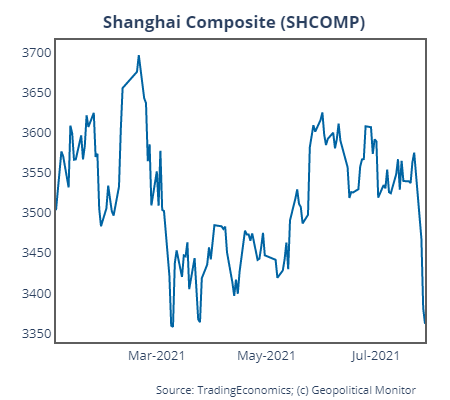

Chinese equities saw a broad sell-off to start the week, only to regain a tenuous equilibrium by the end of Wednesday trading. The selling was most pronounced in the tech sector, which has been targeted in an ongoing regulatory crackdown by state authorities. Tencent, China’s largest company by market capitalization, dropped 9% in just one day following an announcement that it had temporarily paused new sign-ups to WeChat in order to “align with all relevant laws and regulators.”

The sell-off reflects growing regulatory pressures both within and without China, which are fueling fears among investors that their capital is at risk of being summarily wiped out, not by market forces, but by the stroke of a pen in Beijing or Washington.

Analysis

Market tremors can be viewed as the latest indication of financial decoupling between China and the United States, a process that stretches all the way back to efforts by the Trump administration to ensure US ownership of data-sensitive companies like TikTok. However, it’s important to note that said decoupling isn’t necessarily the overriding regulatory goal of Chinese regulators. For example, whether the anti-trust investigation that caused Meituan stock to shed 50% of its value since February is motivated by protecting worker rights or punishing the rhetorical whims of CEO Wang Xing, neither has anything to do with US-China relations.

The key difference, though, is that now the Chinese authorities are much more willing to accept financial decoupling as a fait accompli. Indeed, recent moves have almost universally had the effect of discouraging foreign investment in the manifold industries that the Party considers to be politically sensitive.

The Didi saga shook markets earlier in the month: a Chinese ride-sharing company that listed on the NYSE only to be targeted by Chinese regulators days later, presumably after Didi failed to display sufficient deference to the Cyberspace Administration of China (CAC) ahead of its IPO. The stock has now shed over half its value since being listed. A slew of new rules from Chinese regulators followed, most of which are geared toward encouraging tech startups to list in Hong Kong rather than in the United States.

On the US side, the Securities and Exchange Commission (SEC) has taken steps toward bringing US-listed Chinese companies into compliance with long-ignored auditing rules, a move that threatens Chinese tech giants like Alibaba and Baidu with eventual delisting should they continue to withhold their auditing reports.

A regulatory crackdown on China’s private education industry has also shaken investor confidence, though this too is an example of an ostensibly domestic policy prerogative – mitigating spiraling private tutor costs so as to boost birth rates – producing major shockwaves for global capital. The proposed plan would transform a $100 billion oasis of foreign investment into a non-profit sector, wiping out billions of investments from major institutional investors like BlackRock, Tencent, and Softbank in the process.

What projects to be even more consequential, however, is that the fact the proposed regulations go so far as to ban companies using variable interest entities (VIEs) to maintain a presence in the private tutoring industry. VIEs are a longstanding loophole whereby foreign investors could gain access to the Chinese economy despite a domestic ban on foreign ownership; they are a structure that affords economic benefit while foregoing corporate control.

Though the list of recent regulatory shocks is long and getting longer, it is the targeting of VIEs that is causing many foreign investors to rethink their future China exposure, as an attack on the VIE structure is hypothetically an attack on all of US-listed corporate China, including Alibaba, Baidu, and Pinduoduo. Incidentally, the flimsy legal protections afforded by VIEs have been the target of intense criticism since the structure first arrived in US markets in the early 2000s.

Regulatory motivations notwithstanding, it goes without saying that recent events are testing the risk appetite of foreign institutional investors. Indeed, the selling frenzy that descended on Hong Kong’s Hang Seng exchange on Tuesday was driven in part by rumors that US-based funds had started to unload their China and Hong Kong assets. Whether or not there’s any truth to these rumors, it’s readily evident that the stakes couldn’t be higher: an estimated $1 trillion worth of Chinese tech stocks are held by US investors, the bulk of which comes via US-based listings.

Forecast

In the past, the Chinese government has managed to strike a balance between ensuring foreign investor confidence and advancing the Party’s political imperatives. Will it achieve such a balance again? And more importantly: Does Beijing even want to? The answer might be ‘no’ on both fronts, the reason being that Chinese regulators see the writing on the wall in recent moves by the US SEC. One way or another, US and China markets appear headed for a messy break-up, suggesting more market volatility to come.

In the past, the Chinese government has managed to strike a balance between ensuring foreign investor confidence and advancing the Party’s political imperatives. Will it achieve such a balance again? And more importantly: Does Beijing even want to? The answer might be ‘no’ on both fronts, the reason being that Chinese regulators see the writing on the wall in recent moves by the US SEC. One way or another, US and China markets appear headed for a messy break-up, suggesting more market volatility to come.

.jpg")