In March 2022, the decision by Visa and Mastercard to suspend operations in Russia turned international card networks into a visible chokepoint in global geoeconomic infrastructure. Visa announced that cards issued in Russia would stop working abroad and that foreign-issued Visa cards would stop functioning inside Russia. Mastercard delivered a similar message: cards issued by Russian banks would no longer be supported on its network, while cards issued outside Russia would not work at Russian merchants or ATMs. The effect was immediate. Cross-border card functionality, usually treated as invisible financial plumbing, was revealed to be contingent on geopolitical alignment and corporate risk decisions.

That episode did not suddenly make payment cards strategically important; it made their importance impossible to ignore. Cards are critical infrastructure for retail commerce, travel, e-commerce, and the day-to-day liquidity of households and firms. The vulnerability lies not in dependence on the United States as such, although Washington’s more assertive and less predictable use of economic power has sharpened the issue. It lies in the combination of market concentration and extraterritorial exposure: when essential payment rails, rule-setting, and operating decisions sit outside local jurisdiction, political shocks can quickly become economic disruptions, while market power becomes a durable source of pricing and governance leverage.

Those events underpin the ongoing policy debate on card-payment systems in the European Union. Europe’s exposure to US payment companies is not directly comparable to Russia’s position in 2022, but it is serious enough to raise clear questions about strategic vulnerability in a critical layer of retail payments. In the euro area, 13 countries rely entirely on international card schemes for card transactions, and international schemes account for roughly 61% of euro-area card payments. Piero Cipollone, a member of the European Central Bank’s (ECB) Executive Board, summarized the EU’s concern bluntly in February 2026: non-European companies carry out almost two-thirds of euro-area card-based transactions, weakening Europe’s payments autonomy, which is ‘already under pressure’ as cash use declines.

The question, then, is not whether the EU should do away with US-based payment providers; that remains politically unrealistic and would be economically self-defeating. The real question is whether Europe can reduce single-point dependencies without fragmenting the single market, degrading user experience, or turning payments into a transatlantic grievance. In practice, ‘autonomy’ in card payments means building credible European fallbacks and negotiating leverage to ensure European consumers can pay and European merchants can accept payments under Europe’s rules even when geopolitics turns hostile.

Payment Cards as a Dependency

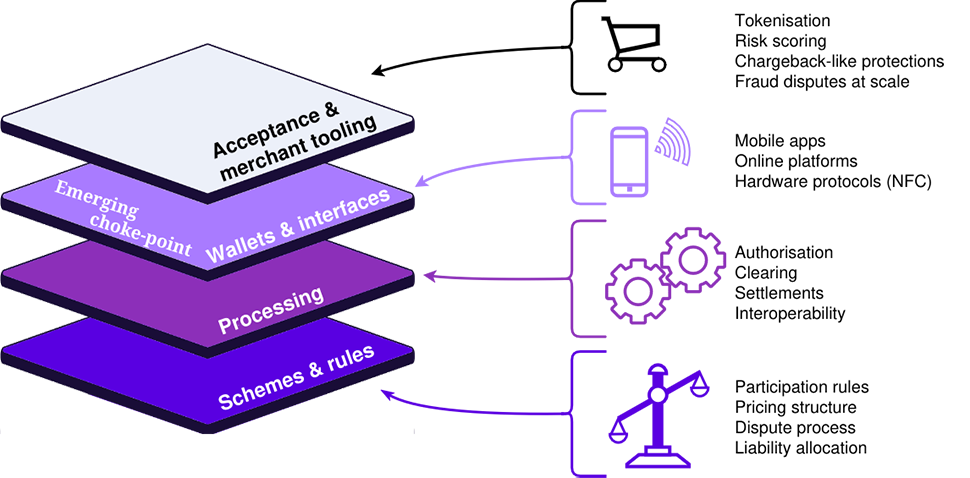

The Visa-Mastercard duopoly in card payments is not a single dependency but a layered stack of them, together shaping whether Europeans can pay and whether European merchants can accept payments seamlessly across borders. The public debate tends to focus on the logo on the card. The more important vulnerability lies in who controls the rules, the processing infrastructure, and the customer interface.

Control in card payments is layered across schemes and rules, processing, wallets and interfaces, and merchant acceptance, with the wallet layer emerging as the key chokepoint.

First, schemes and rules. Card schemes define the commercial and technical rule book: who can participate, how fees are structured, how disputes are handled, how liability is allocated, and which standards allow a card issued in one country to work in another.

Second, processing. Even if Europe had more domestic card brands, authorization and processing services could still run through entities outside European control. The ECB’s mapping of card processors shows that, among the major processors operating across EU borders, none can be identified as fully EU-owned, creating a distinct chokepoint beyond the schemes themselves.

Third, front ends. The contactless payment experience is increasingly mediated by device operating systems and wallets, which can shape user choice through access conditions, default settings, and interface privileges. The Commission’s Apple case made that gate-keeping risk explicit. It required Apple to open iPhone NFC access to third-party wallet developers, allow default-wallet functionality, and address related competition concerns arising from platform control over contactless payments.

Fourth, acceptance and fraud tooling. Acceptance is not just a matter of terminals. It also depends on tokenisation, risk scoring, dispute-management processes, and the operational systems that merchants and payment service providers use to manage fraud and customer complaints at scale. These functions shape user trust and merchant willingness to adopt any alternative payment system.

The strategic implication is straightforward: even if Europe substitutes one layer, such as a new scheme or an instant payment system, another layer may still control access to the customer experience. Europe’s challenge is not simply to build a European equivalent to Visa. It is to achieve pan-European scale where network effects, default behavior, and user dependence emerge fastest.

Why Dependency Matters: Three Tangible Costs for the EU

Until early 2026, Europe’s response to dependence in card payments had focused less on displacing US providers outright than on reducing vulnerability by tightening competition enforcement and developing alternative European capabilities. Since 2020, the EU’s retail payments strategy has combined tighter oversight with efforts to support instant payments, improve access to essential infrastructures, broaden digital acceptance, and encourage European payment solutions with cross-border reach. The objective is not autarky or the construction of protected national champions, but a payments ecosystem in which critical chokepoints are less concentrated and less exposed to decisions taken outside European jurisdiction.

First, at the level of schemes and rules, European authorities are trying to reduce the persistent bargaining asymmetry merchants face. For many firms, especially the small and medium-sized businesses that make up much of Europe’s economy, declining cash use means card acceptance is no longer a genuine choice. In a structurally concentrated market, merchants are often left to accept the dominant networks’ terms on a take-it-or-leave-it basis. Regulators are increasingly treating this not as a tolerable price for convenience, but as a competition problem. The UK’s Payment Systems Regulator offers a useful precedent: it found that Mastercard and Visa had increased core scheme and processing fees to acquirers by at least 25% since 2017, costing businesses at least £170 million more per year, while opaque fee information impeded negotiation. In the EU, that same combination of concentration, weak transparency, and limited merchant leverage is now attracting closer antitrust scrutiny. In 2025, the European Commission widened its antitrust probe into Visa and Mastercard’s fees, seeking evidence on transparency, value for money, mandatory services, and the effects of market power.

Second, at the level of processing and system resilience, concentration can amplify both commercial and geopolitical risk. The suspension of Visa and Mastercard’s Russian operations in March 2022 showed how quickly cross-border card functionality can be segmented when sanctions compliance collides with geopolitical shock. For Europe, the lesson is not that its position is equivalent to Russia’s, but that dependence on a small number of non-European providers can become a continuity risk in a more conflict-prone environment. Cipollone argued that Europe’s payments autonomy is already under pressure in retail payments and called for a more resilient European payments system. The ECB’s retail payments strategy is even more explicit, stating that Russia’s war of aggression against Ukraine has underlined the importance of resilience and strategic autonomy in retail payment systems. Reduced reliance, then, is not an abstract autonomy preference. It is contingency planning for systemic resilience.

Third, at the front-end layer, control over data, standards, and interface design is increasingly where value and power accumulate. The greatest strategic value in modern payment systems often lies not in the basic transfer itself, but in tokenization, risk modelling, dispute management, and the user experience that shapes consumer choice. In practice, whoever controls the hardware protocols, wallet environment, and data flows can capture the higher-margin services built on top of basic transactions. The ECB has argued that overdependence on a small number of non-European payment solutions and technologies is undesirable partly because of the need to protect payments data and preserve traceability in the fight against money laundering, terrorist financing, and tax evasion. It also warns that the interests of global technology firms may not align with those of European stakeholders, and that excessive concentration can reduce competition and enable the abuse of market power.

Europe’s Practical Route: Make Instant Account-to-account Payments Usable at Scale

Historically, regulation has been an essential component of the EU’s response to technologies and markets on which it depends but in which it has only a limited productive footprint. In retail payments, however, the European approach has moved beyond regulation alone. The ECB’s retail payments strategy has long paired oversight with two broader goals: improving instant payments and supporting the emergence of pan-European payment solutions. More recently, ECB speeches on payments autonomy have made clear that regulatory control over the existing stack is not enough on its own. Europe also needs payment rails and acceptance structures it can scale under its own conditions. That does not mean creating an ‘Airbus for cards.’ It means making instant account-to-account payments a credible mass-market alternative in parts of retail payments where the card stack is not indispensable. The Instant Payments Regulation is central to that effort: it mandates payment service providers that offer standard euro credit transfers to also offer instant euro credit transfers, and it bars them from charging more for instant transfers than for corresponding non-instant ones.

The ECB’s description of instant A2A payments highlights three reasons they are strategically attractive. First, they move the transaction logic away from international card schemes and towards account-based infrastructure. If instant A2A becomes ubiquitous, the premium attached to card-based intermediation becomes harder to justify in a range of domestic use cases, especially bill payments, person-to-business transfers, and lower-margin retail transactions. Second, instant payments reduce dependence on some of the chokepoints embedded in the international card stack, even if they do not eliminate all of them. In the EU, instant euro credit transfers are based on the SEPA Instant Credit Transfer scheme and can be settled through infrastructures such as TIPS, which settles in central bank money. Third, the regulatory framework addresses specific frictions that previously limited adoption. The Instant Payments Regulation requires verification of payee before authorization, at no additional charge, and replaces transaction-by-transaction sanctions screening for instant payments with periodic checks of customers against targeted restrictive measures, at least daily.

Still, instant A2A can displace cards only if it evolves from a compliance product into a compelling retail proposition that consumers and merchants trust. That means solving for the practical features users already expect from card payments: low-friction refunds, credible protections in e-commerce, strong but unobtrusive authentication, standardized merchant integration, and fraud controls that scale without generating excessive false positives. It also means avoiding a situation in which the user experience is simply re-routed through the same foreign-owned closed wallet and platform ecosystems that already mediate the front end of digital payments. From the merchant side, instant payments cannot remain just a bank transfer with better timing. They need standardized checkout buttons, plug-ins, reconciliation flows, and support processes that are as easy to implement as established card solutions. This is where Europe still faces a scale problem. As the ECB has noted, most existing European payment solutions suffer from a small footprint in physical shops and limited online coverage, while building a common acceptance network will take time and money.

Europe can nevertheless draw useful lessons from Brazil and India, both of which show that instant payments can achieve mass adoption when they are interoperable, simple, and widely accepted. In Brazil, Pix has become one of the country’s dominant retail payment instruments within a few years, accounting for nearly half of all non-cash payment transactions by the last quarter of 2024. In India, UPI reached roughly 21.7 billion transactions in January 2026 alone. Still, Europe cannot copy either model directly. The EU remains a union of 27 states with fragmented banking and retail landscapes, different legacy systems, and more complex coordination problems than a single domestic jurisdiction. That is precisely why product standardization, common acceptance, and pan-European roll-out matter so much: without them, instant payments may expand as infrastructure without becoming a true consumer-and-merchant standard.

The Market Vehicle: EPI’s Wero as Test Case

The European Payments Initiative (EPI) is a consortium of 16 banks operating across France, the Netherlands, Germany, Belgium, Luxembourg formed to develop payment solutions built in Europe for European users. Its flagship product is Wero, a pan-European digital wallet built on instant A2A transfers. Wero matters because it is one of the clearest market attempts to make instant payments usable across borders at the consumer interface rather than leaving them as a back-end compliance feature. In that sense, it is more than a symbolic sovereignty project, and potentially stands as a practical test of whether A2A payments can become a recognizable payment method for everyday retail use in Europe. EPI’s roll-out has already moved beyond peer-to-peer transfers. In late 2025, the EPI launched Wero for e-commerce in Germany. Then, in March 2026, Wero’s e-commerce deployment expanded to Belgium with a list of early-adopters amongst leading merchants in the country.

The decisive question, however, is adoption. Here, Wero faces a classic two-sided network problem: merchants will not invest in integration or redesign checkout flows without evidence of customer demand, while customers will not switch without broad acceptance and a clear advantage in speed, simplicity, trust, or convenience. EPI’s own sequencing reflects that reality. Wero first built an initial base through person-to-person payments and only then moved into merchant use cases, with e-commerce positioned as the next step and in-store payments still to come. On the merchant side, the phased migration from iDEAL to Wero in the Netherlands gives EPI a way to build scale by leaning on an existing national A2A habit rather than starting from scratch, though that transition will unfold over time rather than in a single step. On the consumer side, the initiative seems also to be gaining traction amongst online-first payment providers, with Revolut, Mollie, and bunq already participating in EPI and N26 joining Wero in December 2025. Yet, the harder test is sustaining momentum across markets so ‘local’ and ‘online-first’ footholds compound into genuinely pan-European scale.

Beyond Visa and Mastercard: Big Tech Wallets and Device Control

Europe may be able to lay the regulatory foundations for an alternative payments stack and even support credible pan-European products such as Wero. Yet, market power will not shift if those options cannot reach consumers at the point of payment. Increasingly, that point is mediated by smartphone operating systems, digital wallets, and platform-controlled interfaces. The ECB has warned that mobile apps and e-payment solutions in Europe are already dominated by foreign providers such as PayPal and Apple Pay, and that when transactions are routed through these channels European banks lose not only fees but also data. In that context, default settings, interface design, and platform access rules can shape which payment method users actually adopt, regardless of whether a European A2A alternative exists underneath.

This is why competition enforcement and platform regulation are a necessary pillar of any serious European payments strategy. The clearest case is Apple’s control over NFC access on the iPhone for in-store mobile wallet payments. In July 2024, the European Commission made Apple’s commitments legally binding under EU antitrust rules. Apple agreed to grant third-party wallet providers free access to NFC on iOS, apply fair and non-discriminatory access criteria, and allow users to set rival apps as their default payment app while using key iPhone functions such as Field Detect, double-click, Face ID, Touch ID, and passcode authentication. The policy logic is straightforward: if a European payment solution cannot access the same hardware features, cannot be set as the default wallet, or faces extra friction at checkout, it is unlikely to reach scale no matter how efficient the underlying payment rail may be.

Recent market behavior underlines the point. In May 2025, PayPal launched contactless mobile wallet payments on iPhone in Germany as NFC access opened up, showing how quickly interface governance can reshape competition for in-store transactions. Apple’s case is a textbook reminder that payment autonomy cannot rest only on enabling regulation and technological innovation, but requires market oversight to guarantee interoperability, especially when it comes to the front end’s default settings, hardware protocols, and other platform-specific constraints.

What Success or Failure Looks Like for the EU

Europe will not ‘break free’ from Visa and Mastercard in any meaningful sense over a two-year horizon. The practical objective is narrower: to ensure that day-to-day commerce can run at scale on a payments stack that operates within Europe’s regulatory and institutional perimeter, so that global card schemes remain valuable options rather than unavoidable toll booths. That is why the policy focus is shifting towards instant A2A payments, while market actors are investing in productization efforts such as Wero. The Instant Payments Regulation is designed to accelerate the roll-out of instant euro credit transfers, and Wero’s e-commerce expansion shows what a market-facing European alternative is supposed to look like.

The EU’s payments-autonomy agenda will succeed or fail on three measures. First, transaction mix: whether a meaningful share of routine retail payments, online and in-store, actually migrates onto a European payments stack through repeated use rather than nominal availability. Second, merchant economics: whether sellers, especially small businesses, find enough value in the new system to adopt it at scale, and whether that adoption materially weakens the market power and pricing leverage of the Visa-Mastercard duopoly. Third, resilience and redundancy: whether Europe can keep payments functioning through disputes, outages, or geopolitical shocks because it has built a credible alternative stack, acceptance channels, and front ends rather than relying on parts of the existing foreign-controlled stack. The ECB has made clear that Europe’s autonomy in retail payments is already under pressure and that resilience now has to be treated as a strategic objective, not merely a technical one.

The plausible upside is one of incremental autonomy: instant A2A payments become a routine option in parts of retail commerce; Wero and similar front ends achieve meaningful penetration in e-commerce and, eventually, in-store payments; cards remain in the system, but lose some of their pricing power because merchants and consumers have credible substitutes. The downside is a failure mode already familiar from other European-sovereignty efforts: fragmentation persists, Big Tech wallets and the incumbent payments stack retain consumer and merchant trust, and Europe ends up investing in alternatives that exist formally but do not reach behavioral scale. In that scenario, the chokepoints remain because the technical means to bypass them exist only on paper.

An MH-60R Sea Hawk helicopter attached to the “Swamp Foxes” of Helicopter Maritime Strike Squadron (HSM) 74 flies by the Arleigh Burke-class guided-missile destroyer USS Thomas Hudner (DDG 116), June 17, 2021 during exercise BALTOPS 50. BALTOPS 50 is an annual international maritime-led joint exercise including 16 NATO allies and 2 partner nations demonstrating the ability of the alliance to contribute to deterring and if required defeating aggression. (U.S. Navy photo by U.S. Thomas Hudner Public Affairs/Released) cc Flickr, modified, https://www.flickr.com/photos/cne-cna-c6f/51257091333/")

_01.jpg")