., modified. Originally from: https://commons.wikimedia.org/wiki/File:At_Santos,_Brazil_2017_105.jpg")

On April 24, DP World launched the Brazil-Africa Link, an integrated logistics corridor connecting the Port of Santos to its operations in Angola, Mozambique, and South Africa. Unveiled at the Intermodal South America trade fair in São Paulo, the service combines ocean freight with inland transport under a single-operator model, drawing on three port terminals, 52 warehouses, and a fleet of more than 4,250 vehicles.

Mohammed Akoojee, who leads DP World in Africa, called the corridor a “transformative step” for trade between the two continents. The launch drew limited coverage in international media, yet it marks a deliberate move by an Emirati state-controlled operator to consolidate a thin and fragmented trade lane between two of the world’s largest commodity-exporting regions.

The corridor’s significance comes from the control it concentrates over the route rather than the volume it will carry at the outset.

Background and Context

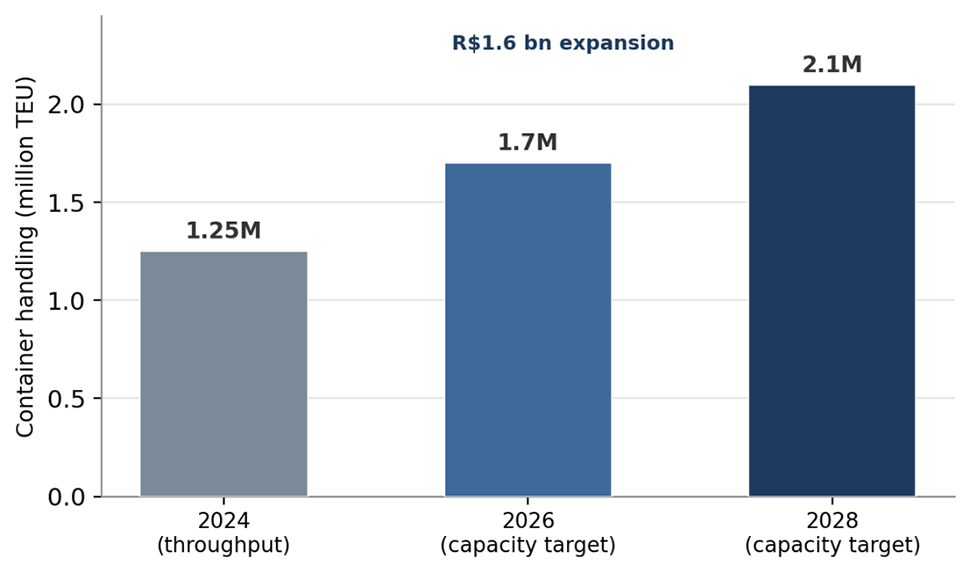

DP World, headquartered in and controlled by the Government of Dubai operates ports and logistics across six continents. Its presence on both sides of the South Atlantic gives the corridor its foundation. In Brazil, the company owns the former Embraport terminal at Santos, the country’s largest port, which handled a record 1.25 million twenty-foot equivalent units in 2024.

An investment announced in December 2025 will raise the terminal’s annual capacity to 1.7 million twenty-foot equivalent units in 2026 and 2.1 million by 2028. Across the Atlantic, DP World holds port concessions in Luanda and Maputo and runs an inland network in South Africa, part of a wider African build-out that includes a $1.2 billion dollar port under construction at Ndayane in Senegal.

Table 1. DP World Assets Underpinning the Brazil-Africa Link

| Location | Asset | Detail |

|---|---|---|

| Santos, Brazil | Container terminal (former Embraport) | Brazil’s largest port; 1.25M TEU handled in 2024; expansion to 2.1M TEU by 2028 |

| Luanda, Angola | Multipurpose terminal | 20-year concession |

| Maputo, Mozambique | Port concession | Long-standing concession with capacity expansion |

| South Africa | Inland logistics network | Warehousing and road transport feeding the corridor |

| Ndayane, Senegal | New deepwater port (under construction) | Roughly US$1.2 billion investment |

Sources: DP World; Seatrade Maritime; AGBI.

Figure 1. Port of Santos container capacity. Source: DP World. 2024 figure is actual throughput; later years are capacity targets.

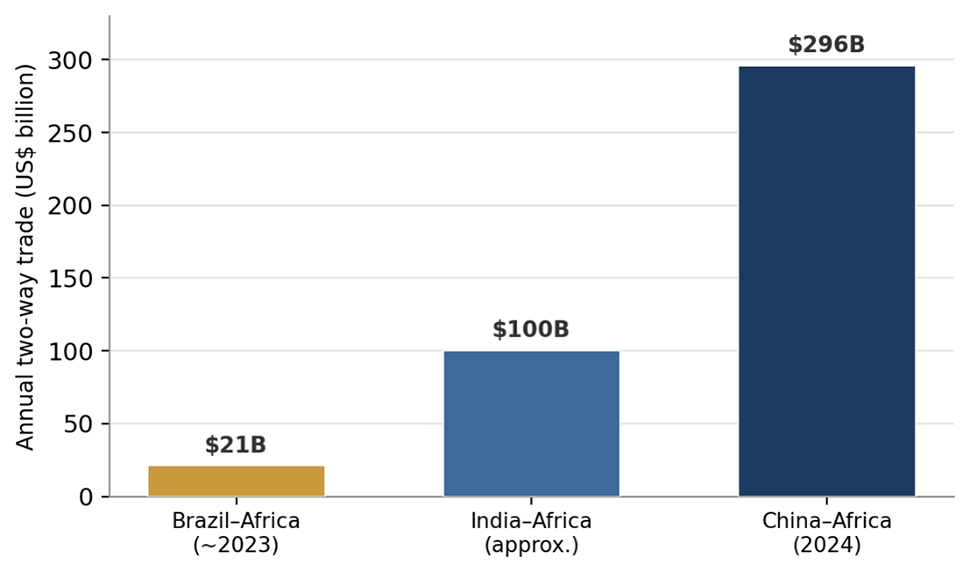

The trade the corridor addresses is modest. Brazil-Africa commerce has declined from roughly $28 billion dollars in 2013 to about $21 billion in recent years, close to 3.5 percent of Brazil’s total trade.

That figure sits far below China-Africa trade, which reached a record $295 billion dollars in 2024, and below India-Africa exchange of roughly $100 billion. Brazil ships animal protein, sugar, corn, and other agricultural goods to African markets, drawing on an agribusiness sector whose exports hit a record $169.2 billion dollars in 2025.

African shipments to Brazil consist mainly of crude oil and fertilizers, much of which moves on bulk and tanker tonnage outside the container system the corridor serves.

The two regions are complementary in some respects. Brazil ranks among the largest exporters of sugar, soybeans, beef, and poultry, while many African economies are fast-growing food importers with limited domestic production, and African demand for halal-certified protein has supported Brazilian meat exporters in particular.

The reverse flow is narrower and concentrated in raw materials, including the fertilizers on which Brazilian agriculture depends. That imbalance keeps the containerized traffic of the corridor weighted toward the outbound Brazilian leg, and it explains why a single operator controlling warehousing and inland distribution on the African side can extract value that fragmented shippers cannot.

Figure 2. Two-way trade with Africa, by partner. Sources: World Bank; China-Global South Project.

Geopolitical Implications

The corridor fits a wider Emirati strategy of acquiring logistics infrastructure across Africa and Latin America. DP World and its Gulf peers have spent the past decade securing port and terminal assets along African coastlines, positions that carry both commercial and strategic weight.

The Brazil-Africa Link extends that footprint into the South Atlantic and ties it to Latin America’s largest economy. The Gulf presence in Brazil already reaches beyond logistics, with Emirati entities among the largest Middle Eastern investors in the country and non-oil trade between the UAE and Brazil rising to about 5.4 billion dollars in 2024. The corridor joins these commercial ties to the African assets DP World has accumulated, placing infrastructure at both ends of the route under a single Gulf operator.

Both the United Arab Emirates and Brazil belong to the expanded BRICS group, which the UAE joined in January 2024. At the BRICS summit hosted by Brazil in July 2025, the Abu Dhabi Investment Group and Banco do Brasil signed a memorandum for a $100 billion investment fund, the largest such commitment between the two states.

A trade agreement between Mercosur and the UAE is under negotiation. These ties give the corridor a political frame that aligns with President Lula’s pursuit of diversified partnerships, a course reinforced by trade friction with the United States in 2025.

The corridor also offers an alternative to the established pattern of South Atlantic trade, in which cargo between Brazil and Africa often routes through European or Middle Eastern transshipment hubs.

By providing a direct, single-operator service, DP World positions itself against both that indirect routing and the Chinese logistics presence that has expanded across Africa under the Belt and Road Initiative.

For the corridor states, the arrangement brings improved market access and infrastructure investment, along with deeper dependence on a single foreign operator for a strategic trade route.

Economic Implications

The corridor’s design points to a clear set of winners and losers. DP World stands to capture margin across the full length of the supply chain, from quay to inland warehouse, by selling integration rather than a single port call.

Brazilian agribusiness exporters gain a more direct route to African buyers, and the corridor states gain port upgrades and logistics capacity. The clearest losers are the freight forwarders and intermediaries who currently assemble these shipments across multiple handlers, together with the European transshipment hubs that capture throughput when Brazil-Africa cargo routes through the Northern Hemisphere.

Table 2. Winners and Losers of the Brazil-Africa Link

| Stakeholder | Position | Rationale |

|---|---|---|

| DP World (UAE) | Winner | Captures margin across ports, warehousing, and inland transport by selling integration |

| Brazilian agribusiness exporters | Winner | More direct access to African protein, sugar, and grain markets |

| Angola, Mozambique, South Africa | Winner | Port upgrades, logistics investment, and jobs |

| Freight forwarders, intermediaries | Loser | Single-operator model absorbs the coordination they currently provide |

| European transshipment hubs | Loser | Direct routing bypasses Northern Hemisphere transfer points, reducing revenues and market share. |

| Maersk, Hapag-Lloyd, carriers | Mixed | Remain DP World terminal customers; lose forwarding-layer margin |

| COSCO, rival operators | Mixed | Santos mega-terminal auction could seat a competitor at the corridor’s main port |

Source: Author analysis based on DP World disclosures and trade-press reporting.

The position of the major shipping lines is more complicated. DP World operates terminals rather than its own ocean carrier at Santos, and it relies on lines such as Maersk and Hapag-Lloyd as customers; it signed a long-term terminal agreement with Hapag-Lloyd and a multiyear arrangement with Maersk. The disintermediation therefore targets the European hub leg and the forwarding layer rather than the mainline carriers that call at its terminals.

A competitive risk sits at the corridor’s Brazilian end. Brazil’s port regulator has structured a 6.4 billion real auction for a large new container terminal at Santos and moved to bar the port’s existing operators, including DP World, from the first round to widen competition, a model that remained under review in mid-2026. Expected bidders include China’s COSCO and other international operators, which could establish a rival presence at the same port on which the corridor depends.

For African importers, a more reliable protein and grain channel carries a food-security dimension, since several corridor markets rely on imports to meet domestic demand.

Removing a transshipment leg and reducing the number of handlers can lower delivered costs and shorten transit times, though the size of those gains depends on the volumes the corridor ultimately attracts.

The same consolidation that benefits shippers also narrows their options, leaving exporters and importers along the route more reliant on the pricing and service decisions of one operator.

Forecast

The Brazil-Africa Link is best understood as the consolidation of an underdeveloped lane rather than the start of a trade surge. Brazil-Africa volumes remain small, and much of the Africa-to-Brazil flow lies outside the container model, which limits near-term growth. The value to DP World comes from owning both ends of a route that competitors serve only in fragments.

Several developments will indicate whether the corridor moves beyond branding. Dedicated sailing schedules for the lane, which had not been confirmed in public sources as of mid-2026, would signal genuine volume.

New financing, additional partners, and the outcome of the Santos terminal auction will shape the competitive landscape. The broader trajectory depends on the Mercosur-UAE trade negotiation, the Abu Dhabi investment fund, and Brazil’s continued movement toward BRICS and South-South partnerships.

For corridor countries and the wider commodity trade, the Brazil-Africa Link signals the steady extension of Gulf logistics control into the South Atlantic, a region that links two major sources of food, energy, and minerals.

The arrangement deepens South-South commercial ties while concentrating the infrastructure that carries them in the hands of a single Emirati operator.

.jpg")

., modified")