The latest report from the Congressional Budget Office (CBO) is enough to curdle the blood of any fiscal conservative.

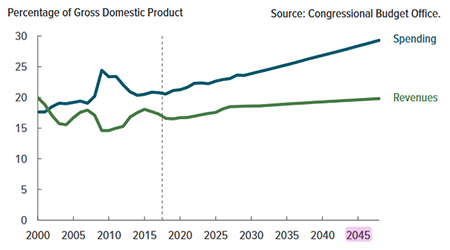

According to the report, US federal debt held by the public relative to GDP currently stands at 78 percent (debt issued in Treasury securities). If current trends hold, that number will reach 100 percent of GDP by the end of the decade, and 152 percent of GDP by 2048. Broadly speaking, the expansion is being fueled by outlays for Social Security and Medicare and increasingly burdensome interest payments on preexisting debt.

The country’s darkening fiscal outlook is sure to resonate in future elections in the United States, but there’s a crucial international dimension here as well.

Background

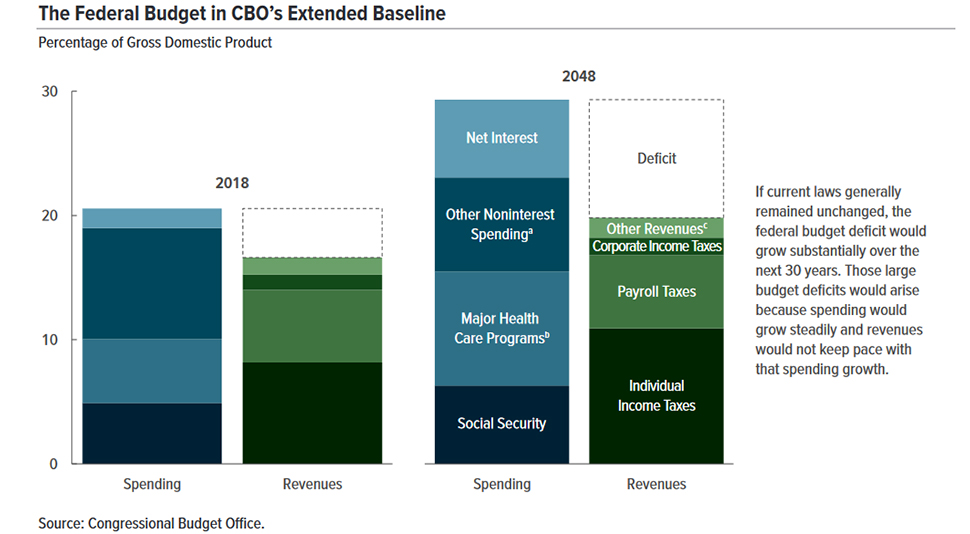

Spending growth will contribute to widening deficits over the next 30 years.

The CBO predicts that Social Security spending will grow from 4.9 percent of GDP in 2018 to 6.3 percent in 2048; health care programs (including Medicare and Medicaid among others) will rise from 5.2 percent to 8.7 percent, mostly on the back of an aging population and high healthcare costs per person; and interest payments will balloon from 1.6 percent to 5.3 percent.

Annual deficits are projected to rise from 3.9 percent in 2018 to 8.4 percent in 2048.

Discretionary spending relative to GDP over the same period is expected to fall, if nothing because the budgetary math increasingly won’t allow for it. Discretionary spending was 6.3 percent of GDP in 2018; the CBO expects that number to fall to 5.5 percent by 2048.

Revenues are expected to remain flat for the next few years and then jump in 2026, when income tax cuts from this year’s tax act are set to expire. Revenues would then grow in-step with the economy, but they would still fail to keep pace with spending growth.

Impact

The CBO projections are grim enough as-is, but the reality could turn out even worse. The CBO makes various assumptions when calculating its estimates – assumptions on growth, interest rates, productivity, and labor participation. And while there is some room on the upside for better-than-expected overall results (for example, if the political will materialized in Washington to address the debt problem sooner rather than later), there’s considerable downside risks as well.

Interest rates

One such risk stems from unforeseen fluctuations in interest rates. The post-2009 era has seen unprecedentedly low rates, which have produced a favorable borrowing environment for the US government. The CBO foresees the yield on 10-year Treasuries rising to 3.7 percent by 2028 and then 4.8 percent in 2048. The average yield from the period of 1990-2007 was 5.8 percent.

Bond yields are a product of supply and demand. There has been ample supply as US governments over the past two decades have sought outside funding to fill their deficit gaps. But what about demand?

The United States government has always benefitted from crisp foreign demand for US Treasuries, which are seen as a safe-haven asset denominated in a global and relatively stable currency (critically, nearly all global oil sales are settled in USD). Countries like Japan and China have amassed huge reserves of US government debt, holding some $1.030 trillion and $1.179 trillion in Treasuries respectively as of early 2018. Their purchases of US debt serve to depress yields, which in turn makes it cheaper for the US government to borrow and finance its agenda at home and abroad.

There’s reason to believe that US Treasuries will be less appealing for foreign governments over the short-to-medium term. One consistent drag will stem from the United States’ growing debt pile; not insofar that it represents a risk of default per se, but rather a risk of currency devaluation in order to make the debt easier to pay off at some point in the future. If the US dollar tanks, it makes foreign Treasury holdings less valuable relative to the local currency in question.

There’s also the fact that, as states move further along the development curve, maintaining large holdings of foreign exchange becomes less crucial to their economic stability. We’re already seeing signs of this as Japanese and Chinese investors start to divest from Treasuries. Such divestment is sure to proceed slowly so as not to cause a panic and impact the value of a country’s remaining holdings. China in particular has been especially circumspect over the past year, presumably because it doesn’t want to give the impression it’s triggering the ‘nuclear option’ in its ongoing trade war with the United States. That nuclear option would be a liquidation of its USD-denominated reserves – a move that would cause US Treasury yields to surge, but severely undercut the value of China’s remaining holdings in the process.

USD-denominated assets have been the global the benchmark for foreign reserves since the gold standard was abandoned in the 20th century. This may not always be the case, but for now USD primacy is definitely bolstered by a lack of credible alternatives. The euro is held in the reserve portfolio of various governments, but the spectre of Greece and perennial risks to the long-term stability of the euro zone continue to relegate the currency to a secondary position behind the USD. The renminbi is another possible alternative, but it remains illiquid as a global currency barring a wave of new reforms in China.

The situation could well change in the 30 years considered by these CBO projections, especially if the expected debt accumulation actually comes to pass. In other words, just like the gold standard that preceded it, the US dollar may not always be viewed as the standard-bearer of global finance. And if a reckoning does eventually occur, it will surely have been expedited by the precarious fiscal outlook of the US government.

Growth shocks

Another realistic contingency that the CBO outlook ignores is a systemic shock like the 2008-2009 Great Recession. Tough to predict, these events can scuttle even the most exacting economic projections.

In 2007, the US debt stood at just 35 percent of GDP, nearly half of its current level. Post-2009 simulative policy responses were spend-heavy, impacting the government’s bottom line in ways that still resonate to this day. One 2012 estimate from the US Treasury put the total exposure for US taxpayers at $24 trillion in response to the Great Recession – and that’s just on the spending side of the equation. In terms of revenues, systemic economic shocks can wipe out trillions of household wealth, hollow out the employment market for several years, and undercut the government’s tax base. (Though in some respects, US taxpayers actually gained when distressed assets and Treasuries were eventually sold off).

The CBO projections use a baseline of 1.9 percent annual growth for the next 30 years. The rate is lower than the historical average of 2.8 percent owing in large part to tepid growth of the US labor pool.

Forecast

We’re still well within the bounds of normalcy here.

Washington is ignoring the long-term track of government finances, and the global financial system is still dominated by Wall Street (notwithstanding a few early signs of dissent, such as calls in the EU for an alternative system for the Continent and the proliferation of bilateral deals to settle trade accounts in local currencies). US debt levels also remain within elevated-but-acceptable limits at 78 percent GDP, with a deficit of just under 4 percent.

But it’s from here on out where the normalcy potentially dissipates, at least if the CBO projections prove correct. The borrowing binge of the past decade was aided by record-low yield rates thanks to QE and the uncertain fate of the euro zone. Now yields are normalizing, and so too is the long-term fiscal impact of the government deficit, which in turn drives upward pressure on borrowing rates as demand for Treasuries dries up.

In other words, US finances are now entering a dangerous cycle of debt begetting more debt.

It will take rare political will to right the country’s fiscal ship, and the sooner it arrives, the less pain there will be over the long run. However, should Washington politicians continue to ignore the problem, we could be looking at a very different global financial system by the time the CBO projections’ end-date of 2048 finally rolls around.

**Originally published on November 14, 2018.