at the Gaylord National Resort & Convention Center in National Harbor, Maryland. // cc Gage Skidmore - https://www.flickr.com/photos/gageskidmore/54360989675")

Nuclear energy currently provides 5-7% of Argentina’s electricity, but successive administrations have failed to push for increased investment and construction has lagged on new reactors. In December 2024, Argentine President Javier Milei announced the “Argentine Nuclear Plan” (APN) that presented a three-step plan to support the resurgence of Argentina’s domestic nuclear energy capacity. The APN would guide Milei’s other ambition to build off-grid Small Modular Reactors (SMRs) to support the development of new AI data centers that are in high demand.

However, both the APN and AI strategy are fraught with economic and geopolitical challenges that have not been properly considered by the Milei administration. The challenges are threefold: firstly, developing a new domestic SMR design is a long and costly venture; secondly, AI data centers are capital intensive and deliver few long-term jobs, and lastly, investing in off-grid SMRs to power data centers will continue to push back urgently needed investment into Argentina’s electricity grid which is currently struggling and suffering from significant lack of proper investment.

SMRs are considered a highly attractive nuclear technology due to their potential to address many limitations of traditional large nuclear plants, offering lower upfront capital investment and faster deployment timelines. SMRs can come online in as little as three years, compared to up to 12 years for conventional reactors. While offering greater flexibility for locations unable to accommodate larger facilities, these compact reactors, typically under 300 megawatts in capacity, can be largely manufactured in factories and require minimal on-site construction, making them suitable for locations unable to accommodate larger facilities, such as smaller electrical markets, isolated areas, and even decommissioned coal plant sites.

Nuclear leaders like Russia, the United Kingdom and the United States have been working to develop SMR engineering and design and make projects economically feasible and attractive to investors. The design, certification, and implementation of SMRs involve using extensive in-country knowledge, but also billions in funding for research and development. As of now, only China has successfully developed and deployed a SMR reactor in Shandong Province, and other countries are rushing to catch up.

CAREM-25: A Cautionary Tale of Ambition

The APN rests on the successful development of a domestically produced SMR design that can be used in Argentina and later exported abroad. However, Argentina’s recent nuclear energy history is fraught with challenges and setbacks. The Argentine-designed CAREM-25 32Mwe SMR that began construction in 2014 was meant to herald an Argentine nuclear renaissance and increase Argentina’s nuclear power generation. Yet, by 2023, CAREM-25 had only reached 85% completion and saw 470 engineers laid off in early 2024 due to Milei’s 54% budget cuts to nuclear projects.

Wider economic decisions combined with technical challenges have limited the development and construction of CAREM-25. The SMR was supposed to have been completed by 2017 – later pushed back to 2020 – and a new timeline of 2028 is now looking untenable following recent budget cuts and mass firings. CAREM-25 represents the dichotomy that the Milei administration will face with the development of nuclear power: the high upfront cost and the long lead times clash with Milei’s need for economic restraint to control inflation and stabilize the larger Argentine economy.

The austerity measures implemented by Milei to help the Argentine economy in the short term has been impressive, such as pushing down inflation to from 2024 highs of 275% to 43% this year. However, this conflicts with the reality that nuclear projects remain a long-term investment and project with few immediate and obvious economic or political benefits.

Many of the challenges that CAREM-25 faces are the result of over 20 years of economic mismanagement and strict local component mandates that have beguiled the project with delays. Key nuclear infrastructure has often been sourced from limited countries including France, Japan, Russia, China and the United States. Creating a domestic supply chain requires long-term investment to build the technical manufacturing capacity that Argentina currently lacks. For example, SMRs require High Assay Low Enriched Uranium (HALEU) fuel, which typically ranges from 5-20% enriched uranium-235. HALEU is enriched significantly above the 5% level that powers most of the nuclear power plants currently operating in the world, so an entirely new global supply chain must be created for HALEU fuel. As of today, Russia and China are the only suppliers of HALEU, and this will prove one of the largest challenges for SMR developers, including Argentina. Russian control of the global HALEU supply chain will increase competition for limited supplies and push up prices, and Argentina’s limited availability of foreign cash reserves will be further diminished by higher prices for HALEU.

The onerous requirements for local manufacturing and production of highly technically complex critical components coupled with strict import controls have severely limited the progress of CAREM-25. These challenges will continue until either more of the key components and technology are imported, or there is enough investment into the entire nuclear chain to support local profitable commercial ventures.

Nuclear fission construction remains a project that requires long-term economic, political and social stability. Former administrations, including the Macri and Milei governments, have relied on sweeping reforms that cut costs in the short term, but create long-term fissures for Argentine nuclear development. These pendulum swings disincentivizes foreign investors and favors quick agreements to create short-term economic successes. The political reality of Argentina lends itself to short-term gains over long-term strategy and planning, which is one of the largest requirements of nuclear projects. Milei will have to use considerable political capital to secure and protect investment in nuclear and SMR projects without guarantees that they will deliver economic, political, or social benefits during his administration.

Nuclear Construction Challenges

Milei will also have to contend with the reality that modern-day nuclear power stations are fraught with delays and cost overruns. According to the IEA, projects across Europe, South Korea, and the United States have faced delays exceeding five years, with significant kW price increases. These countries already have established nuclear programs with a strong nuclear industry and skill base yet are still facing problems. Nuclear projects worldwide average 8-12 years for completion – significantly past Milei’s current administration.

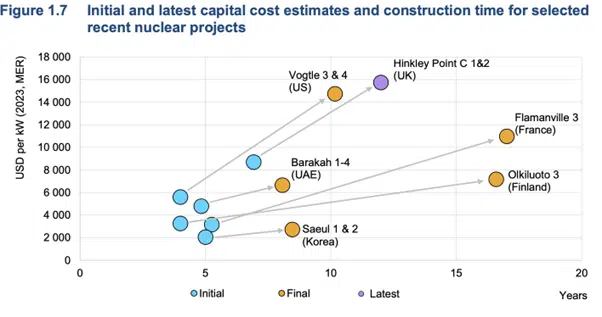

As the IEA graph below shows, delays and cost overruns have been rampant across nuclear infrastructure projects, leading to increased kW prices for consumers and governments. These delays will decrease the overall appetite by nations and investors to support the development of fresh nuclear, instead opting for extending existing nuclear station lives or finding alternative energy investments. How these delays will play out during the current, and possible future, Milei administrations remain to be seen, but the long-term nature of nuclear projects does not lend itself to Argentina’s highly fractured politics. The recent changes in government between de Kirchner, Macri, Fernandez, and now Milei are indicative of an electorate and political system that is often changing between extremes, with few of the former administration’s policies ever remaining intact. The Argentine midterms in October 2025 will be an indicator of the support for Milei’s unorthodox economic and political policies and the feasibility of a second term that would further secure the development of the APN.

Figure 1: International Energy Agency (IEA) analysis shows how nuclear projects, especially in OECD economies, have faced significant delays and capital cost increases, pushing up energy prices.

Even countries that may not have built a reactor in over 10 to 20 years retain institutional capacity while operating their plants. Argentina is not a new-to-nuclear country but has limited depth in the field, especially as recent previous administrations have restricted investment in nuclear as an energy source. Milei will have to moderate his demands of the limited Argentine nuclear industry that has taken other nations decades and billions of dollars to create and support. This will create further strains for the government as it seeks to rein in government spending while maintaining levels of research and development that are required to sustain a safe and thriving nuclear energy industry.

Atucha III: Geopolitical Delays in Action

Atucha III, a planned 1.2 GW nuclear power plant utilizing China’s third-generation Hualong One (HPR1000) reactor technology, is set to complement the existing German-designed Atucha I and II units in Argentina. The project, part of the Belt and Road Initiative, was initially agreed upon in 2015, with a formal contract signed in 2022. However, the construction of Atucha III has faced significant delays due to the complex geopolitics surrounding Argentina’s energy sector and large deposits of critical mineral resources, such as lithium. These tensions reflect the broader global competition in developing nuclear energy and mining critical minerals, particularly as Milei attempts to balance energy needs, economic interests, and international partnerships.

In 2022, China agreed to finance 85% of the $8.3 billion project, but due to hyperinflation and a deteriorating economic outlook, Argentina later demanded 100% upfront financing from Beijing. The Hualong One reactor is largely dependent on Chinese technology, limiting the involvement of Argentina’s nuclear industry and engineers. When Atucha I/II was built, Argentina sought German, Spanish and Brazilian assistance while also undertaking human capital investment. At the project’s height, it employed 7,500 people. Unlike the Chinese-sponsored Atucha III, Atucha I/II helped upskill Argentina’s scientists on nuclear technology and established a thriving local nuclear education and business track.

Between 2010 and 2018, Argentina and Russia held extensive talks and signed MoUs for the development of nuclear power using Russian technology. Since 2018, negotiations between Moscow and Buenos Aires have stalled because of a new administration in Argentina, and the Ukraine war. Both Russia and China recognize that Argentina remains a country with immense nuclear capacity coupled with a long history of using nuclear power. However, development of new nuclear projects and technologies in Argentina over the last 15 years has been limited. This slowdown further limits Argentina’s ability to negotiate international nuclear agreements and quickly restart development and construction on complex infrastructure projects.

The proposed Atucha III project has placed Argentina in a challenging position, balancing a range of geopolitical heavyweights that are looking to expand their influence with Argentina and its proven lithium and critical mineral resources. As the Trump and Milei administrations further align on geopolitical topics, will the Chinese sponsorship of Atucha III be under threat, and will a globally retreating US foreign policy entertain the idea of challenging Chinese nuclear energy influence in Argentina?

Artificial Intelligence

Milei has also raised the prospect of directly connecting proposed new SMRs with data centers that are in high demand because of AI. Atucha-III demonstrates that building new nuclear plants, even with familiar designs, is already expensive and complex. Using new, relatively experimental nuclear designs (SMRs) that introduce new designs and require a specific type of uranium will prove to be even more challenging. Argentina’s southern provinces provide a good climate that can provide cheap cooling, and data centers are energy-intensive: a single large data center can consume as much electricity as 50,000 homes. Purpose-building SMRs for data centers will not help solve Argentina’s larger energy demand and supply challenges.

Directly connecting off-grid data centers powered by dedicated nuclear energy sources will ultimately reduce the government incentive to fix Argentina’s electricity grid. As private, self-sufficient infrastructure to support energy-hungry AI data centers is built, companies and utility firms become less reliant on the public grid’s stability and reliability. This shift risks diverting political and financial attention away from urgently needed grid modernization for the broader population. If elite sectors and foreign investors can bypass the deteriorating grid, there is less pressure on the government to address chronic underinvestment, outdated infrastructure, and persistent blackouts that affect ordinary Argentine citizens. This will deepen energy inequality and prevent the development of a robust, inclusive national energy system.

Argentina’s electricity grid faces rising electricity demand, combined with outdated infrastructure from years of economic mishandling and investment shortfalls. The lack of investment has created energy bottlenecks as the grid lacks the capacity to effectively absorb new energy solutions as they are brought online. To effectively include additional base-load nuclear, Argentina must invest in improving the national energy grid to support both increasing demand and supply.

The Argentine administration seems to think that tying new, experimental nuclear power directly to data centers will make it easier to attract foreign investment. While this is certainly the case in the U.S., where states such as Virginia have drawn in massive investment (70% of the world’s internet traffic is estimated to run through Northern Virginia), this success will not be replicated in Argentina. This approach will not address Argentina’s unreliable electricity supply and will divert millions intro constructing off-grid data centers and power stations. The lack of investment will eventually further challenge the stability of the Argentine grid as energy demand from the wider economy continues to grow without the equivalent investment. Ultimately, this will deliver little value to Argentines and the economy and further entrench the existing supply and demand issues that exist within the Argentine electricity grid.

Data centers are capital-intensive, meaning they produce few high-quality jobs and contribute little to local communities. SEC filings in Virginia show how data center operators are now calling for expanded investment in electric transmission facilities to meet the growing demand. Argentina would be unable to invest in supporting the additional demand coming from both AI data centers and the population to ensure that both have their respective needs met. Milei expects nuclear energy to address the energy demands of AI data centers without considering the significant problems already facing the electricity grid.

Long-term Stability

The lack of long-term financing and government stability have hampered successive governments’ efforts to negotiate with foreign governments and energy companies for the further development of nuclear power. Milei’s 2024 Incentive Regime for Large Investments (Régimen de Incentivo para Grandes Inversiones, or RIGI) has provided a generous series of incentives to build investors’ confidence in the Argentine economy. However, the long lead times for nuclear power mean that a change in administration or a weakening in Milei’s political stability might make this legislation irrelevant and risk any long-term investments.

RIGI has had some notable recent successes, including attracting $2.5 billion from Rio Tinto to expand their Rincon mining project to 60,000 tonnes of lithium per year. Yet, Argentina’s history with foreign investment and nationalization under previous Peronist administrations, such as the YPF and Repsol case, will continue to make foreign investors wary of making large investments. The long-term nature and frequent delays of nuclear projects means that securing foreign investment in any nuclear project will require strong contracts and the continued development of Argentina’s economic and political stability even after the Milei administration.

The long lead times of nuclear projects and the fact that CAREM has faced so many struggles will make international energy companies and foreign governments wary of making long-term investments into Argentina. To secure international financing at accessible terms, Milei must provide incentives for long-term, high capital investments to secure foreign support for the construction of complex nuclear projects that are critical for the resilience of the Argentine electricity grid. Furthermore, strong contracts will be required to protect investors’ funds with project development guarantees that will secure project finances over the long term.

Conclusion

Since 2010, delays have contributed to 18% of nuclear project costs and are often overlooked when new projects are planned. Nuclear construction delays are not an Argentine-only challenge, as countries around the world have consistently struggled when building highly complex nuclear infrastructure projects. Argentina is hoping that its CAREM-25 SMR design will challenge other SMR designs from the UK, USA, France, China, and Russia. Yet Argentina remains grossly unprepared for Milei’s Argentina Nuclear Plan due to financial and geopolitical restraints that will hamper the ability of the government to push ahead to overcome funding, geopolitical, and technical challenges to leverage nuclear energy in Argentina.