In January 2015, the European Central Bank (ECB) held monetary policy meetings to construct a new strategy for combating the region’s sovereign debt crisis. The main concern then was that any significant changes in monetary policy could damage the already weak prospects for generalized growth in the Eurozone.

Part of the reason for this came from the fact that the economic prospects in several countries were so fragmented as the weakest countries in the member union will likely require different measures when compared to the stronger member countries. Specifically, this means that nations like Greece, Portugal, and Spain will need to be dealt with differently than the likes of Germany and Austria. If this is not done correctly, we could be looking at several more years of economic stagnation in the region.

QE Not Achieving Desired Effect

But even with all of the attention paid to these factors, it does not appear as though the quantitative easing programs enacted last January are having their desired effect. In theory, QE programs will almost always have a negative impact on the currency of a region. This is actually a positive because lower currency valuations make export products cheaper for foreign consumers, and this can bring added sales for a region that might have otherwise been stalling.

But the specific programs enacted by the ECB have not generated this result, as the value of the Euro is now higher than it was when these QE programs were first initiated by the ECB.

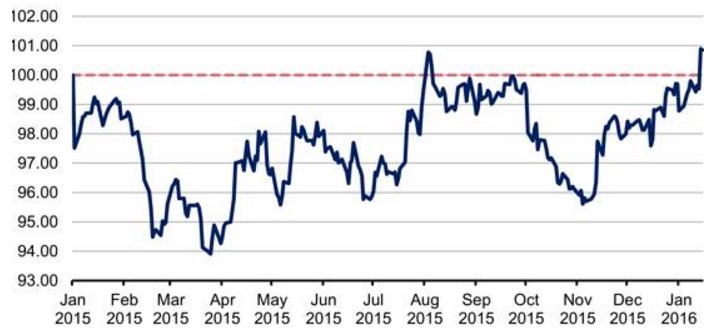

Source: Fibogroup

In the chart above, the red dotted line indicates the value of the Euro against a basket of its most commonly traded counterparts. This is a more important indicator than anything that can be determined by looking at any single currency pair (for example, the EUR/USD) because the Eurozone has significant trade relationships with all of the world’s major economies. So, while we might be seeing relatively low values in the Euro against the US Dollar, this is simply not the case when we assess things from a global perspective.

Looking Ahead

Going forward, it will be important for the ECB to continue monitoring the value of its currency in these terms. Failures here could mean that we will see changes in the monetary policy agenda that is being laid out by the central bank and this could ultimately suggest continued volatility in the shared Euro currency. This will have significance for both consumers and investors, as regional stock markets could be negatively impacted by excessive price instability.

We need look back only a few years to see the various ways that the Eurozone’s sovereign debt crisis has impacted the global economy, so there is really something here for everyone when we are looking to judge the effectiveness of the ECB’s policy measures to stimulate growth in the region. This is an issue that has faded from the headlines over the last year – but when we look at the various ways this story is playing out, we could very well see this issue become a dominant factor once again in the world’s financial news headlines.