The central question facing the United States is no longer whether public debt is high, but how a reserve-currency sovereign manages debt levels that increasingly rely on sustained refinancing, politically constrained fiscal choices, and continued market confidence.

Historically, heavily indebted states have often stabilized debt burdens not through explicit default, but through some combination of nominal growth, inflation, financial repression, and currency depreciation. The United States may not be deliberately pursuing such an approach. Yet the structural incentives facing policymakers increasingly appear compatible with it.

The result is not necessarily an imminent crisis, but the possibility of a prolonged period characterized by monetary accommodation, persistently compressed real yields, and gradual institutional erosion beneath the appearance of nominal stability. If such an environment emerges, it may arise less from explicit debt-monetization objectives than from repeated interventions aimed at stabilizing financial markets, preserving Treasury market liquidity, or countering recessionary pressures.

Interest Costs, Not Debt Size, Are the Core Constraint

The sustainability of sovereign debt depends less on the absolute stock of liabilities than on the relationship between nominal economic growth and the cost of servicing debt.

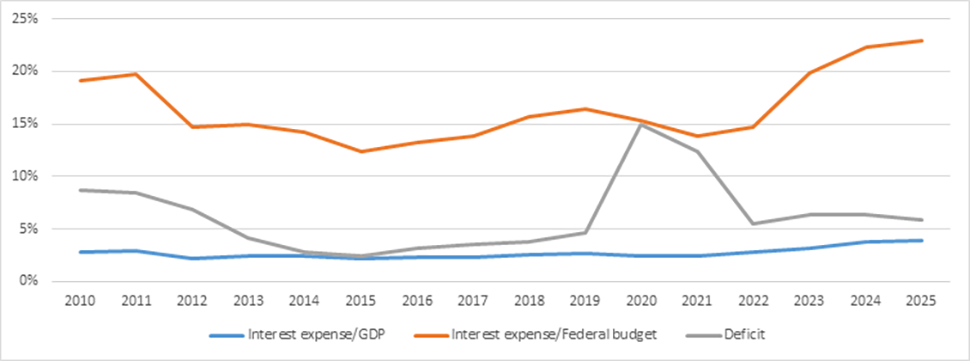

Figure 1 – Interest expense as percentage of GDP and Federal budget at nominal values.

For most of the post-2008 period, exceptionally low interest rates muted the fiscal consequences of persistent deficits. That environment now appears increasingly atypical. As rates rose after 2021, refinancing costs became materially more visible within the federal budget.

Although interest payments as a share of GDP remain moderate by historical standards despite rising in recent years, interest expense as a share of federal revenues has increased sharply. The key vulnerability lies in the structure of the debt itself: the United States relies heavily on continuous refinancing, with a large majority of Treasury gross issuance consisting of rolling over maturing obligations. As a result, higher rates gradually transmit into the fiscal position as existing debt matures.

Inflation has partially supported nominal GDP and tax revenues, but it has also forced the Treasury to refinance debt at higher nominal yields. Since 2022, federal interest expenses have risen substantially faster than federal revenues, increasing fiscal rigidity even while nominal GDP growth remained elevated.

As the overwhelming majority of US Treasury debt as of 2025–2026 remains nominal rather than inflation-linked, the underlying dynamic is relatively straightforward: interest-bearing liabilities have compounded faster than the tax base during a period in which refinancing costs normalized upward, without being offset by sustained primary surpluses or inflationary adjustment.

The Treasury substantially extended the average maturity of federal debt from 49 months in 2010 to roughly 71 months by 2025, although issuance shifted somewhat back toward bills during recent high-rate periods. By extending maturity, the Treasury reduced short-term refinancing risk and smoothed rollover needs, partially insulating the budget from immediate interest-rate fluctuations.

However, this shift involves trade-offs. Longer-dated issuance generally requires higher yields at the time of borrowing, as investors demand compensation for locking in capital over extended horizons. The cost of debt can therefore become partially “locked in” at elevated rates for longer periods. Maturity extension also affects market structure: Treasury securities function as core collateral across global funding markets, repo operations, and broader financial liquidity systems. Increasing long-duration issuance may alter the composition and availability of highly liquid short-term instruments while redistributing demand across the yield curve.

Narrowing Policy Alternatives

The principal policy options available to highly indebted advanced economies are well known: fiscal consolidation, growth-oriented investment, and financial repression. None is politically or economically costless.

Austerity in the form of sustained spending cuts or tax increases aimed at reducing deficits remains the most direct mechanism for stabilizing debt dynamics. Yet its macroeconomic effects are politically difficult. Reductions in public spending tend to weaken aggregate demand and can partially offset fiscal improvements through slower growth. In polarized democracies, sustained fiscal consolidation is especially difficult to maintain. The US budget is also increasingly structurally constrained by Social Security, Medicare, and defense expenditures.

The US federal tax system remains progressive under conventional income measures, but its degree of progressivity is reduced substantially when unrealized capital gains are treated as economic income rather than excluded until realization. A widely cited 2021 White House analysis estimated that the 400 wealthiest American families paid an average federal tax rate of roughly 8.2% when unrealized capital gains were included in the income base, signaling political unwillingness to tax concentrated wealth. At the lower end of the income distribution, limited liquid savings and declining real median financial buffers constrain additional taxable capacity without reducing household consumption.

Growth-oriented investment strategies are politically more attractive. Public investment in infrastructure, industrial policy, energy, and advanced technologies can strengthen productivity and expand the future tax base. However, such strategies operate over long time horizons, while financing costs are immediate. Additional debt-financed expansion may therefore increase short-term fiscal rigidity while depending on uncertain long-term productivity gains, making successful stabilization contingent on execution quality, policy continuity, and favorable financing conditions.

The third mechanism, financial repression, operates more indirectly. Rather than reducing debt outright, the state creates relatively captive demand for sovereign debt through regulatory incentives or institutional constraints imposed on domestic financial institutions. By channeling demand toward sovereign securities, governments can lower financing costs while reinforcing the centrality of public debt within modern collateral and liquidity systems. The tradeoff is a gradual crowding-out effect in capital allocation and a persistent suppression of risk-free returns, which can incentivize leverage and inflate asset valuations elsewhere in the financial system.

In practice, advanced economies often rely on some combination of all three approaches. Yet none fully resolves the underlying constraint: sustaining large debt burdens while simultaneously preserving growth, political stability, and market confidence.

The Structural Temptation of Monetary Accommodation

Under these conditions, mild inflation and gradual currency depreciation can become increasingly attractive adjustment mechanisms.

A reserve-currency sovereign possesses advantages unavailable to most states. Because the dollar remains the world’s dominant reserve and trade currency, global demand for dollar-denominated assets absorbs part of the monetary expansion that might otherwise feed more directly into domestic inflation.

This creates a powerful incentive structure. Policymakers may seek to:

- suppress borrowing costs;

- tolerate moderately higher inflation;

- maintain mildly negative real interest rates;

- and gradually reduce debt burdens in real terms.

The post-2008 period demonstrated the extent to which central banks can influence sovereign debt markets through asset purchases and liquidity support. During periods of systemic stress, the Federal Reserve repeatedly intervened to stabilize financial conditions and limit disorderly increases in yields.

However, this capacity is not unlimited.

Modern monetary systems ultimately depend on institutional credibility. If markets increasingly perceive monetary policy as subordinated to fiscal financing needs rather than price stability, investor behavior could shift gradually but structurally.

The Federal Reserve’s tightening cycle after 2022 demonstrated that monetary authorities remain willing to prioritize inflation stabilization despite significant market and fiscal consequences. At the same time, the resulting increase in federal interest costs illustrated how sensitive a highly indebted system can become to prolonged positive real rates. Future stress episodes could generate renewed political and financial pressure for balance-sheet expansion.

Financial repression is not simply a policy choice to keep interest rates below inflation. It is better understood as a sequence of adjustments in which markets continuously reprice inflation and fiscal-risk expectations while the central bank intermittently offsets those pressures. The result is less a linear deterioration than a regime of constrained oscillation. Such arrangements tend to function most effectively when inflation remains positive but contained, growth at least stable, and institutional demand for sovereign debt sufficiently large. Deglobalization, aging populations, and tighter labor markets may complicate the maintenance of such a regime by contributing to structural inflationary pressure.

Large private wealth can stabilize the sovereign debt, while simultaneously increasing pressure for monetary accommodation, as pensions depend on markets, households depend on 401(k)s, and collateral values support credit creation. That creates political pressure against deep recessions, large asset deflations, and prolonged high real rates.

The central risk is therefore not necessarily sudden collapse, but the gradual emergence of fiscal dominance: a system in which debt sustainability becomes increasingly dependent on accommodative monetary policy and structurally compressed real yields.

Reserve Currency Privilege and Restraint

The United States benefits enormously from the dollar’s global role, but that privilege also creates structural tensions.

To sustain dollar dominance, the global system requires a continuous supply of dollar liquidity and safe assets, primarily in the form of Treasury securities. Yet supplying those assets simultaneously increases US dependence on debt issuance itself.

This resembles a modernized version of the Triffin dilemma under financial globalization: the reserve-currency issuer must maintain confidence in its currency while continuing to expand the supply of liabilities demanded by the international system.

No alternative currency currently possesses the liquidity, institutional depth, legal infrastructure, and geopolitical backing necessary to replace the dollar fully. Nonetheless, reserve systems do not need to collapse to become incrementally less dominant.

Signs of diversification are already visible at the margins, even if they do not presently threaten the core reserve architecture:

- greater central-bank gold accumulation;

- regional settlement arrangements;

- bilateral trade agreements outside the dollar system;

- and gradual reductions in the dollar share of global reserves.

Individually, these developments remain limited. Collectively, however, they suggest that some actors are increasingly hedging against long-term dollar concentration risk.

Even partial diversification matters. Reserve-currency systems derive strength from network effects and confidence. If investors increasingly expect long-term depreciation or persistently negative real returns, diversification incentives could become partially self-reinforcing.

Unlike the relatively cohesive geopolitical environment that enabled the Plaza Accord of 1985, the international system of the mid-2020s is increasingly fragmented by strategic competition, trade disputes, sanctions regimes, and domestic political polarization. As a result, large-scale coordinated currency management aimed at engineering an orderly dollar adjustment may be considerably more difficult to achieve today.

Figure 2 – Inflation-adjusted yield on U.S. 10-year Treasury securities. Further yield compression would likely imply persistently negative real returns for lenders.

Japan: An Imperfect Comparison

Comparisons between the United States and Japan are common, but only partially applicable.

Japan sustained extraordinarily high public debt levels because several stabilizing conditions operated simultaneously:

- debt was overwhelmingly domestically financed;

- deflationary pressures dominated for decades;

- political institutions remained relatively cohesive;

- and household savings remained structurally high.

The United States faces a different configuration:

- larger external imbalances;

- greater political polarization;

- higher inequality;

- and stronger dependence on foreign capital inflows.

At the same time, the United States retains structural advantages Japan lacked, including stronger demographic dynamism, global technological leadership, deep capital markets, and greater geopolitical influence.

This combination makes the US case both unusually resilient and historically difficult to model.

Postwar Britain may offer a more relevant historical comparison. Following World War II, the United Kingdom carried debt levels exceeding 200% of GDP while confronting the gradual erosion of sterling’s monetary dominance. Rather than defaulting outright, Britain stabilized its debt burden through a prolonged combination of regulated finance, controlled interest rates, moderate inflation, and institutional pressure on domestic financial institutions to absorb government debt.

This process gradually reduced the real value of public liabilities, but it also carried meaningful distributional consequences. Persistently negative real returns transferred wealth from savers toward debtors and the state, while sterling’s gradual weakening reduced international purchasing power and diminished Britain’s financial influence over time. The system remained stable for decades, but stability increasingly depended on institutional controls and managed monetary conditions rather than strong underlying growth.

At the same time, the Volcker era and the fiscal consolidation of the 1990s serve as important counterexamples to deterministic interpretations of debt monetization or inevitable financial repression. The aggressive monetary tightening of the early 1980s demonstrated that the United States was willing to impose severe short-term economic costs in order to restore monetary credibility and stabilize inflation expectations. Real interest rates rose sharply, unemployment increased substantially, and financial conditions tightened across the economy. Yet the restoration of confidence in the dollar ultimately reinforced the long-term credibility of American financial institutions and preserved reserve-currency dominance.

Likewise, the fiscal improvements and productivity expansion of the 1990s illustrated that strong growth, technological innovation, and disciplined fiscal policy can materially improve sovereign debt dynamics without requiring prolonged inflationary adjustment. Current US investment in artificial intelligence, advanced computing, and industrial policy may reflect, at least in part, an attempt to recreate a productivity-driven expansion dynamic. While productivity expansion may improve aggregate debt sustainability, it might simultaneously be intensifying distributional divergence between asset-owning and labor-dependent households.

These historical episodes suggest that heavily indebted reserve-currency systems rarely follow a single linear trajectory.

Risks of a Managed Deterioration

The most plausible risk scenario is neither hyperinflation nor abrupt collapse.

A more plausible path may involve a prolonged period characterized by:

- persistently negative real rates;

- elevated asset inflation;

- widening wealth inequality;

- gradual erosion of middle-class purchasing power;

- increasing fiscal dependence on monetary accommodation;

- and declining confidence in institutional neutrality.

Global finance continues to rely heavily on Treasuries as primary reserve assets and pristine collateral. This creates a structural equilibrium in which rising debt can simultaneously increase systemic fragility while reinforcing demand for safe collateral. Such systems can persist for long periods. Indeed, moderate financial repression has historically proven relatively durable. The postwar period offers multiple examples of advanced economies stabilizing debt through combinations of inflation, controlled yields, and regulated financial systems.

Treasuries remain uniquely scalable, liquid, and infrastructure-based. The danger lies less in immediate instability than in cumulative long-term effects. Persistent monetary accommodation can distort capital allocation, reinforce asset-price dependence, weaken productive investment incentives, and deepen political fragmentation.

A structurally weakening dollar combined with suppressed domestic yields could also increase the attractiveness of the dollar as a funding currency for global carry trades, potentially reinforcing depreciation pressures. However, persistent negative real rates do not automatically imply sustained dollar weakness. If Europe stagnates, China exerts stronger capital controls, or Japan remains yield-suppressed, then the dollar can stay structurally strong despite US fiscal deterioration.

Figure 3 – Inflation-adjusted purchasing power of median U.S. household post-tax income, normalized to 2009.

Whether current US policy ultimately reflects deliberate strategy or iterative crisis management may be secondary. Structural incentives increasingly appear aligned with policies consistent with mild financial repression and gradual inflationary adjustment, even absent any explicit coordinated framework.

The central question is therefore not whether the United States can sustain such a system in the near term. It likely can. It is how long a reserve-currency sovereign can rely on monetary accommodation, rising debt issuance, and gradual currency depreciation before confidence begins shifting in ways that are slow, nonlinear, and difficult to reverse.

A workable stabilization path likely exists, but its long-term costs may fall less on the system itself than on the purchasing power, savings capacity, and economic security of the middle class.

A related institutional risk is the growing tendency for fiscal policy to respond to short-term electoral incentives, potentially at the expense of longer-term debt sustainability. In parallel, increasing partisanship and greater reliance on executive-driven fiscal actions could weaken congressional oversight and the traditional balance of fiscal decision-making, raising the risk of policy inconsistency and abrupt directional shifts.

, cc White House, modified, https://commons.wikimedia.org/wiki/File:Vice_President_Joe_Biden_greets_Russian_Prime_Minister_Vladimir_Putin.jpg")

2012, modified, https://creativecommons.org/licenses/by-sa/2.0/")