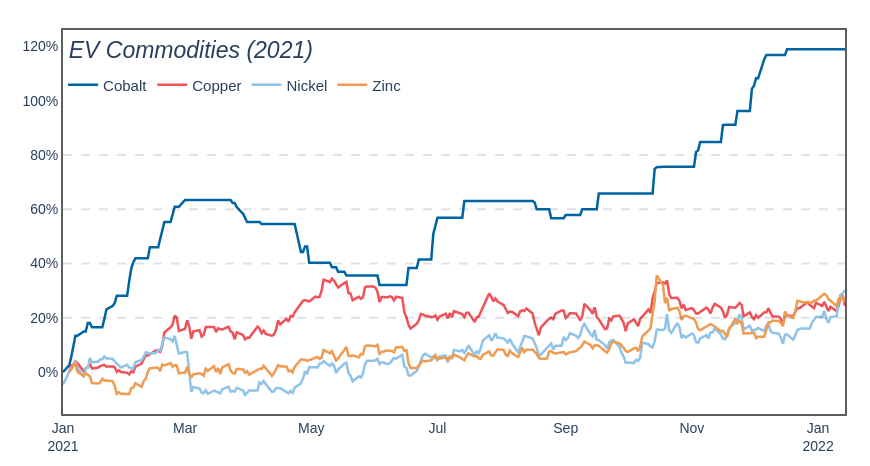

Constrained supply and bubbling demand are combining to drive up prices of key electric vehicle inputs, with many of the factors behind this bullish trend set to endure into 2022.

Lithium, or ‘white gold,’ is leading the pack: lithium carbonate prices spiked more than 400% over the course of 2021, with lithium hydroxide up 250% over the same period (numbers based on average seaborne trade, as the alkali metal does not have a spot market). S&P Global Market Intelligence estimates 2021 lithium chemical supply at 497,000 mt; in 2022, the number is expected to rise to 636,000 mt. However, markets are expected to remain tight as demand is also expected to rise, from 504,000 mt in 2021 to 641,000 mt in 2022. The resulting deficit of approximately 5,000 mt implies sustained price momentum in the year ahead. (Lithium markets were in surplus to the tune of 66,000 mt in 2020, and a deficit of 8,000 mt in 2021).

Broadly, this aligns with longstanding forecasts predicting lithium supply and demand to boom on green transitioning policy initiatives around the world, with a distinct possibility of demand outpacing capital-intensive supply relief. In terms of the latter, one supply story to keep an eye on in 2022 is left-wing president-elect Gabriel Boric’s efforts to regulate the lithium industry in Chile, a country that accounts for nearly one quarter of global supply. Boric has recently mooted the possibility of establishing a state-owned lithium corporation, and the royalty regime for private operators is widely expected to be dramatically altered in the years ahead (either by Boric’s administration or the ongoing constitutional reform process).