The year 2023 will go down in history as one of defied expectations for China’s policymaking establishment and the manifold analysts who called it wrong. Both were banking on a post-pandemic economic recovery that never materialized, and this failure to launch is now shaping markedly gloomier forecasts for 2024.

One event framed the political context of the first half of 2023 more than any other: the abrupt end of China’s zero-COVID policy. The first few months of the year saw hospitals and health services overwhelmed with the sick, and a population fearful of catching a virus that had been aggressively stigmatized by the state. COVID-related deaths rapidly mounted, though no one can be sure of the exact number given underreporting in the official data. Estimates of total deaths range from the hundreds of thousands to millions.

There was a widely held expectation that, once this transitory period was over, the Chinese economy would experience a boom much like the United States did after 2021, fueled by pent-up consumer demand and savings over the course of the pandemic. But the boom has yet to materialize; on the contrary, the listless post-COVID recovery has thrown long-term economic contradictions into even sharper relief, namely weak consumer spending, declining real estate markets, mounting debt burdens, and capital imbalances.

Now one quarter into the new year, China watchers are scanning for any sign of an economic inflection point, one where the doldrums of 2023 can be put squarely in the rearview mirror. Fortunately, the latest data is providing some much-needed fuel for the optimists.

Strong retail sales and industrial production to start the year

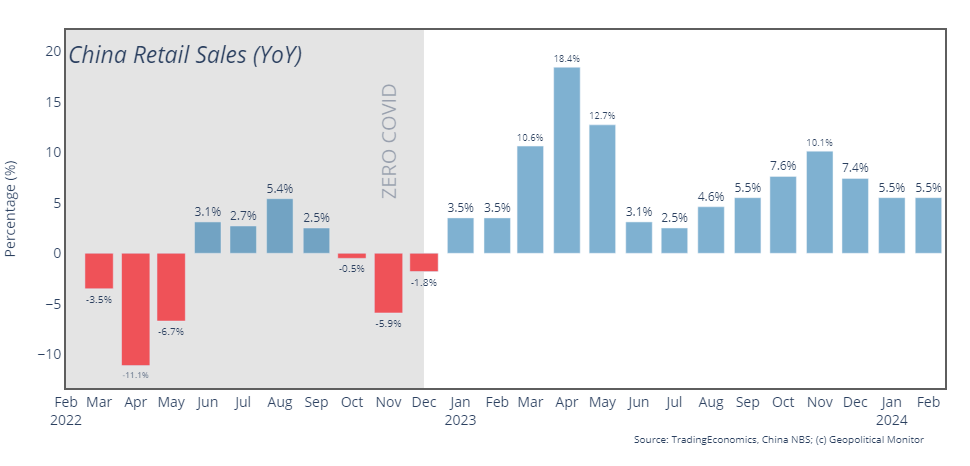

China’s economic performance in the early months of the year surpassed expectations, with retail sales increasing by 5.5%, outpacing the 5.2% growth predicted by analysts. This growth was accompanied by a significant 7% rise in industrial production, exceeding the forecasted 5% increase, and a 4.2% uptick in fixed asset investment, which also surpassed analyst expectations of 3.2%. Notably, online retail sales of physical goods saw a robust 14.4% increase from the previous year, signaling a strong consumer shift towards digital platforms.

The Chinese government seems to recognize the need for additional policy measures to achieve its ambitious growth target of around 5% for the year, particularly through demand-side interventions such as fiscal policy adjustments and efforts to boost housing and consumption. National Bureau of Statistics Spokesperson Liu Aihua highlighted ongoing domestic demand challenges, describing the economy as being in a critical period of recovery. Despite the festive boost from the Lunar New Year, which typically elevates economic figures for January and February, concerns remain regarding the sustainability of the (tentative) recovery we’re seeing in retail sales and overall consumer confidence. All told, neither has rebounded as strongly as anticipated post-pandemic, as described above.

Optimism in consumer spending and industrial output is tempered somewhat by an unexpected decline in new loans, which typically signals headwinds for household borrowing and consumer sentiment, producing the inevitable calls for further monetary policy easing. This is also where concerns in the real estate sector continue to reverberate, as lower property prices and transaction volumes dampen consumer appetites for new borrowing and spending. Meanwhile, the Chinese government’s strategic shift towards bolstering manufacturing and technological capabilities, rather than providing significant new support for the real estate sector, suggests a focused effort on high-quality development and an added degree of caution with regard to creating new inefficient investments.

Manufacturing and services on the upswing

The government’s focus on manufacturing and high-tech is underscored by recent data showing an uptick in exports and imports, suggesting a resilient external sector amidst a more complicated domestic outlook. The (state-issued) China NBS Manufacturing PMI posted a significant expansion in March, a welcome relief after 10 of the past 12 months showing contraction. It was also an upside surprise given the 49.9 reading that analysts were expecting. According to National Bureau of Statistics senior statistician Zhao Qinghe, the surprise March improvement is down to increased market activity as companies accelerated production resumption after the holiday break. The Caixin manufacturing PMI posted an even higher reading at 51.1 points for March. The uptick in manufacturing orders was broadly driven by increased orders from both domestic and international markets.

Elsewhere, the non-manufacturing PMI also saw an increase, rising to 53 in March from 51.4 in February, marking the highest reading since June 2023. The improvement in service sector activity comes as China’s economy attempts to recovery from the zero-COVID era, facing significant challenges, particularly in the real estate sector due to efforts to reduce excessive borrowing among property developers.

No signs of relief in real estate sector

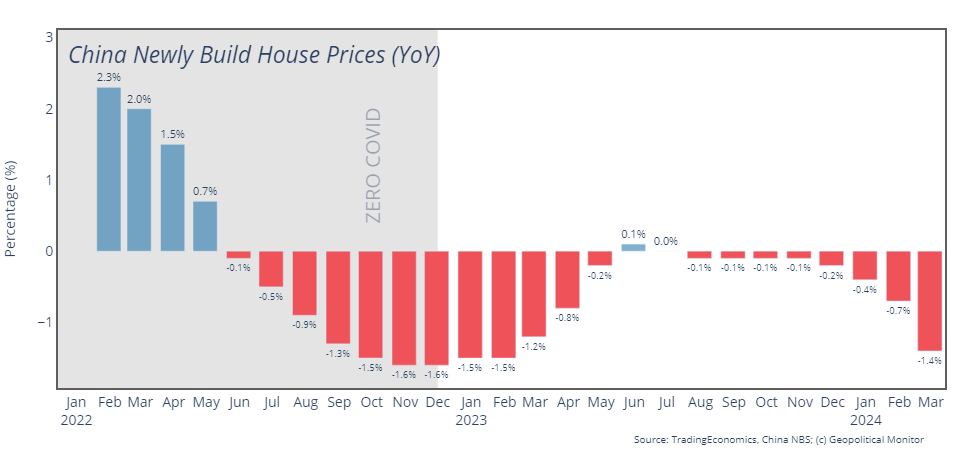

The real estate sector continues to face strong headwinds, with investment falling by 9% year-on-year, underscoring sectoral divergences in the broader economic landscape. As outlined in previous backgrounders, it’s hard to capture the dynamics of China’s real estate market in any one metric: official data is limited and potentially skewed, private alternatives are rare, and the actual economic forces at work vary wildly on the basis of city tier. The glimpses that we do catch however tend to be overwhelmingly negative. It’s clear from the state data that new home prices have yet to turn the corner and are continuing to decline on average. The situation is even more dire for second-hand homes, as the 6.3% year-on-year decline recorded in February marks the worst reading since data was first collected in 2011.

With Evergrande now bankrupt and consigned to the dustbin of corporate history, the focus has shifted to another of China’s large property developers – Country Garden, whose shares were recently suspended in Hong Kong after several delays of its annual financial results. Elsewhere, shares in state-backed property developer China Vanke tanked after it announced a two-year program of debt reduction.

With Evergrande now bankrupt and consigned to the dustbin of corporate history, the focus has shifted to another of China’s large property developers – Country Garden, whose shares were recently suspended in Hong Kong after several delays of its annual financial results. Elsewhere, shares in state-backed property developer China Vanke tanked after it announced a two-year program of debt reduction.

A floundering real estate sector will continue to limit positive economic signs emerging elsewhere. Beijing’s response has thus far revolved around a targeted easing of banking and borrowing regulations meant to bolster buyer confidence. However, excessive oversupply in the market represents a problem with no easy solution. It is in this context that we’re starting to hear about a massive new government intervention in the sector, one that will broadly have two objectives: 1) address the fundamental contradictions that are stymying the economy (consumer spending first and foremost); and 2) contribute to a social safety net in a country that will face a broad aging trend over the coming decades. To this a third point could probably be added: to maximize Party control in a sector that is critical to wider social stability. The details of these plans remain murky, but some have suggested they involve a massive program of state purchases of distressed property assets, which are then in turn owned and rented by the government. More details will surely emerge over the course of 2024; the longer and deeper the pain in the real estate sector, the more likely we may see sweeping state action along these lines.

State finances remain a question mark

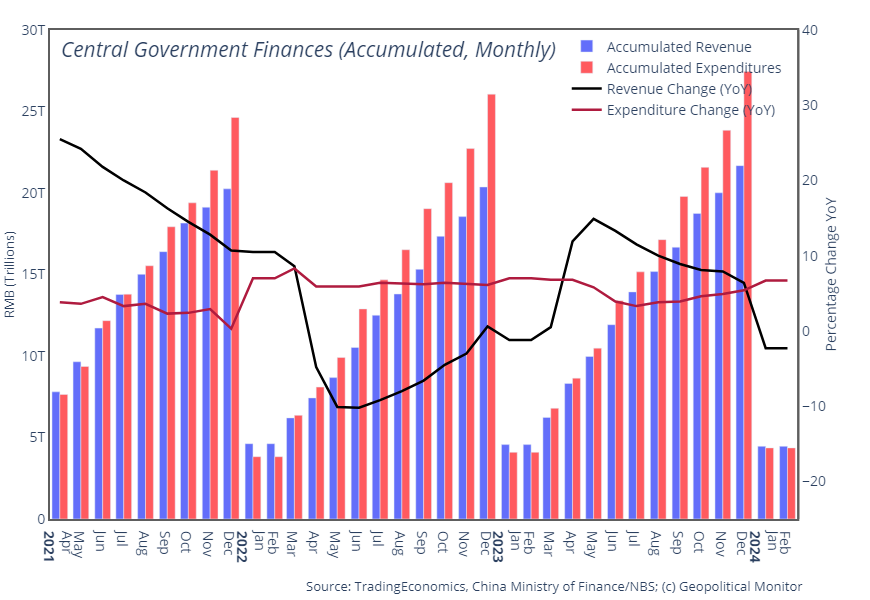

Any new government outlays are going to be assessed against the structural risks of China’s growing debt load. China’s total debt-to-GDP ratio hit a new record of 287.8% in 2023, following a 13.5% year-on-year expansion pinched on one end by the lower revenues of an economic slump and on the other by the spending demands of bailing out distressed industries. Over the calendar year, China ran a deficit of approximately 3% of GDP (probably a lower side estimate). There is a growing consensus that the 2024 number will be even higher given desire to stimulate growth with an accommodative fiscal policy, possibly necessitating a new and extraordinary round of bond issuance, similar to the round of borrowing initiated during the COVID pandemic.