Economic warning signs are flashing in Pakistan as fiscal constraints combine with resurgent inflation and a worsening current account.

Economic warning signs are flashing in Pakistan as fiscal constraints combine with resurgent inflation and a worsening current account.

Background

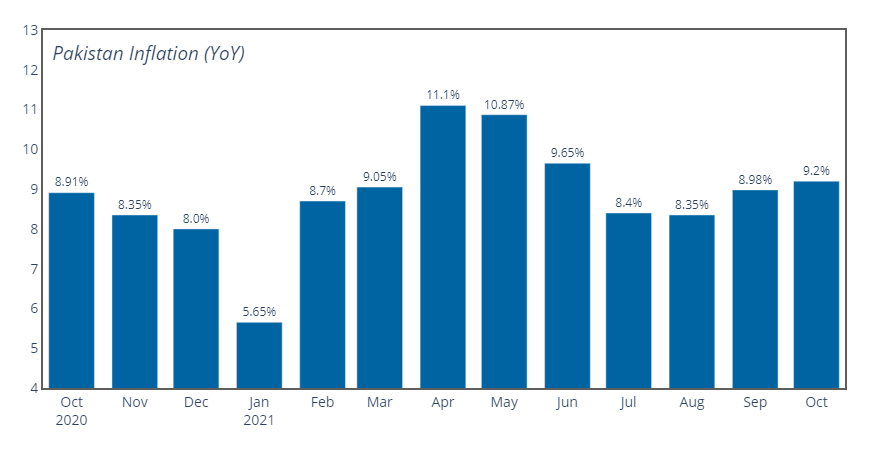

The most alarming economic trend so far as the government of Imran Khan is concerned is undoubtedly rising prices, specifically rising food prices. A broad swathe of staples has become more expensive of late: ghee is up 43 percent, flour 12.97 percent, and pulses by 17.62 percent year-on-year. Overall, food inflation is up 12.6 percent from July to November this year, and general inflation registered at 9.2 percent year-on-year in October.

It should also be noted that this recent surge comes after years of sustained inflation. With the exception of January 2021, Pakistan’s inflation rate has been over 8% since March of 2019.

Higher prices are pushing thousands of families below the poverty line and generating new political risks for Prime Minister Imran Khan. In response, the Khan government has passed a short-term relief package worth approximately $700 million, self-described as the country’s “largest ever welfare program.” The package amounts to consumer subsidies for the abovementioned staples, and is expected to remain in effect for at least six months.

Global energy price inflation is another factor behind Pakistan’s internal price woes; it is also sapping vital foreign reserves as fuel imports become more and more expensive, with weekly decreases of nearly 2% recorded over the latter half of October. The country’s trade balance remains squarely in deficit, and its current account has once again entered into freefall following the briefest of reprieves over the second half of 2020. Imports of steel, cement, and other construction materials continue to flow into the country for CPEC projects; however, a commiserate and balancing swell in exports has yet to manifest.

The value of the rupee has been battered by these various headwinds, and the currency is down approximately 10% against the US dollar since June of this year.