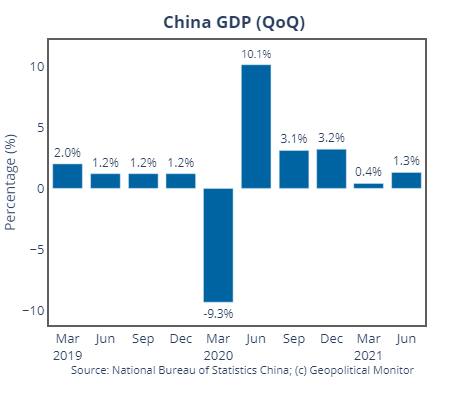

China’s gross domestic product grew by 7.9% year-on-year in the second quarter. However, given the economic climate of this time last year, when the country had just begun to cobble together its recovery from COVID-19, the much more telling indicator remains quarter-on-quarter growth. That figure came in at 1.3%, up from 0.4% the previous quarter.

The numbers are more-or-less what economists had expected, though the usual disclaimer that China state economic data should be taken with a grain of salt applies here as always.

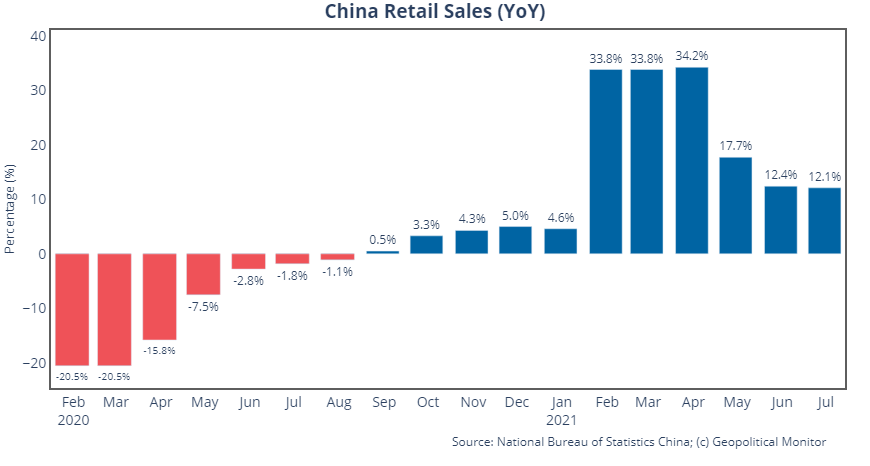

But where the extent of the growth didn’t disappoint, its nature raises questions on whether China’s economic recovery is peaking early. Retail sales saw a monthly expansion of 12.1%, down from 12.4% the month before, though the result beat out Bloomberg’s median forecast of 10.8%.

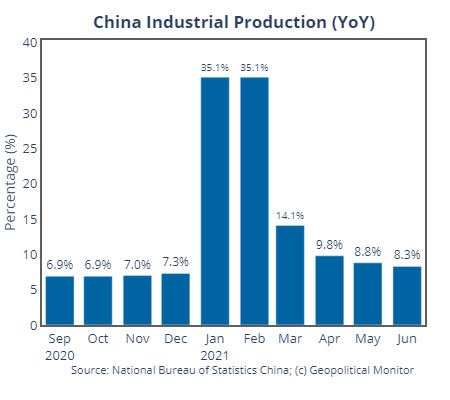

Industrial production, which is strongly correlated to export growth, rose 8.3% year-on-year in June, down slightly from the 8.8% recorded the previous month. Month-on-month production of both steel and cement declined over the same period.

Taken together, the latest data disclosures from the National Bureau of Statistics represent stable growth over the second quarter of 2021. However, where the Chinese economy goes from here has become a point of intense debate, facilitated in no small part by a surprise decision by the People’s Bank of China (PBOC) to cut its reserve requirement ratio (RRR) by 50 basis points, which suggests that the government and monetary authorities are now more inclined to intervene in support of the economy going forward.

This begs the question: Is there anything in the data that has them worried?

One area concern could be a dampening of global demand for Chinese exports. Buoyed savings and deferred purchases across the developed world are producing a bumper crop for China’s export industries, despite ongoing headwinds like increased input and freight costs. The export bonanza has lasted all the way into June, and helped produced the aforementioned favorable Q2 GDP numbers. Chinese exports will inevitably come down to earth as this pent-up demand is exhausted – a process that could be expedited by the resurgence of COVID-19 variants in key export markets from South Asia to the United States.

Another area of concern is the status of COVID-19 in China through the rest of the year. There is a growing body of evidence to suggest that China-produced vaccines are struggling to provide adequate protection against the Delta strain, most recently attested to by Thailand’s decision to provide a booster shot of a Western-developed vaccine to healthcare workers who had already received two shots of the Sinovac vaccine. In Indonesia, 10 of 48 doctors who died from COVID-19 last month had received two Sinovac doses, according to the Indonesian Medical Association.

Insufficient protection against the Delta strain could become an issue for China’s post-COVID economic recovery, as these vaccines form the basis of the Chinese population’s immunity. Though Sinovac and Sinopharm have been shown to significantly reduce the instance of severe illness, they were less effective at eliminating symptomatic cases of the Alpha strain, and their protection is believed to have been further eroded on all fronts by the advent of the Delta strain. The true extent of this erosion remains unknown as, much like with the original rollout of China’s vaccines, there is a dearth of verifiable data with regard to how these vaccines interact with the Delta strain.

What this means in economic terms is a higher likelihood that China will be forced to keep pandemic restrictions in-place through 2021, such as closed national borders and lockdowns of outbreak zones. Such policies stand in stark contrast to other countries pursuing a herd immunity strategy, or ‘learning to live with the virus.’ On the demand side, there’s the risk that Chinese consumers will adopt a wait-and-see approach and defer future purchases, threatening that ever-elusive demand-side growth that China’s economic planners seek.

Mongolia and Chile – two countries that relied on Chinese vaccines and were hit hard by the Delta variant – provide cautionary examples; however, neither has implemented the kind of pandemic-related restriction/monitoring regime that China has rolled out since last year. Therefore, though it remains to be seen how China’s ‘closed borders’ approach to the Delta strain performs, the ongoing presence of COVID will be a net negative for economic growth over the short-term, particularly on the demand side.

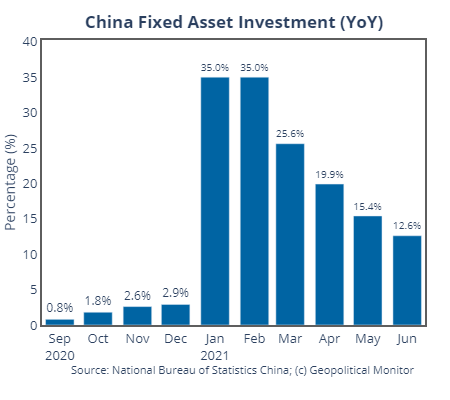

It is better focus on what the Chinese government does, rather than what it says (even in terms of official data releases). Over the short-term, new monetary and fiscal stimulus measures will tell the story of how Beijing views the economic recovery, especially since the authorities have been showing a strong aversion to such measures for fear of unstable debt accumulation in the financial system. To this end, fixed asset investment is worth monitoring as there will be an incentive to enact the same kind of supply-side stimulus that has helped Beijing navigate choppy economic waters in the past.

.jpg")