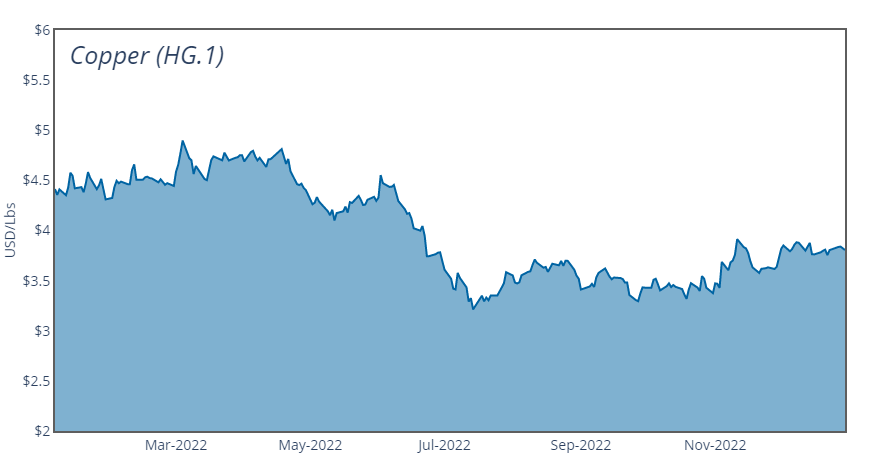

Copper markets are expected to remain relatively stable through 2023 as supply- and demand-side dynamics continue to cancel each other out.

Copper markets are expected to remain relatively stable through 2023 as supply- and demand-side dynamics continue to cancel each other out.

On the demand side, a looming recession in major economies such as the United States and, in particular, China (whose economy is currently being upended by a surge of COVID-19 infections), is tempering expectations for copper purchases and putting downward pressure on prices. Fitch expects demand to grow by approximately 2% over the course of the year, but of course, demand will ultimately be determined by the health of the global economy in the year ahead. How healthy will the economy be? Predictions are indicating various degrees of recession, ranging from the relatively tame (Moody’s ‘slowcession’ of stagnant growth) to the grim (Fitch’s ‘90s-style recession’) to the seminal (Nouriel Roubini’s ‘extreme recession’).

Soft demand is being balanced on the supply side, however, as political developments in the world’s two largest producers – Chile and Peru – continue to act as a drag on global production, keeping prices stable through the latter half of 2022.

In Chile, production is sliding due in part to labor upheavals, water shortages, and regulatory uncertainty. Through July, yearly production slumped 6% year-on-year, contributing to a 12.8% dip in exports over the same period. There is hope that the trend will reverse itself in 2023 as new operations come online, notably Teck Resources’ Quebrada Blanca Phase 2 (QB2), which is expected to add anywhere from 170,000 to 300,000 tonnes of annual output (quite substantial given that Chile produced an estimated 459,000 tonnes in 2022). However, political and environmental dynamics could still intervene to curb supply. For one, it’s difficult to overstate the potential impacts of the aforementioned water crisis, which now has more than half of the national population living in areas of ‘severe water scarcity.’ Water has long been regulated by a Pinochet-era law that is highly favorable to private interests, generating significant political tensions as scarce supply is diverted to agricultural and mining interests (water access figured prominently in the 2019 protest movement that swept the country). New copper operations such as QB2 tend to be extracting the lower-grade sulphide deposits, which require large amounts of water to process. And while some of this water can be sourced from abundant saltwater sources, new sulphide operations are also increasing demand for scarce freshwater, particularly over the near term (the industry hopes to use 68% saltwater by 2032). In addition to water issues, President Gabriel Boric is also presiding over the drafting of new mining royalty bill which will inevitably impact future investment in the copper industry; however, whatever the content of the final draft (it will presumably be less favorable to mining interests), the new scheme won’t come into effect until 2025 at the earliest.