The latest data release from the UK’s Office for Budget Responsibility (OBR) outlines a precarious path back to economic normalcy for a country that has had to fend off the ill effects of COVID-19 and longstanding uncertainty over Brexit.

Established in 2010, the OBR is a watchdog that provides independent analysis of governmental finances. Its main duty is to hold the government to account on its targets and projections.

Thus, when the OBR talks, people tend to listen. And there’s not much to like in this latest disclosure.

Analysis

GDP data sags on the downside

According to the OBR, the UK economy will contract by 11.3% in 2020. To put it in historical context, this is a sharper contraction than any experienced during the world wars. In fact, you need to go all the way back to the Great Frost of 1709 to find a more severe economic disruption.

The OBR projects that the UK will return to a growth rate of 5.5% in 2021, followed by 6.6% growth in 2022, before normalizing into a range of 1.8-2.3% in the three subsequent years.

If these projections play out, the UK economy won’t return to its pre-COVID size until the final quarter of 2022.

The UK GDP projections are considerably worse than those of its continental peers. According to EU Commission forecasts, the only European country hit harder this year is Spain, which is expected to contract by 12.4% in 2020. Other major economies have weathered the storm considerably better than the UK: Germany (expected contraction of 5.6%), the Netherlands (5.3%), Greece (9%), France (9.4%), and Italy (9.9%).

Borrowing and inflation risks

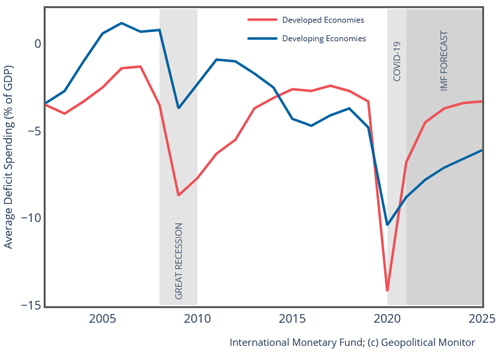

Government borrowing spiked throughout 2020, reaching 19% of GDP ($526 billion) and shattering the previous peacetime record of 10% of GDP. That London leaned on debt to weather the COVID-19 storm is hardly exceptional. Indeed, developing and developed countries alike have piled on debt throughout the COVID-19 pandemic. However, the UK case is exceptional in two ways: 1) the relatively higher levels of borrowing; and 2) the non-COVID related political risks that the country faces (Brexit), which may in turn create future volatility in their own right.

There are countries that have borrowed more than the UK to finance their COVID-19 response. Canada, for example, borrowed nearly 20% of its GDP. The Un ited States isn’t far behind the UK at 18.7%. However, Europe’s borrowing makes London look profligate in comparison: Germany borrowed 8.2% of its GDP, Italy 13%, Spain 14.1%, and the Netherlands 8.8%.

ited States isn’t far behind the UK at 18.7%. However, Europe’s borrowing makes London look profligate in comparison: Germany borrowed 8.2% of its GDP, Italy 13%, Spain 14.1%, and the Netherlands 8.8%.

, modified, https://creativecommons.org/licenses/by/2.0/")