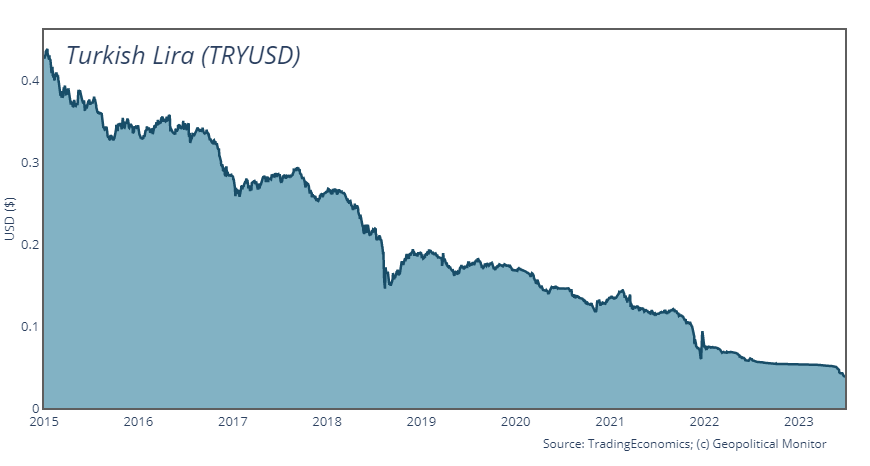

The Turkish economy has been in a precarious state over the past years, grappling with soaring inflation rates, a deteriorating lira, and dwindling foreign reserves. Amidst an economic crisis and his re-election victory in May, President Recep Tayyip Erdogan has adopted a new economic strategy. This article explores the potential implications of Erdogan’s policy shift, considering the severe financial pressures currently confronting Türkiye’s economy.

The Turkish economy has been in a precarious state over the past years, grappling with soaring inflation rates, a deteriorating lira, and dwindling foreign reserves. Amidst an economic crisis and his re-election victory in May, President Recep Tayyip Erdogan has adopted a new economic strategy. This article explores the potential implications of Erdogan’s policy shift, considering the severe financial pressures currently confronting Türkiye’s economy.

President Erdogan has long adhered to an unorthodox monetary policy philosophy, specifically in maintaining low-interest rates. Underpinning Erdogan’s desire for low rates was a controversial and contrarian idea that high-interest rates lead to inflation rather than curb it. Erdogan’s approach has been widely criticized for exacerbating the country’s economic woes.

Last month marked a significant departure from this stance. The Central Bank of Türkiye, under the new leadership of financier and investment banker Hafize Gaye Erkan, hiked the main interest rate from 8.5% to 15%. Erdogan’s appointment of Erkan to lead the central bank, coupled with his appointment of economist Mehmet Simsek as the country’s finance minister, signals a change in economic policy. Simsek served as finance minister under Erdogan in 2009 for over six years, where he was credited with managing Türkiye’s recovery during the global financial crisis.

Under Simsek’s stewardship, Türkiye implemented a countercyclical policy, including an aggressive fiscal stimulus program to boost domestic demand and reduce reliance on external debt. This was coupled with a prudent monetary policy to curb inflation and stabilize the lira. Simsek also undertook structural reforms to enhance the resilience of the Turkish banking sector, which remained relatively unscathed by the crisis.

Today, Simsek returns to a starkly different economic landscape. Unlike the 2009 scenario, which was primarily driven by global economic conditions, Türkiye’s current economic woes are largely homegrown, stemming from years of unorthodox monetary policy and dwindling foreign exchange reserves. Nevertheless, some elements of the challenge are familiar. As in 2009, Simsek will need to stimulate economic growth while balancing the pressing need for fiscal consolidation. Simsek’s biggest challenge will be to restore the credibility of Türkiye’s monetary policy while effectively navigating the intricate economic realities of today. His success will hinge on the design and execution of a robust economic stabilization program that addresses these multifaceted issues.

.jpg")